Business

GST revamp: What are the latest tax rates on cars, gold, mobile phones, EVs, cigarettes? Check details – The Times of India

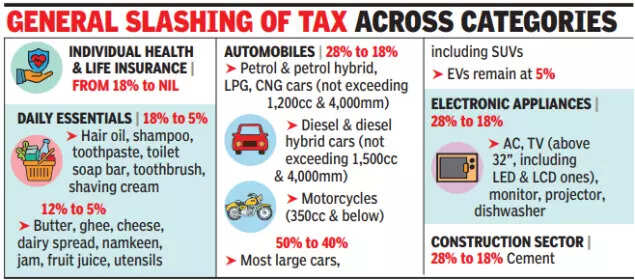

The Goods and Services Tax (GST) Council, chaired by Union finance minister Nirmala Sitharaman, on Wednesday announced the most extensive revamp of the indirect tax system since its rollout in 2017.The reform introduces a simplified two-slab structure of 5% and 18%, alongside a new 40% slab for luxury and sin goods.The new rates, except for tobacco where cess continues, take effect from September 22, the first day of Navratri.

Revenue secretary Arvind Shrivastava estimated the net fiscal implication of the changes at Rs 48,000 crore. He added the measures are designed to spur consumption and improve compliance.

Sitharaman underlined that the reforms were aimed at the common man, stating, “Every tax levied on common man’s daily use items have undergone a rigorous look, and in most cases, the rates have come down drastically”.

Cars

Buyers of small cars stand to benefit the most. Small cars will now attract 18% GST, reduced from the earlier 29% (28% plus 1% cess).For GST purposes, small cars are defined as petrol, LPG or CNG vehicles with an engine capacity of up to 1200 cc and length up to 4000 mm. In the case of diesel cars, the definition covers vehicles with engine capacity up to 1500 cc and length not exceeding 4000 mm.Large vehicles exceeding 1500 cc or longer than 4000 mm will fall into the new 40% GST slab.The same rate will also apply to all utility vehicles, including SUVs, MUVs, MPVs and cross-over vehicles, provided they have an engine capacity above 1500 cc, a length over 4000 mm, and a ground clearance of 170 mm or more.Unlike the earlier regime that combined 28% GST with a 17–22% cess, the new framework consolidates this into a single 40% rate without cess.

Bikes

Two-wheelers have also seen a rationalisation. Motorcycles up to 350 cc engine capacity will attract 18% GST, reduced from 28%. The 18% rate also applies to 350 cc models.Motorcycles exceeding 350 cc engine capacity have been placed in the 40% bracket, aligning them with the treatment of luxury and high-powered vehicles.This change is expected to encourage mass-market two-wheeler sales, especially in rural and urban middle-class markets, while continuing to tax premium motorcycles at a higher rate.

Electric Vehicles

Electric cars remain unchanged, continuing to be taxed at 5%.

Health Insurance

A major relief comes for individuals purchasing life and health insurance. These policies will now be exempt from GST. Earlier, these services attracted 18%, adding to premium costs.Exemption is expected to make policies more affordable, widening insurance coverage in a country where penetration levels remain low.

Cigarettes and tobacco

The GST Council has shifted cigarettes, cigars, pan masala, and chewing tobacco into the 40% slab. However, until compensation cess loans are fully repaid, the existing 28% GST plus cess regime will continue.Analysts noted that revenue neutrality is a priority for the government, as cigarette taxation contributes significantly to exchequer inflows. The move balances public health concerns with the need to curb illicit trade.

Alcohol

Alcohol remains outside the purview of GST altogether. It continues to be taxed separately through state excise duties, meaning the GST overhaul has no bearing on alcohol pricing.States will retain autonomy in setting alcohol taxes, a key revenue source for their budgets.

Gold

There has been no change in the taxation of precious metals. Gold and silver jewellery remain taxed at 3%, with an additional 5% GST on making charges. Gold bars and coins also continue to face 3% GST.With no direct impact from GST 2.0, demand in the bullion market is expected to remain steady, especially during the festive season when purchases peak.

Mobile Phones

Despite repeated industry requests, mobile phones remain taxed at 18%. ET reported that the India Cellular and Electronics Association (ICEA) had sought a 5% slab, calling the current levy “regressive” and reminding that pre-GST state VAT on mobiles was mostly capped at 5%.Despite the wider rate cuts across consumer goods, mobile phones remain at 18% GST, unchanged under the new regime. As per ET, the India Cellular and Electronics Association (ICEA) had urged for a 5% slab, calling the current levy “regressive.”The industry argued that mobile phones are a basic digital necessity, not a luxury.ICEA highlighted that pre-GST, most states had capped VAT at 5%. With domestic production rising to Rs 5.45 lakh crore in FY25 and exports crossing Rs 2 lakh crore, industry bodies stressed that lower GST would have boosted affordability and domestic demand.

Gold prices in Pakistan have risen again at the start of the business week after several days of decline, according to the All Pakistan Bullion Market.

The price of gold per tola increased by Rs 800, reaching Rs 493,962.

Similarly, the price of 10 grams of gold rose by Rs 686 to Rs 423,492.

In the global market, gold also recorded an increase of $8 per ounce, reaching $4,716.

Experts say global economic uncertainty, currency fluctuations, and investor preference for safe-haven assets are driving the upward trend in gold prices.

They add that changes in international markets directly impact Pakistan’s local bullion rates, leading to continued fluctuations in domestic prices.

Now one of the biggest sportswear firms, Anta’s rise follows a playbook adopted by many Chinese giants.

Source link

Business

Gold price prediction today: Will gold prices continue to be volatile? Key levels to watch out for April 27, 2026 week – The Times of India

Gold price prediction today: Gold prices will closely track movements on the rate decisions by several central banks, including the US Federal Reserve, this week, says Manav Modi, Senior Analyst, Commodity Research at Motilal Oswal Financial Services Ltd.Gold is currently consolidating after sharp swings in a broad range, indicating a pause rather than a reversal. Price action shows a higher-high structure intact, but the recent sideways movement suggests indecision near the upper supply zone around 158,000–160,000. The formation resembles a short-term flag/triangle continuation pattern, where a breakout on either side will define the next directional move. Volume has tapered slightly, reinforcing the consolidation narrative.Gold prices recently moved from the upper band toward the mid-band (20 DMA), and are now attempting to stabilize. The bands have started to contract, signaling a potential volatility expansion ahead. Sustaining above the mid-band (~150,500–151,000 zone) keeps bullish bias intact, while a breakdown below this could trigger a deeper mean reversion toward the lower band.For the week, immediate support for gold prices is placed at around Rs 150,500, which is followed by stronger support near Rs 148,500. On the upside, the resistance stands at around Rs 155,500, and after that the key supply zone is at Rs 158,000. A decisive close for gold above Rs 158,000 levels can then resume the broader uptrend. However, a break in gold prices below levels of Rs 148,500 may shift the momentum to bearish in the near term.The economic docket is filled with data points and events this week as the focus will be on FED, BOJ, ECB and ECB policy meetings. US consumer confidence, GDP, inflation and durable goods orders data will also be in radar.(Disclaimer: Recommendations and views on the stock market, other asset classes or personal finance management tips given by experts are their own. These opinions do not represent the views of The Times of India)

SBP raises policy rate by 100bps to 11.5% as inflation risks mount

Finalise Bangladesh’s textile-RMG circular economy strategy: Experts

Gold prices rise rebound in Pakistan after recent decline – SUCH TV

-

Sports1 week ago

Sports1 week agoWWE WrestleMania 42 Night 2: Live match results and analysis

-

Sports1 week ago

Sports1 week agoNCAA men’s gymnastics championship: All-time winners list

-

Fashion1 week ago

Fashion1 week agoUK’s Sosandar returns to profitability amid robust FY26 performance

-

Politics6 days ago

Politics6 days agoUK’s Starmer seeks to deflect blame over Mandelson appointment

-

Entertainment7 days ago

Entertainment7 days agoLee Anderson, Zarah Sultana kicked out of UK Parliament for calling PM ‘liar’

-

Business1 week ago

Business1 week agoNo fuel shortage: Govt assures 100% domestic LPG, PNG, CNG supply amid Hormuz energy crunch – The Times of India

-

Business7 days ago

Business7 days agoHow Trump’s psychedelics executive order could unlock stalled cannabis reform

-

Business1 week ago

Business1 week agoExercise to test response to offshore energy threat involving vessels and drones