Business

How 2025 became the year of the cyber hack – and what British businesses face next

As 2025 winds down, business leaders and executives will feel it has been a particularly expensive year as the cost of employment shot up, inflation of raw materials impacted supply chains and both oil and tariff shocks hit in the first half of the year.

But perhaps the biggest cost of all was one borne by companies hit by cyber attacks.

One damning government report suggests that close to half of British businesses (43 per cent) and three in ten charities (30 per cent) claimed to suffered a type of cyber security breach or attack in the past year. These include anything from a phishing attack to a full-blown digital shutdown costing hundreds of millions of pounds.

The list of those affected includes some of Britain’s biggest businesses.

Marks and Spencer. Adidas. Co-op Group. Heathrow airport. Harrods. And, of course Jaguar Land Rover (JLR). Each have suffered publicly confirmed cyber hacks. These attacks were not limited to companies either: the German parliament also suffered a breach and, in October, the UK government saw the Foreign Office hacked.

Organisations have to fight a moving target, one with seemingly limitless capabilities. This isn’t a foe a business and kill and move on from – cyber attacks come in all different ways, from all points of the earth and if one attempt doesn’t work, it just keeps coming.

Jason Soroko, a cybersecurity expert and host of the Root Causes podcast, put it bluntly: “For cyber attacks, 2025 was brutal. 2026 will be worse.”

What did the hacks cost?

Attackers aren’t just looking to break into digital vaults and extract cash. Data has become incredibly valuable, while damage to economic or manufacturing operations can provide an opportunity for someone else to pick up the slack in demand, meaning State-level involvement is part of the picture at times too.

The truth is for a business, lost sales are only part of the picture – there’s reputational damage to consider, possible reimbursement or lost opportunity costs, the loss of ongoing clients to rivals and, obviously, the amount spent to fix and then upgrade their own systems too.

Cybersecurity Ventures, a noted source of data and research in the cybersecurity sphere, says the entire “industry” was worth around $10.5 trillion this year alone (£7.8tn). In country terms, this would make it the third-biggest economy in the world after only the US and China.

For individual companies, the reliance is on their accountancy estimates being made public. M&S originally said the hit to their profits would be in the region of £300m, but ultimately in November gave a figure of just under half that, having recouped £100m in insurance payouts.

JLR were not so fortunate as they had not renewed their cyber insurance specifically, meaning they’d bear the brunt of a £200m estimated cost. Meanwhile, Co-op’s cyber attack saw more than 6 million customers’ data stolen, with the final tally expected to cost around £120m.

Elsewhere, the “cost” is more difficult to place a figure on, but is more wide-ranging and potentially damaging.

JLR’s shutdown was big enough, and prolonged enough, to contribute towards an economic downturn: car production failed to rebound in September and October across the industry and was one of the big factors in UK GDP contracting 0.1 per cent in the latter month.

The biggest issues and why firms are struggling

There are several good reasons why companies cannot keep cybercrime at bay.

Attacks can be multi-pronged in style or timing and have the advantage of being first: those in defence must rely on seeing what the attackers are doing and respond accordingly.

“Attackers now deploy AI at a speed defenders simply haven’t matched. It’s an asymmetry that widens by the month. Defenders have been slow to uptake stronger authentication, which is like failing to better locks on the doors. The attackers take advantage of this,” explained Mr Soroko, who works with online security firm Sectigo.

Cybersecurity Ventures, meanwhile, estimates that the “frequency of ransomware attacks on governments, businesses, consumers, and devices will continue to rise […] to hit once every two seconds by 2031.”

It’s a lot to stop – and that’s just the digital version.

What about when humans get involved? We know about people getting caught out by scams through texts, emails and more. Why would it be any different for ordinary people at work?

“We’re currently seeing youths socially-engineer their way into global businesses. After online research and exploiting other breaches to obtain information, a single phone call to a help desk can be enough to persuade them to reset passwords or MFA tokens,” explained Tim Rawlins, security director at the cyber firm NCC Group.

“This opens the door for criminals to move across systems and escalate their access until they have the same level of access as IT teams do.”

What comes next is critical.

Co-op notably opted to pull the plug, as it were, locking out those hacking them but also limiting their own initial powers of response as it was deemed that was the safest course of action.

.jpeg)

The government’s cyber report notes even the biggest firms don’t actually have a set course of action for if they are hit: 53 per cent of medium businesses and 75 per cent of large ones have “have an incident response plan”, it suggests.

“Following breaches, organisations can’t afford knee-jerk fixes,” Mr Rawlins adds. “Organisations must work with cyber experts to rebuild their systems safely; seeing how the hackers were able to infiltrate, what they accessed, and how a breach is impacting critical business systems.”

But this is a wide-ranging topic, a brand new area for many businesses to deal with and an area of high expertise needed. As such, many remain underprepared to deal with it.

Research from compliance company IO suggests a third of British and American companies don’t feel that governments are doing enough to support and protect them.

What are the next big risks?

The pace of technological change means firms are facing an awful lot of “the same, but different”. Hackers looking to exploit gaps in security, individuals unwittingly opening or accessing files and even external or third party contributors accidentally letting outsiders in have all been part of the equation this year.

Companies essentially have to defend against what they cannot see coming – plus there’s no telling when attackers themselves might decide a particular target is now the ideal one.

Moody’s, the global ratings firm, says cyber attacks on banks in particular “are rising and becoming more sophisticated”. If you thought being unable to order a click and collect from M&S for a couple of months was bad, try imagining not being able to make payments, withdraw cash or check your balance.

Happily they do note most banks have “robust defences”, though those financial institutions using technological infrastructure “developed decades ago” and simply building new apps and process on top of it do present an ongoing concern.

Simply put, it’s a race to a never-in-sight finish line to keep security systems updated. For some businesses next year, the question will at some stage inevitably turn to what the best method of containment is, rather than how to keep attackers out. Once the defences are breached, the answer to that question can be the difference worth many, many millions.

Business

Fuel price hike impact: How it will change what you eat, how you travel and what you can afford

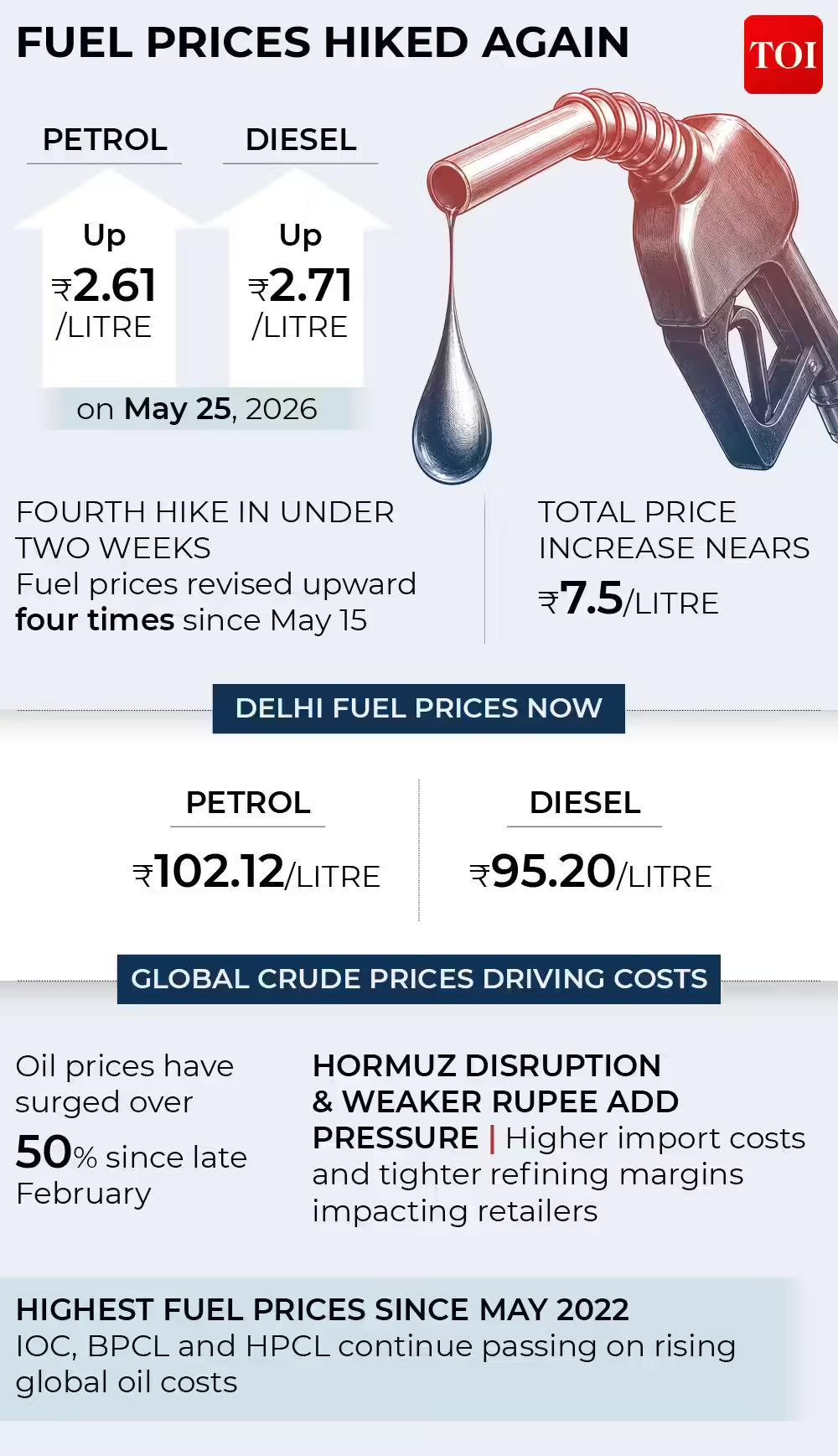

Your next trip to the fuel station just got more expensive!Fuel prices across the nation saw another revision, now becoming costlier by Rs 7.5 per litre since the Middle East crisis began. Early Monday, petrol prices were hiked by Rs 2.61 per litre, while diesel prices were increased by Rs 2.71, marking the fourth increase in just ten days.These back-to-back revisions are now raising concerns over a ripple effect on household budgets, inflationary pressures, and everyday commuting costs, leaving consumers to quietly do the math all over again.The latest round of price hikes comes against the backdrop of the ongoing conflict in the Middle East, which has tightened global energy supplies. With crude shipments under pressure and geopolitical tensions showing little sign of easing, international oil prices have been trending higher, with the impact steadily filtering into domestic retail markets.Retail fuel prices had remained largely unchanged for nearly four years before the first hike on May 15, making the sharp, fortnight-long surge in prices all the more striking.Prices continue to vary across states due to differing local taxes.

Impact of rising petrol and diesel prices

Impact on transportation

Transportation is the first and most direct sector to feel the impact of petrol and diesel price hikes. Your drive to the office, that weekend road trip, and quick grocery run — everything will now cost slightly more. With the latest increase, transporters are under significant operational pressure after four rapid fuel revisions. Fuel alone accounts for more than half of truck operating costs, and when added to rising expenses such as tires, insurance, tolls, maintenance, finance costs and statutory compliances, transport operations are now facing severe pressure on viability.“Fuel alone accounts for nearly 55% of truck operating costs. Along with increasing costs of tyres, insurance, tolls, maintenance, finance costs and statutory compliances, the viability of transport operations is under severe pressure,” one transporter told TOI.Transporters also argue that instead of repeated smaller hikes, a single transparent fuel pricing decision would allow better planning of freight structures and business viability.

Supply chains and deliveries

Rising fuel prices are also creating wider pressure across supply chains and delivery networks in the country. Logistics operations are under strain, with transporters already raising freight charges, a move that is expected to increase the cost of delivered goods, including essential items. At the same time, higher operating costs are affecting delivery schedules, reducing overall efficiency in supply chains and last-mile distribution systems.In several regions, reports suggest that a large number of vehicles are being kept idle as operating costs and challenges continue to rise, leading to estimated losses of nearly Rs 3,500 per vehicle per day in some sectors. The ripple effect is already visible, with disruptions in vehicle movement, pressure on supply chains, delayed deliveries, and growing strain on manufacturing, import-export activity, and the movement of essential commodities.

Household bills go up

Rising petrol and diesel prices are set to squeeze household budgets, making everyday expenses, from food delivery and groceries to dining out, more expensive. As fuel costs climb, transport-linked expenses across essential goods are also rising, adding to the burden on consumers and pushing up overall living costs. The impact is expected to deepen further, with inflationary pressures building across the economy. Your daily consumption basket: including staples, packaged foods and other essentials could get costlier in the months ahead as higher fuel prices feed into supply chain and input costs. The latest fuel price revision, amid ongoing Middle East tensions, is also likely to pressure FMCG companies, which may be left with limited options such as selective price hikes or reductions in product grammage, according to industry executives. Freight costs are set to increase distribution and input costs, further straining margins of companies already grappling with 8-10% inflation.“If fuel prices remain elevated over multiple quarters, companies may eventually resort to calibrated price hikes or grammage reductions, which could weigh on consumption recovery, particularly in price-sensitive rural markets’’ Naveen Malpani, partner and consumer & retail industry leader, Grant Thornton Bharat had told TOI.FMCG companies like Nestle, Hindustan Unilever, Marico and Dabur have seen demand recovery but are facing rising input costs and inflation pressures. To offset this, they have already taken 2–5% price hikes and may consider further increases along with cost-cutting measures.

Impact on economy

Finance minister Nirmala Sitharaman on Monday assured that India’s economy continues to show resilience on a broader note. “We should appreciate that the challenges are more externally driven. We must also recognise that India’s domestic economic situation remains positive and resilient even today,” the FM said.

At the same time, rising fuel prices have raised concerns about creating wider economic pressure as transportation costs feed into supply chains. This is increasing the cost of essentials, including fruits and vegetables, and adding inflationary pressure across sectors. The movement of goods, manufacturing activity, and import-export operations are all experiencing stress due to higher logistics costs and delivery disruptions.

OMC shares soar

Fuel price revisions have also influenced market activity. Shares of major oil marketing companies moved higher on Monday, with Hindustan Petroleum Corporation Limited (HPCL), Indian Oil Corporation (IOC), and Bharat Petroleum Corporation Limited (BPCL) all soared in green.IOC shares rose 4% to Rs 145, HPCL surged 6% to Rs 412.55, and BPCL advanced over 4.5% to Rs 309 on the BSE. The movement came as crude oil prices touched a two-week low amid signs of progress in US-Iran peace talks.Meanwhile, before the recent price hike, the government had been stepping in to help oil marketing companies (OMCs) manage the pressure from rising crude prices by cutting excise duties. Now, the FM highlighted, any reduction in excise duty on petrol and diesel would result in a revenue impact of around Rs 1 lakh crore.

What’s ahead for OMCs?

Earlier, in the absence of price hikes, oil marketing companies (OMCs) were facing heavy losses of up to Rs 1,000 crore per day. Now, with fuel prices rising by nearly Rs 7 per litre, the question is whether these losses will be reduced or not.The recent series of back-to-back price increases is expected to provide some relief to OMCs, but it is unlikely to fully offset their burden. Even if the situation in West Asia stabilises, uncertainty around the Strait of Hormuz is expected to persist for some time, keeping crude prices elevated, likely above $90 per barrel.At the same time, a weakening rupee continues to add pressure on margins. “Combined with a weakening rupee, this continues to pressure OMC margins, and they could still face under-recoveries. Going forward, some calibrated price revisions may be required. The government will need to balance OMC financial health against the impact on consumers,” Sourav Mitra, Partner – Oil and Gas, Grant Thornton Bharat told TOI.

3 F’s in focus

Finance minister Nirmala Sitharaman has also urged the country to focus on the 3 Fs, of fuel, fertiliser and forex. Apart from elevated crude oil prices, fertiliser costs have also surged to “unimaginable” levels, the FM noted, adding that high gold prices are creating additional challenges on the external front. She emphasised the need to focus on the “three Fs,” fuel, fertiliser and forex, pointing out that Prime Minister Narendra Modi’s recent appeals have been made in this context.Taken together, the latest fuel price revisions are no longer just a heavier cost at the petrol pump, they are beginning to ripple through daily lives. From transporters recalibrating freight rates and supply chains under strain, to households quietly tightening monthly budgets, the impact is gradually seeping into everyday life. With global crude trends still uncertain and geopolitical tensions far from settled, the outlook for fuel prices remains vulnerable to developments beyond the country.

Stock market rallied sharply on Monday, with the Sensex soaring more than 1,000 points and the Nifty reclaiming the 24,000 mark, as easing geopolitical tensions in West Asia and falling crude oil prices boosted investor sentiment globally.The 30-share BSE Sensex jumped 1,073.61 points, or 1.42 per cent, to close at 76,488.96, while the NSE Nifty 50 surged 312.40 points, or 1.32 per cent, to settle at 24,031.70.The rally came after optimism grew around a possible agreement between the United States and Iran, following remarks by US President Donald Trump over the weekend that a deal was “largely negotiated”.

Nifty50 top gainers

| Company Name | Current Price (Rs) | Price Change | % Change |

|---|---|---|---|

| Eicher Motors | 7,414 | 433.00 ↑ | 6.20% ↑ |

| Adani Ent. | 2,850 | 132.00 ↑ | 4.88% ↑ |

| Bajaj Finance | 941.90 | 25.40 ↑ | 2.77% ↑ |

| Tata Motors PV | 373.25 | 9.90 ↑ | 2.73% ↑ |

| L&T | 4,033 | 107.00 ↑ | 2.72% ↑ |

| HDFC Bank | 786.85 | 20.10 ↑ | 2.62% ↑ |

| Eternal | 247.67 | 5.72 ↑ | 2.37% ↑ |

| Bajaj Finserv | 1,807 | 41.40 ↑ | 2.35% ↑ |

| Kotak Bank | 392.85 | 8.71 ↑ | 2.27% ↑ |

| Shriram Finance | 961.95 | 21.00 ↑ | 2.23% ↑ |

Sensex top gainers

| Company Name | Current Price (Rs) | Price Change | % Change |

|---|---|---|---|

| Bajaj Finance | 941.90 | 25.40 ↑ | 2.77% ↑ |

| L&T | 4,033 | 107.00 ↑ | 2.72% ↑ |

| HDFC Bank | 786.85 | 20.10 ↑ | 2.62% ↑ |

| Eternal | 247.67 | 5.72 ↑ | 2.37% ↑ |

| Bajaj Finserv | 1,807 | 41.40 ↑ | 2.35% ↑ |

| Kotak Bank | 392.85 | 8.71 ↑ | 2.27% ↑ |

| ICICI Bank | 1,292 | 27.50 ↑ | 2.18% ↑ |

| SBI | 969.60 | 20.40 ↑ | 2.15% ↑ |

| Axis Bank | 1,311 | 25.80 ↑ | 2.01% ↑ |

| Titan Company | 4,159 | 79.40 ↑ | 1.95% ↑ |

Nifty50 top losers

| Company Name | Current Price (Rs) | Price Change | % Change |

|---|---|---|---|

| Max Healthcare | 1,001 | -22.40 ↓ | -2.19% ↓ |

| ONGC | 284.95 | -5.06 ↓ | -1.75% ↓ |

| Hindalco | 1,100 | -9.61 ↓ | -0.87% ↓ |

| Nestle India | 1,414 | -9.50 ↓ | -0.67% ↓ |

| Bajaj Auto | 10,491 | -58.50 ↓ | -0.56% ↓ |

| Infosys | 1,169 | -6.00 ↓ | -0.52% ↓ |

| TCS | 2,308 | -9.11 ↓ | -0.40% ↓ |

| Tata Consumer | 1,187 | -4.60 ↓ | -0.39% ↓ |

| HUL | 2,197 | -7.10 ↓ | -0.33% ↓ |

| Sun Pharma | 1,841 | -4.00 ↓ | -0.22% ↓ |

Sensex top losers

| Company Name | Current Price (Rs) | Price Change | % Change |

|---|---|---|---|

| Infosys | 1,169 | -6.00 ↓ | -0.52% ↓ |

| TCS | 2,308 | -9.11 ↓ | -0.40% ↓ |

| HUL | 2,197 | -7.10 ↓ | -0.33% ↓ |

| Sun Pharma | 1,841 | -4.00 ↓ | -0.22% ↓ |

| Kwality Wall’s | 26.33 | -0.06 ↓ | -0.19% ↓ |

Oil prices tumble as Iran deal hopes rise

Investor confidence improved as markets increasingly priced in the possibility of a diplomatic breakthrough between Washington and Tehran, which could lead to the reopening of the Strait of Hormuz and ease global energy supply concerns.According to news agency ANI, market expert Ponmudi R said optimism surrounding a potential US-Iran agreement revived risk appetite across global markets.“Investor sentiment improved significantly after Donald Trump stated over the weekend that a deal was ‘largely negotiated’, encouraging markets to increasingly price in the possibility of a near-term diplomatic resolution,” he said.He added that markets would look for the “successful implementation of a lasting peace agreement and the credible reopening of the Strait of Hormuz”.Brent crude prices dropped sharply below the $100 per barrel mark and were trading around $98 per barrel, down more than 5 per cent during the session.The Indian rupee also recovered strongly, gaining 48 paise to trade at Rs 95.21 against the US dollar after recent weakness.

Banking stocks lead market rally

Financial stocks led the gains on Dalal Street. Bajaj Finance, Larsen & Toubro, HDFC Bank, Eternal, Bajaj Finserv and Kotak Mahindra Bank emerged among the top Sensex gainers.Sectorally, Nifty PSU Bank rose 2.73 per cent, while Nifty Private Bank advanced 2.02 per cent, as per ANI. Nifty Auto climbed 1.66 per cent and Realty gained 1.54 per cent.However, FMCG stocks remained under pressure. Infosys, Tata Consultancy Services, Sun Pharma and Hindustan Unilever were among the laggards.

Global markets gain amid improving sentiment

Asian markets also ended higher on Monday amid improving global risk appetite. Japan’s Nikkei 225 surged 2.76 per cent, while Taiwan’s weighted index jumped 3.15 per cent.European markets were trading in positive territory, while US markets had settled higher on Friday.Meanwhile, Foreign Institutional Investors (FIIs) offloaded equities worth Rs 4,440.47 crore on Friday, according to exchange data.

Business

Gold price today: Yellow metal rises; check 24K, 22K city-wise rates in Delhi, Mumbai, Kolkata and more

Gold prices rose in futures trade on Monday, tracking gains in global markets amid growing optimism surrounding a possible peace agreement between the United States and Iran. Retail gold rates across major Indian cities also moved higher, with 22K, 24K and 18K prices recording gains compared to the previous day.On the Multi Commodity Exchange (MCX), gold contracts for June delivery climbed by Rs 426, or 0.27 per cent, to Rs 1,59,105 per 10 grams in a business turnover of 5,312 lots. As per PTI, analysts attributed the rise to a weaker US dollar and positive sentiment linked to the ongoing US-Iran negotiations.Gaurav Garg, research analyst at Lemonn Markets Desk, said easing crude oil prices and hopes of a peace deal supported bullion prices globally. In the international market, Comex gold futures for the June contract rose nearly 1 per cent to USD 4,590.62 per ounce in New York, as quoted by news agency PTI.Analysts also noted that hopes of easing tensions in West Asia have reduced fears of another inflationary spike driven by oil prices, supporting sentiment in precious metals markets.

City-wise gold rates today

Gold rate in Bengaluru today:Gold prices in Bengaluru have moved higher today. The 24K gold rate stands at Rs 15,938 per gram, while 22K gold is priced at Rs 14,610 and 18K at Rs 11,954 per gram, all up from yesterday’s levels.Gold rate in Delhi today:In Delhi, gold prices recorded gains across categories. The 24K gold rate is Rs 15,953 per gram, while 22K gold stands at Rs 14,625 and 18K at Rs 11,964 per gram.Gold rate in Mumbai today:Mumbai has also witnessed an increase in bullion prices. The 24K gold rate is Rs 15,938 per gram, while 22K and 18K gold are priced at Rs 14,610 and Rs 11,954 per gram, respectively.Gold rate in Chennai today:Gold prices in Chennai have risen sharply compared to other cities. The 24K gold rate stands at Rs 16,124 per gram, while 22K gold is at Rs 14,780 and 18K at Rs 12,400 per gram.Gold rate in Kolkata today:Kolkata has seen a rise in gold prices today. The 24K gold rate is Rs 15,938 per gram, while 22K gold is priced at Rs 14,610 and 18K at Rs 11,954 per gram.Gold rate in Hyderabad today:Gold prices in Hyderabad have edged higher. The 24K gold rate stands at Rs 15,938 per gram, while 22K and 18K gold are available at Rs 14,610 and Rs 11,954 per gram, respectively.Gold rate in Ahmedabad today:Ahmedabad has recorded gains in gold prices. The 24K gold rate is Rs 15,943 per gram, while 22K gold stands at Rs 14,615 and 18K at Rs 11,959 per gram.Gold rate in Jaipur today:In Jaipur, gold prices have moved up today. The 24K gold rate stands at Rs 15,953 per gram, while 22K and 18K gold are priced at Rs 14,625 and Rs 11,964 per gram, respectively.Gold rate in Bhubaneswar today:Gold prices in Bhubaneswar have increased from yesterday’s levels. The 24K gold rate is Rs 15,938 per gram, while 22K gold is at Rs 14,610 and 18K at Rs 11,954 per gram.Gold rate in Pune today:Pune has also witnessed higher bullion rates. The 24K gold rate stands at Rs 15,938 per gram, while 22K and 18K gold are priced at Rs 14,610 and Rs 11,954 per gram, respectively.Gold rate in Kanpur today:Gold prices in Kanpur have edged higher today. The 24K gold rate is Rs 15,953 per gram, while 22K gold stands at Rs 14,625 and 18K at Rs 11,964 per gram.

Bracket set, regionals begin May 29

A Swimmer Broke a World Record at the “Steroid Olympics”

Kyle Fletcher shows up to AEW Double or Nothing, beats down Konosuke Takeshita after international title win

-

Tech1 week ago

Tech1 week agoWhy Is Your Grill So Dumb? The Best Grills Set Temp Like an Oven

-

Tech1 week ago

Tech1 week agoThis Solar-Powered Smart Sprinkler Keeps My Lawn Watered Without Any Power Cables

-

Fashion4 days ago

Fashion4 days agoICE cotton sees mixed trend as rain forecasts weaken sentiment

-

Fashion5 days ago

Fashion5 days agoUS cotton planting advances to 41%, concerns persist in Texas

-

Fashion1 week ago

Fashion1 week agoTurkiye’s current account deficit expected to widen in 2026: Minister

-

Fashion1 week ago

Fashion1 week agoIndia’s Pearl Global’s FY26 revenue crosses $521 mn milestone

-

Entertainment1 week ago

Entertainment1 week agoPrincess of Wales praised as ‘step ahead’ of royal family

-

Sports5 days ago

Sports5 days agoTodd Monken says Shedeur Sanders has ‘come miles’ as Browns quarterback competition heats up