Business

Eye-popping rise in one year: Betting on just gold and silver for long-term wealth creation? Think again! – The Times of India

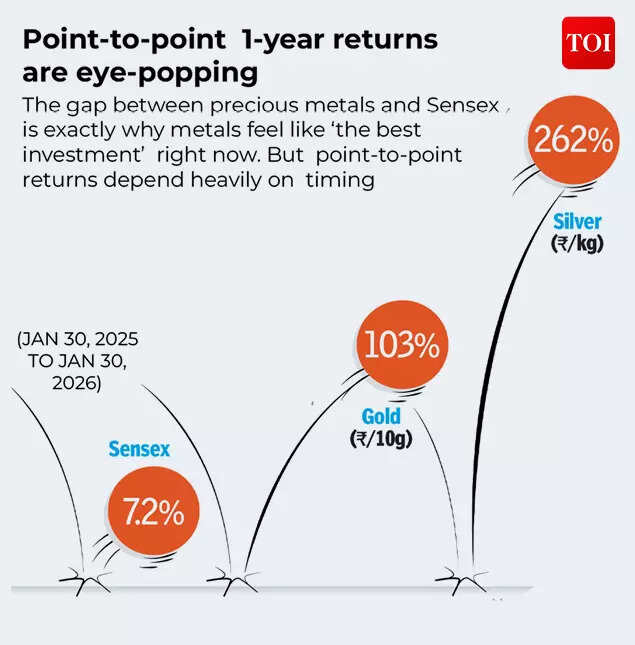

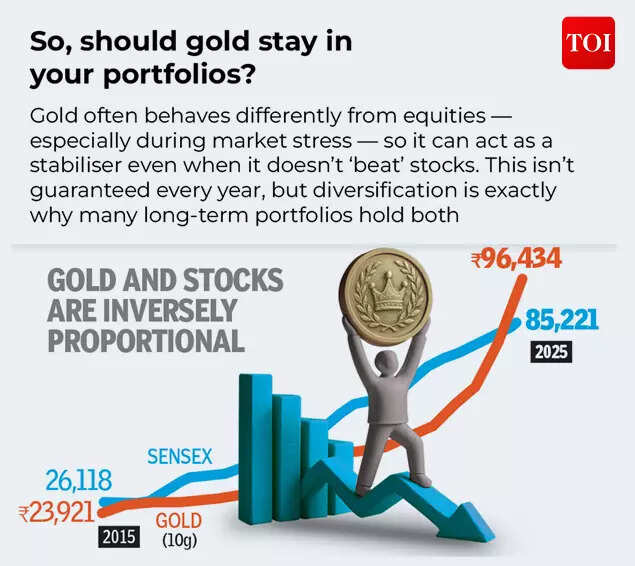

Gold and silver have delivered eye-popping returns over the last one year. In contrast, Sensex and Nifty have delivered a muted performance. Gold and silver have already delivered an exceptional run over the past year, with silver posting gains of around 160% and gold posting over 80% gains domestically in 2025. Over the past one year, precious metals have clearly outpaced equities. Gold in India is hovering around Rs 1.55–1.60 lakh per 10 grams and silver is near Rs 2.60–2.70 lakh per kg after a sharp rally driven by geopolitical tensions, strong central bank buying, inflation concerns and currency weakness. In comparison, the Nifty 50 and Sensex have delivered relatively moderate single-year returns, reflecting a more measured earnings environment.This has prompted investors to wonder if their portfolios should be oriented more towards gold and silver, than equities. But gold and silver have also seen a brutal selloff in the recent weeks, dropping from their record highs, though the precious metals are still sitting on decent returns. Before you make the decision on which asset class to invest in, experts believe it’s prudent to look at historical data to understand how returns in gold, silver and equities shape up over longer time periods.

Gold, silver, stocks: How do the returns compare over a 1-year, 5-years, 10-years time period?

A commonly asked question in the minds of investors is: where should the hard earned money be put to earn the best returns? Over a 1-year, 5-year and 10-year time period, which asset class has offered the highest returns – gold, silver or equities?Looking at performance across time periods gives useful perspective, and a deeper understanding into investments should ideally be allocated.According to Somil Mehta, Head of Retail Research at Mirae Asset Sharekhan, equity markets tend to be volatile. Stocks can outperform sharply in good years, but also see corrections. Gold and silver usually provide stability, especially during global uncertainty, he tells TOI.Over a 5-year time frame, equities (Nifty and Sensex) generally outperform precious metals, supported by earnings growth and economic expansion. Gold performs well during risk-off phases, while silver remains more volatile, Mehta says.However, according to Mehta, over a decade, equities clearly emerge as the strongest wealth creators. Gold delivers steady returns, acting more as a hedge than a growth asset. Silver’s performance is uneven due to its industrial demand cycle.

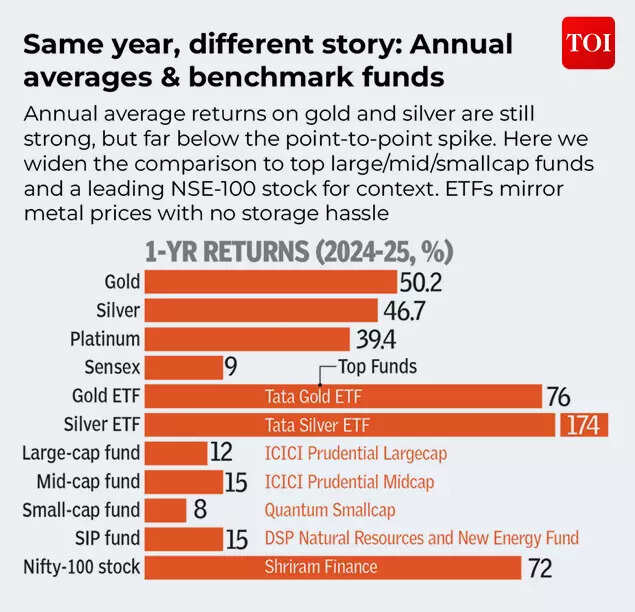

Experts note that the last one year has been an outlier for precious metals as they significantly outperformed equities, with silver and gold delivering strong gains amid safe-haven demand due to global trade concerns (US tariffs) and geopolitical uncertainty, while Nifty returns remained relatively muted. An analysis by TOI on gold, silver and stock markets over various time-frames notes that annual averages smooth out the ups and downs within the year — closer to how most people actually experience prices.

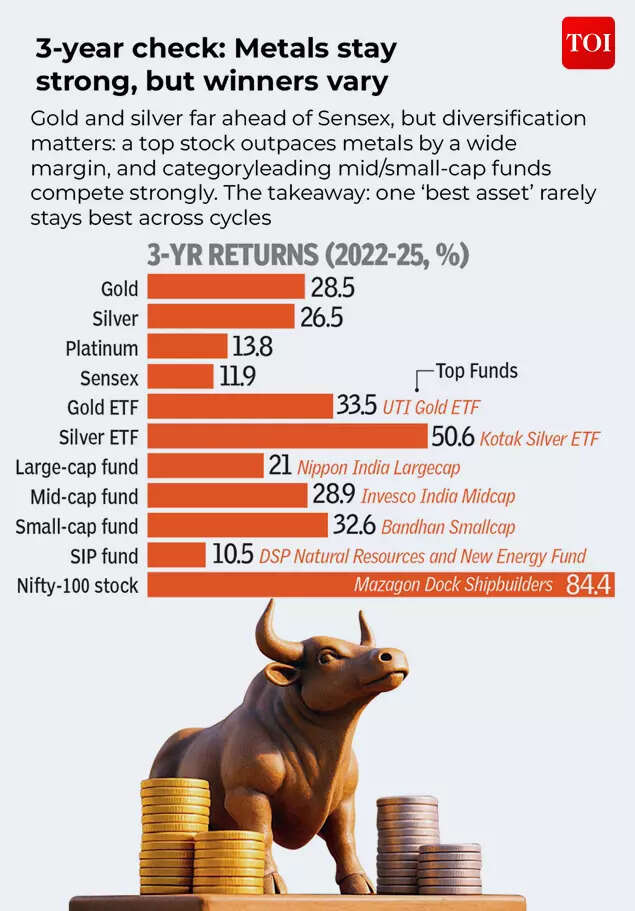

On a 3-year horizon check the TOI analysis notes: “A top stock outpaces metals by a wide margin, and category-leading mid/small-cap funds compete strongly. The takeaway: one ‘best asset’ rarely stays best across cycles.”

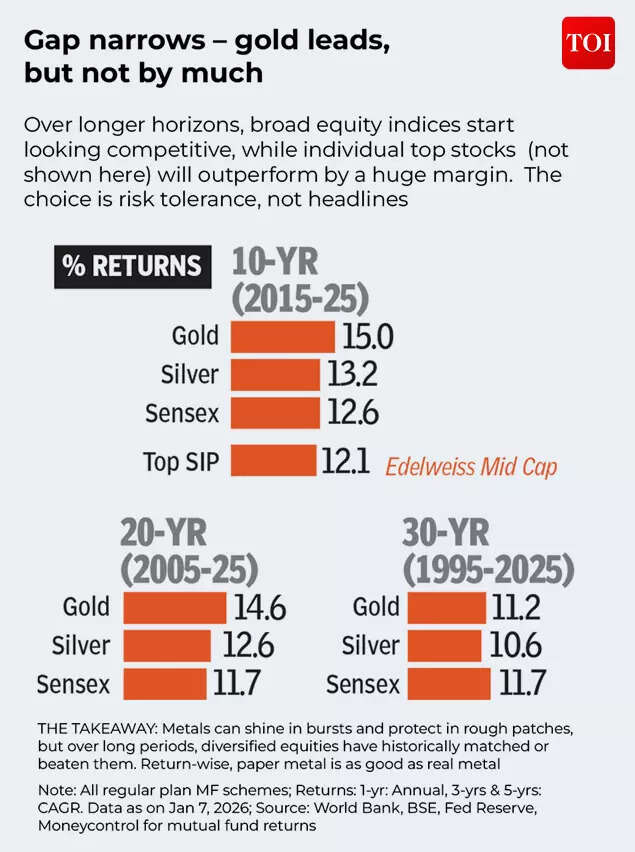

For a 5-year period the winners look different: strong equity funds (mid/small-cap leaders near the high-20s CAGR) look better than metals, and the top-performing NSE-100 stock is in a different league. Message: metals can be easy; equity wealth often comes from riding volatility, says the TOI analysis.

Akshat Garg, Head of Research and Product at Choice Wealth notes that when the time frame is expanded, equities continue to demonstrate the power of compounding. “Businesses grow revenues, expand margins and reinvest profits, which creates sustainable wealth over long periods. Gold and silver, on the other hand, do not generate earnings; they primarily act as stores of value and crisis hedges. They outperform during uncertainty, but over full economic cycles equities tend to lead,” he tells TOI.

Will gold and silver outperform stock markets in 2026 as well?

According to Somil Mehta, Head of Retail Research at Mirae Asset Sharekhan, this year equities are likely to outperform precious metals, provided economic growth remains stable.“Gold may deliver moderate returns if global uncertainty, geopolitical risks, or currency volatility persist. Silver could underperform gold due to higher volatility and dependence on industrial demand,” he tells TOI.However, Maneesh Sharma, AVP – Commodities & Currencies, Anand Rathi Shares and Stock Brokers still sees gold and silver outperforming equites.“As far as equity outlook is concerned, fundamental growth numbers remain crucial for the current year. This is evident from the fact that as the Nifty’s price-to-earnings (P/E) ratio hovers around 22.5 as of mid-February 2026, it trades near its 3-year average of 25.2x, but with the Sensex P/E exceeding its 15-year average, it leaves little room for multiple expansion without fundamental earnings acceleration. Hence cautious optimism persists for Nifty returns this year,” he tells TOI.“Gold & Silver are still expected to outperform equities amid persistent global uncertainties, including geopolitical tensions & structural imbalances in developed economies leading to growing deficits. Central bank demand remains a bullish pillar for gold prices, with many central banks indicating plans to increase their holdings this year although pace of increase is expected to moderate,” he says.While anticipating a good year for gold and silver, Sneha Poddar, VP-Research, Wealth Management, Motilal Oswal Financial Services sees equities giving a 10% return.“Broader commodities space, especially precious metals, could continue to stay resilient in 2026, though not in a one-way rally like last year; instead, may see phases of consolidation with the price levels subject to revision as per evolving macro and liquidity conditions,” she says.The expert anticipates that equities will return to the forefront with an expected 10% price return for Nifty over one year, considering improving earnings trajectory with PAT expected to grow at around 12% CAGR over FY25-27E. “We anticipate improved earnings growth, given the supportive domestic policies (both fiscal and monetary) and strengthening global trade opportunities following recent announcements of trade deals (US, EU) and foreign trade agreements,” she told TOI.Akshat Garg, Head of Research and Product at Choice Wealth sees volatility in the prices of gold and silver this year. “Metals may remain supported if global risks and liquidity trends persist, but after a strong rally volatility cannot be ruled out,” he says.“The bigger lesson for investors is that leadership rotates. Instead of chasing the recent outperformer, diversification and disciplined rebalancing work better,” he tells TOI.Taking a different view, Jateen Trivedi, VP Research Commodity, LKP Securities sees both gold and silver performing due to ongoing global uncertainties. “Given continued geopolitical tensions, trade uncertainties, currency volatility, and sustained central bank buying, bullion may remain structurally supported into 2026. At the same time, equity markets could face sectoral challenges, particularly from global AI disruption and earnings pressures,” Trivedi tells TOI.Broadly he sees gold in the Rs 1,75,000 – Rs 1,85,000 range; silver in the Rs 3,00,000 – 3,25,000 range and Nifty at around 27,000 (assuming no major geopolitical escalation).“Metals may continue to outperform if uncertainty persists, though volatility will remain high,” he says.

Time is a greater teacher: What’s the biggest lesson?

The biggest lesson from the historical performance of gold, silver and equities is clear: don’t chase the recent winner, don’t bet blindly on last year’s outperformer!“This is perhaps the oldest mistake in investing, and also the most common. Investors who rushed into silver after its 2025 rally are taking on far more risk than they realise. Those who ignored gold for years before 2025 paid a price too. The data across decades tells us clearly: no single asset stays on top forever,” says InCred Money.Somil Mehta, Head of Retail Research, Mirae Asset Sharekhan

- No single asset wins every year.

- Equities create long-term wealth, but gold protects portfolios during uncertainty.

- Timing markets is difficult, asset allocation matters more than asset selection

For a 5-10 year time horizon, Somil recommends a portfolio that has 55-65% in equities (focus on quality large caps and structural sectors); 10-15% for gold and silver with gold as the main hedge; 20-30% in debt or fixed income for stability and liquidity.Somil Mehta says: “Equities remain the best long-term wealth creator, while gold plays a supporting role. A balanced portfolio, not chasing short-term winners, is the most reliable way to build wealth over time.”For Sneha Poddar of MOFSL the sure-shot way to win in the long-term is that investing ultimately hinges on discipline, diversification and a clear understanding of the asset class.

Source: Anand Rathi Shares & Stockbrokers“While metals often outperform during volatile macro phases, equities deliver steadier returns and should remain the core long-term allocation, with gold and silver serving as strategic hedges within a well-balanced portfolio,” she says.“For a balanced and relatively stable portfolio, gold should ideally carry a slightly higher weight than silver depending on investors risk profile and tenure of investment. Therefore, portfolios can ideally comprise 85-90% equities and 10–15% gold/silver. Over longer periods, equities historically deliver steady wealth creation, while metals act as portfolio stabilisers rather than return drivers,” she says.Akshat Garg of Choice Wealth is of the view that a portfolio with roughly 60–70% equities, 20–30% debt and 5–10% allocation to gold and silver offers a balanced blend of growth, stability and protection for a 5-10 year time period.The important thing to understand is that equities, metals, bonds — all carry cycles of outperformance and correction. “The key lesson is diversification. Chasing recent winners without balance increases portfolio risk. A balanced mix helps capture upside while managing long-term volatility,” says LKP Securities’ Jateen Trivedi.InCred Money notes that there is no one-size-fits-all allocation, but a simple rule of thumb is this: over a 5-year horizon, lean balanced, around 50–60% equities and 40–50% high-quality fixed income, so you participate in growth without exposing near-term goals (like a home down payment or business capital) to excessive volatility. Over a 10-year horizon, you can afford to tilt more toward growth, 60–75% equities and the rest in bonds or other stable assets, because time smooths out market cycles and compounds returns. The real driver is your risk appetite and goal clarity: if a 15–20% drawdown keeps you up at night, dial down equities; if your goals are long-term wealth creation and you can stay invested through volatility, lean into growth. Allocation should protect your sleep first, and then grow your wealth, says InCred Money.As InCred Money concludes: Gold is your safety net. When stock markets fall, gold tends to hold its ground or rise. It doesn’t make you rich overnight, but it protects what you already have. Silver is more of a wild card, unfortunately, because of speculators. It can shoot up in good times, but it can fall just as hard. Stocks, over time, are the real wealth builders, but they demand patience.The investor who wins over the long run is rarely the one who picked the hottest asset of the year. It’s the one who stayed diversified, stayed calm, and didn’t let headlines drive their decisions.(Disclaimer: Recommendations and views on the stock market, other asset classes or personal finance management tips given by experts are their own. These opinions do not represent the views of The Times of India)

: Sensex jumps 609 points, Nifty nears 24,200-Check top gainers and losers today – The Times of India")

: Nifty50 & Sensex surge nearly 4%-which are the top gainers and losers today? Check stock list – The Times of India")

UK high streets and shopping destinations are showing signs of recovery as more than 13 retail stores opened each week over the past year, according to new figures.

However, England and Wales have still seen more than 6,000 retail premises vanish from local communities over the past five years.

Analysis of Valuation Office Agency data by tax firm Ryan, found that there were 507,810 retail premises across England and Wales at the end of 2025.

It said the figures showed that a recent contraction across the sector has appeared to stabilise, with a 723 net increase in the number of retail stores compared with a year earlier.

Property numbers increased across every region of England and Wales, with the exception of the North West, which saw a decline of 41.

It suggests that parts of the sector are now beginning to rebalance following significant structural contraction seen since the pandemic.

The creation of new retail units also comes as many retail real estate firms, such as Hammerson, have turned empty large units, often former department stores, into a greater number of smaller units.

Other retail groups, such as John Lewis, have moved away from ambitions to transform some retail property for other uses such as rental accommodation.

Nevertheless, the retail sector is still facing pressure from higher business rates for many firms, increased labour costs and concerns over consumer sentiment.

The data also shows that there has also been significant decline over the past few years, with a net reduction of 6,045 retail properties since the end of 2020.

London recorded the largest five-year regional reduction, with 1,266 retail premises disappearing over the period, followed by the South East (-1,191), North West (-719) and North East (-672).

The figures show retail premises which have permanently disappeared from communities altogether, having either been demolished or converted for alternative use.

The figures come as Ryan’s 2026 annual business rates review highlighted that the retail sector saw a 9.3% increase in rateable values at the 2026 business rates revaluation despite the major shift in the retail landscape since the pandemic.

Alex Probyn, practice leader for Europe and Asia-Pacific property tax at Ryan, said: “The pandemic accelerated structural changes that were already emerging across the retail sector, including changing consumer behaviour, hybrid working patterns and a reduced reliance on traditional retail floorspace in many locations.

“Many locations were arguably over-retailed before Covid and high streets have evolved towards more mixed-use environments, with retail space being rebalanced alongside growing demand for residential, leisure, hospitality and service-led uses.

“The revaluation outcome does suggest a large proportion of retail premises have seen bigger increases in their assessments than underlying market conditions and rental evidence would have led occupiers to expect.

“Retailers should therefore carefully review and, where appropriate, challenge their assessments.”

Indians sharply cut back on overseas travel spending in March, with remittances for foreign trips dropping by more than $212 million from the previous month, according to Reserve Bank of India data. The fall in outbound travel expenditure came amid rising oil prices linked to the Middle East conflict and persistent pressure on rupee, even as travel remained the single largest component of outward remittances under the Liberalised Remittance Scheme (LRS).In March, travel-related remittances fell to $1.09 billion from $1.3 billion in February and $1.65 billion in January. The decline came at a time when the West Asia conflict pushed oil prices higher and weakened rupee to record lows. Amid the situation, Prime Minister Narendra Modi urged citizens to cut down on foreign travel and adopt measures such as carpooling. Lower overseas travel spending could reduce foreign exchange outflows and help ease pressure on rupee.According to the RBI’s data on outward remittances by resident individuals, travel continued to account for the largest share of money sent abroad under the LRS in March. Total remittances during the month stood at $2.59 billion.The RBI tracks overseas spending across categories including travel, studies abroad, maintenance of close relatives, overseas investments, and property purchases. Under the LRS framework, resident individuals, including minors, can remit up to $250,000 in a financial year for permitted current or capital account transactions.Within the travel segment, the biggest component remained the ‘other travel’ category, which covers holiday spending and international credit card settlements. Indians spent $623.05 million under this category in March, accounting for nearly 57 per cent of total travel-related remittances during the month.Expenditure linked to education travel, including hostel and fee payments, stood at $450.16 million. Business travel, pilgrimage, and overseas medical treatment together accounted for $21.39 million.The data also showed a rise in remittances meant for the maintenance of close relatives abroad. Such transfers increased to $389.78 million in March from $266.18 million in February.At the same time, spending under the ‘studies abroad’ category declined. This category includes payments made for educational services accessed remotely without travelling overseas, such as correspondence courses. Remittances under this head stood at $151.71 million in March, compared to $175.68 million in February and $267.42 million in January.For the financial year 2024-25, Indians remitted a total of $29.56 billion under the LRS. Travel made up the largest portion of this amount at $16.96 billion.The RBI figures further showed that investments by Indians in overseas equity and debt instruments rose significantly to $440.22 million in March from $265.99 million in February.Meanwhile, outward remittances for the purchase of immovable property overseas declined to $38.68 million in March, down from $51.36 million a month earlier.

Gold and silver are expected to take cues from developments in the ongoing US-Iran talks this week, with analysts forecasting a largely steady trend for gold prices while silver may continue to outperform amid geopolitical tensions and elevated crude oil prices.Investors are also likely to track a series of economic indicators from the United States, including GDP data, housing numbers, consumer confidence figures and the Personal Consumption Expenditure (PCE) inflation print, as markets look for signals on the Federal Reserve’s next policy move.“Gold price momentum next week looks sideways, while silver still looks positive as focus will again be on the peace negotiations between the US and Iran to end the war,” said Pranav Mer, Vice President, EBG – Commodity & Currency Research, JM Financial Services Ltd.Trading activity in domestic commodity futures markets will be curtailed on Thursday morning due to Bakri Id.On the MCX, gold futures ended the previous week at Rs 1.58 lakh per 10 grams after posting marginal gains, while silver futures settled lower at Rs 2.71 lakh per kilogram.“Gold traded in a range-bound manner last week, posting marginal gains of around 0.40% on the MCX to close near Rs 1,58,670 per 10 grams,” said Jateen Trivedi, VP Research Analyst – Commodity and Currency, LKP Securities.He noted that crude oil prices witnessed heavy profit booking during the week and corrected nearly 7% from recent highs, easing concerns around inflationary pressure globally.“At the same time, the rupee recovered from weaker levels of 97 against the US dollar to strengthen near 95.70, which limited upside momentum in domestic gold prices despite stable international bullion trends,” Trivedi added.In international trade, Comex gold futures closed the week 1% lower at $4,523.2 per ounce. Silver futures also weakened, slipping nearly 2% to $76.20 per ounce.“Gold prices moved in a consolidative range over the past few sessions, but ended the week with a marginal loss. Prices were steady amid a lack of fresh direction in the market — be it on the economy front or the US-Iran war front,” Mer said.According to analysts, uncertainty surrounding the geopolitical situation has continued to keep markets on edge, particularly as statements from both Washington and Tehran have frequently shifted.On Sunday, US President Donald Trump said that an agreement between the US and Iran aimed at reducing tensions in the Gulf region and reopening the Strait of Hormuz was close to being finalised.Posting on Truth Social, Trump said the deal had been “largely negotiated” and that only final formalities remained.However, Iranian media disputed Trump’s remarks regarding the full reopening of the Strait of Hormuz, stating that Tehran would continue to maintain control over the key waterway.Analysts said the contrasting positions from both sides are likely to keep bullion prices sensitive to any fresh headlines emerging from the region.Meanwhile, market participants are also expected to monitor comments from Federal Reserve officials after Kevin Warsh formally succeeded Jerome Powell as head of the US central bank on Friday during a period of geopolitical tensions, market volatility and persistent inflation pressures.

Gordon Ramsay reveals ‘most important thing in life’

Shop numbers return to growth after years of decline, say experts

Drake sets new record at ‘Iceman,’ ‘Habibti’ and ‘Maid of Honour’

-

Entertainment1 week ago

Entertainment1 week agoWhere Pete Davidson, Elsie Hewitt stand after breakup: Details revealed

-

Politics1 week ago

Politics1 week agoRising diesel costs from Iran war strain US school budgets

-

Tech1 week ago

Tech1 week agoWhy Is Your Grill So Dumb? The Best Grills Set Temp Like an Oven

-

Tech1 week ago

Tech1 week agoThis Solar-Powered Smart Sprinkler Keeps My Lawn Watered Without Any Power Cables

-

Fashion1 week ago

Fashion1 week agoRMG trade bodies seek policy support from Bangladesh PM

-

Fashion1 week ago

Fashion1 week agoIndia calls for aligning standards, customs procedures with Africa

-

Fashion6 days ago

Fashion6 days agoNigeria Kwara Garment Factory, KWS Garment Production Village ink pact

-

Sports1 week ago

Sports1 week agoPakistan steady after Das ton | The Express Tribune