Business

The electric question | The Express Tribune

PUBLISHED

September 21, 2025

KARACHI:

The afternoon sun beats down on Karachi’s Shahrah-e-Faisal as traffic locks into yet another jam. In an old sedan, a driver taps the steering wheel, eyes fixed on the blinking fuel gauge. At more than Rs. 270 a litre, every refill feels heavier than the last. A few lanes over, a plug-in hybrid electric vehicle (PHEV) glides forward almost noiselessly, its driver unbothered by the stop-and-go grind, knowing most of the ride will cost only a fraction in electricity.

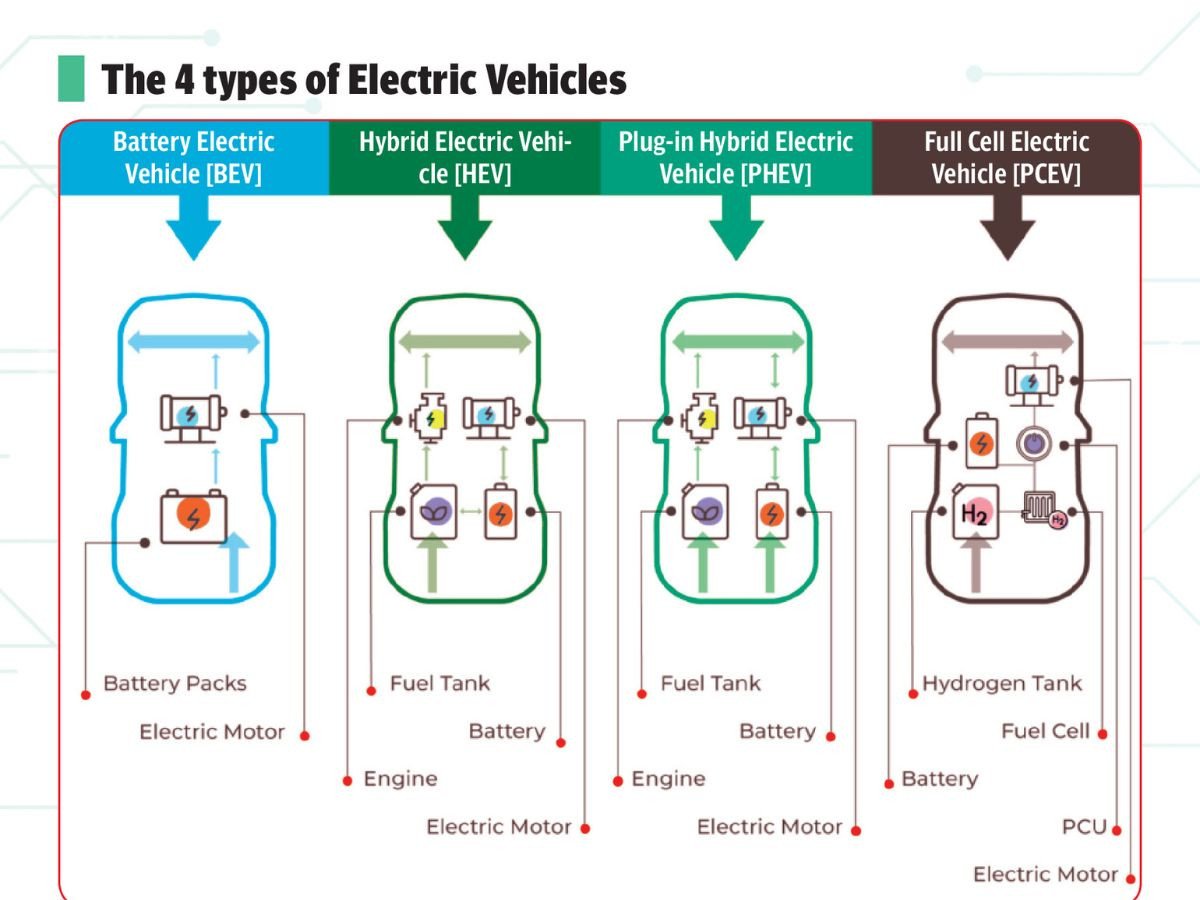

This quiet contrast says a lot about where Pakistan finds itself. In cities like Karachi and Lahore, congestion is a way of life and the rising price of petrol has become a private calculation in every household. The fumes from endless traffic only add to skies already thick with smog. It is here that New Energy Vehicles (NEVs), a category that includes both plug-in hybrids (PHEVs) and fully electric cars (EVs), are being looked at as more than just cars. They promise relief for wallets as well as for the air people breathe.

Elsewhere, this shift has been years in the making. In the beginning, electric cars were more of a novelty. They were costly, clunky, and could not go very far on a single charge. It was only after battery technology improved that the shift began. By the mid-2000s, companies like Tesla in the US and BYD in China started to change perceptions.

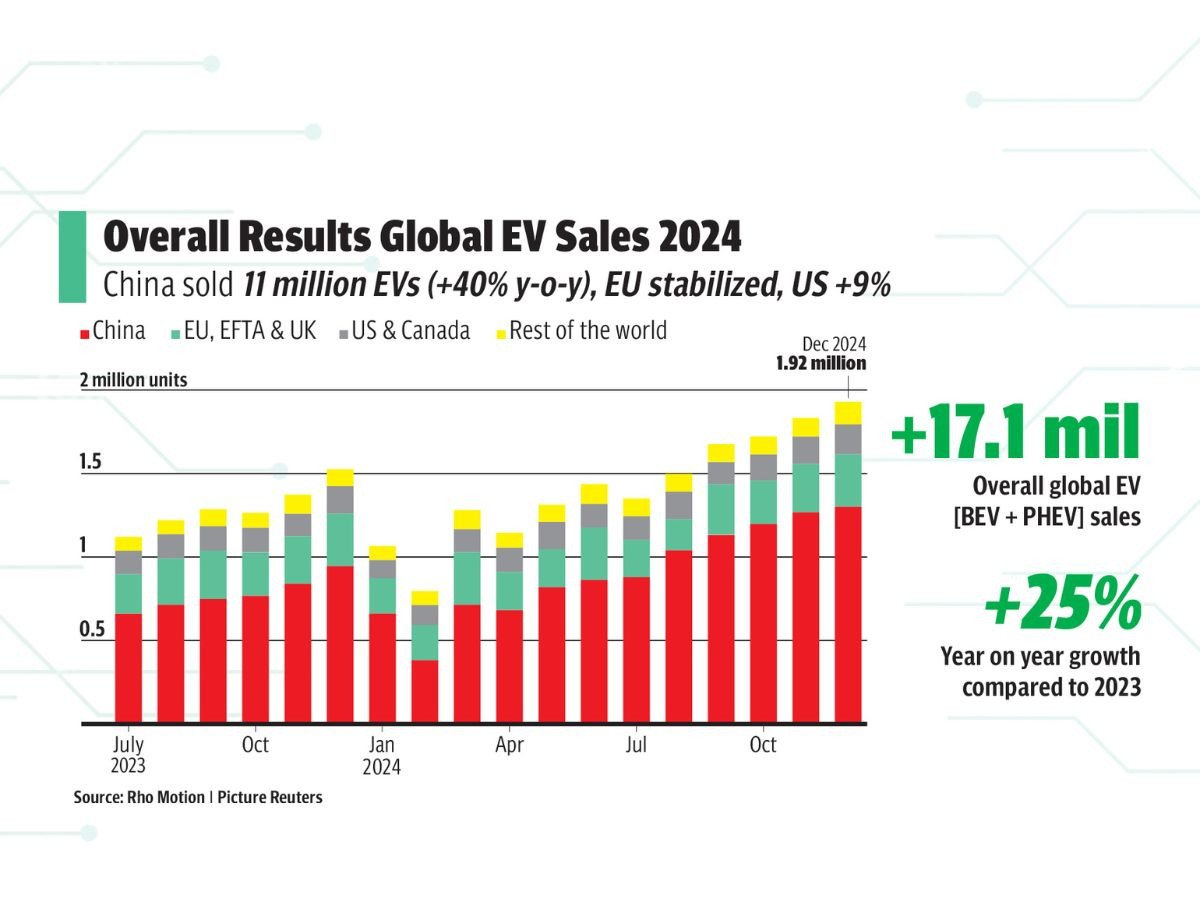

Governments in Europe and Asia added fuel to the push by offering incentives and building charging networks. The result was a global surge. In 2024 alone, more than 17 million electric and plug-in hybrids were sold, and in places like China, Norway and Germany, electric cars now account for a significant share of the market.

Pakistan is late to the curve. Policy papers now talk of 30 per cent of new cars being electric by 2030, yet on the streets petrol still rules. Charging stations remain rare, and EVs are mostly limited to wealthier buyers. Even so, the entry of global players and the slow trickle of PHEVs onto Pakistani roads suggest the story of the country’s auto market may be about to change.

The global promise of NEVs

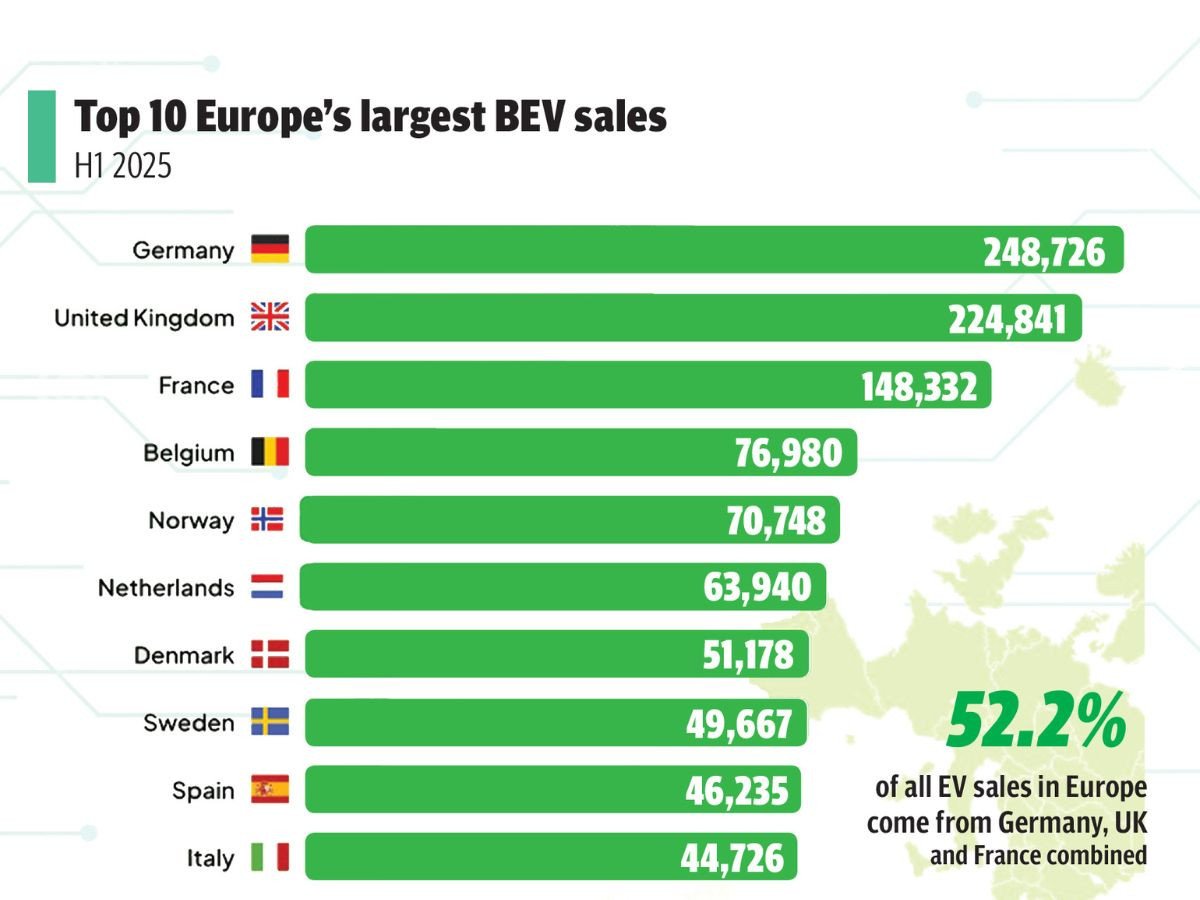

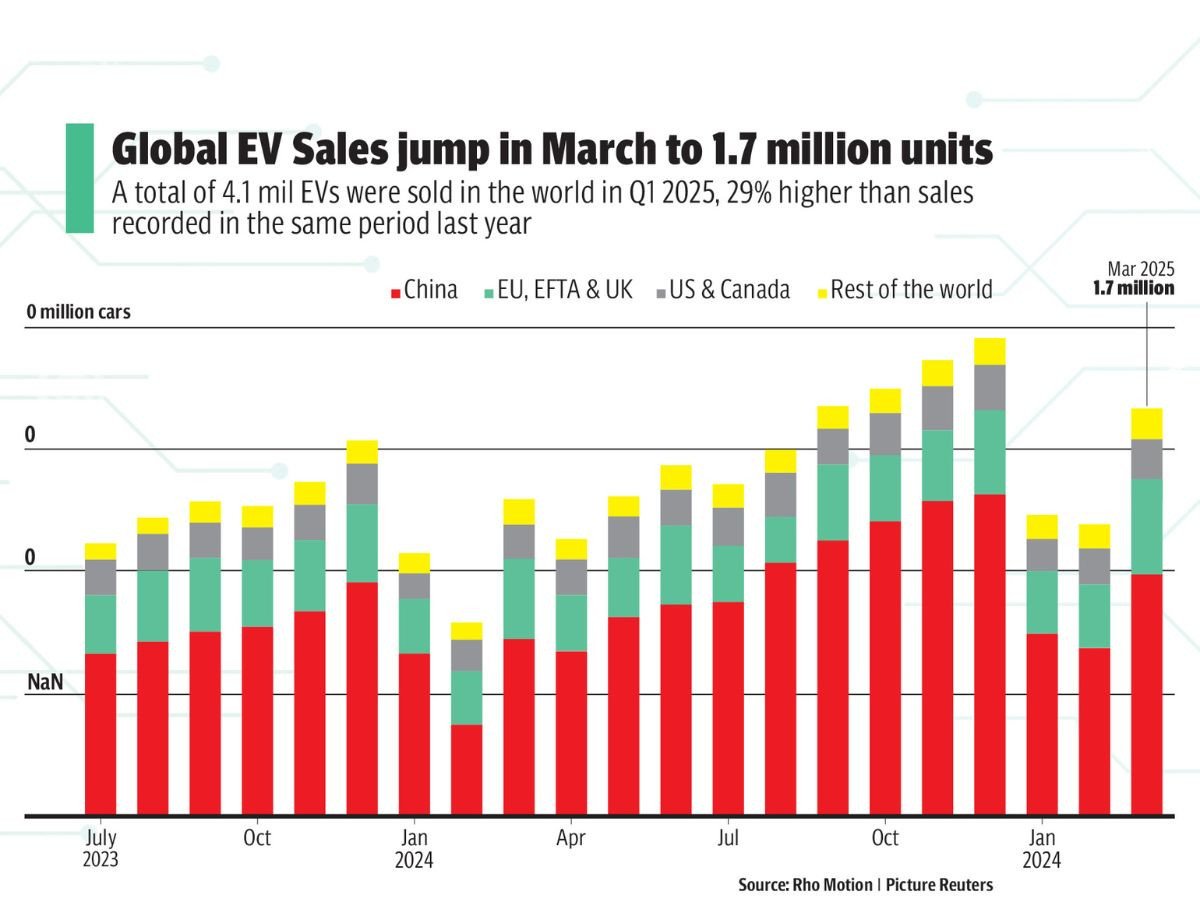

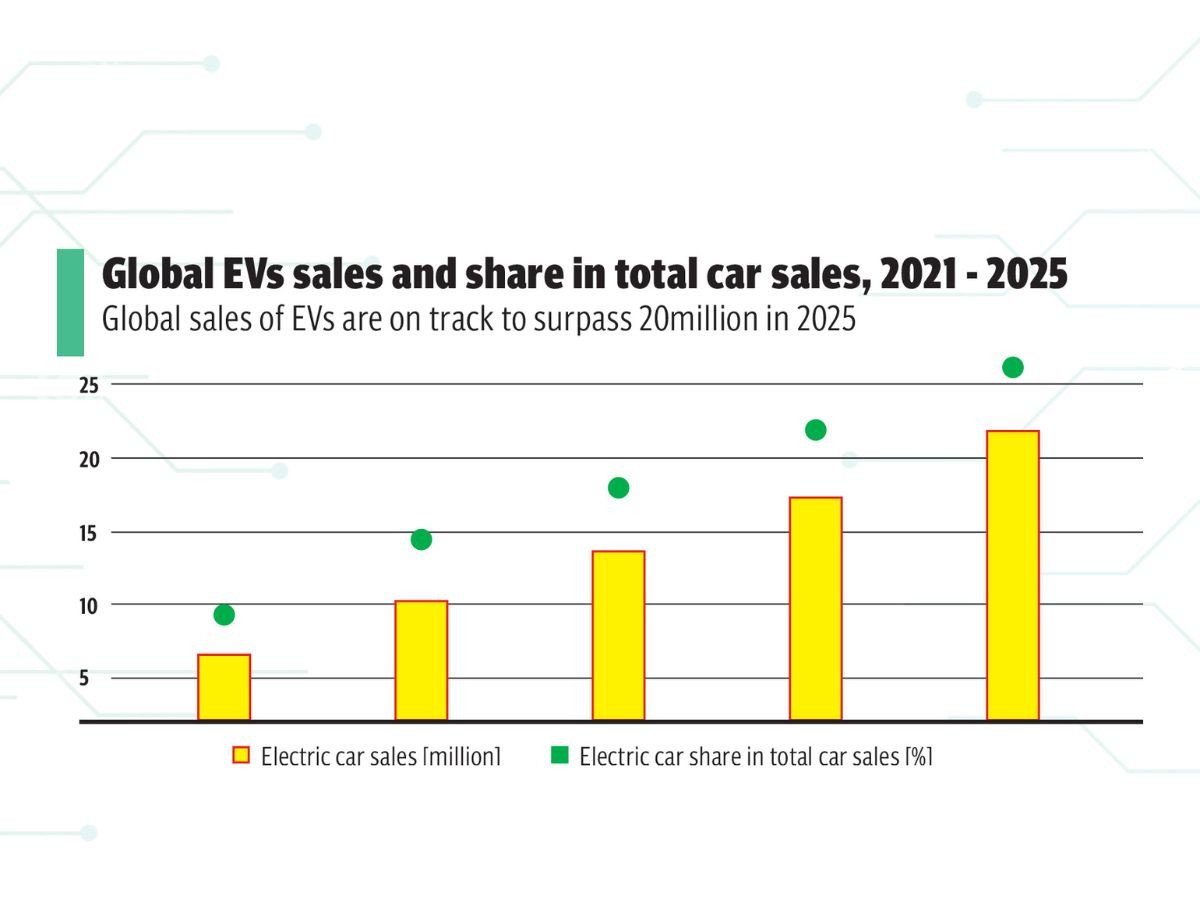

Around the world, the case for New Energy Vehicles has moved well beyond symbolism. In 2024, more than 17 million EVs and PHEVs were sold globally, a 25 percent increase from the year before, with forecasts suggesting sales will surpass 20 million in 2025. China alone now sells more EVs in a single month than most countries sell in a year. Europe, too, has embraced the transition; in the first half of 2025, over half of all new car registrations carried some form of electrification. In Norway, nearly four out of every five new cars are fully electric, an achievement that once seemed unthinkable but is now routine, powered by years of incentives and consistent infrastructure investment.

Governments have discovered that NEVs are more than just a consumer upgrade; they are a tool of national strategy. Transport is one of the largest contributors to carbon emissions, and urban pollution has become a political issue in many countries. By replacing internal combustion engines with electric or hybrid powertrains, nations cut dependence on imported oil, save billions in foreign exchange, and reduce the smog that chokes their cities. For countries that import much of their energy, the appeal is obvious: cleaner air at home and greater resilience abroad.

The rise of NEVs has also spurred new industrial ecosystems. Thailand, for example, has positioned itself as Southeast Asia’s EV hub by offering automakers tax breaks and duty reductions in exchange for commitments to local assembly. Indonesia has moved aggressively into the electric supply chain by promoting domestic nickel reserves for battery production. Even small markets have shown what is possible with the right approach.

These global examples show that the shift to new energy vehicles is no longer limited to rich nations. From Europe’s motorways to the crowded streets of Southeast Asia, electric mobility is spreading on the back of climate concerns and economic logic. Pakistan, by contrast, is only just beginning. Policies have been announced and a few showrooms have opened, but adoption remains slow, infrastructure is thin, and prices are still out of reach for most buyers. The success of NEVs elsewhere shows what is possible, but also underlines how far Pakistan has to travel.

On the ground, the gap between ambition and reality is hard to miss. Other countries move quickly with clear policies and expanding networks, while Pakistan is still sketching the outlines of a plan. The government has set targets, big players have entered with big promises, and early adopters are experimenting in cities such as Karachi and Lahore. But under the optimism linger real questions about charging, affordability and whether policy can keep pace with technology.

Pakistan’s NEV landscape

On paper, Pakistan has not ignored the rise of new energy vehicles. Targets have been set, committees formed, and policies announced with the promise of a greener transport future. The government has spoken of seeing thirty percent of all new vehicles as NEVs by 2030, and officials have laid out frameworks that appear designed to encourage investment. But on the roads of Karachi, Lahore, and Islamabad, progress is far less visible.

When asked about the policy environment, Danish Khaliq, the Vice President Sales and Strategy at Mega Motor Company (Private Limited), BYD’s local partner in Pakistan, acknowledged that conditions had improved compared to just a few years ago. “Two key policy frameworks exist. One is the Electric Vehicle Charging Policy, which streamlines NOCs and reduction in tariffs for charging stations. The other is the National Electric Vehicle Policy 2025-2030, which incentivizes NEV adoption. It gives subsidies on two- and three-wheelers (Up to Rs65,000 on 2 wheelers and up to PKR 400,000 on 3 wheelers.) and talks of extending this to four-wheelers in the future. Consistency and long-term implementation remain important,” he explained. In addition to this the NEV policy aims to achieve 3,000 public charging stations by 2030.

The optimism, however, is tempered by market realities. In September 2025, Pakistan’s Tariff Policy Board formally approved the commercial import of used vehicles up to five years old. According to the Federal Board of Revenue (FBR), these imports are subject to an additional 40% percent duty and the decision is still to be placed before the Economic Coordination Committee (ECC) for final authorization. While framed as a step toward broadening consumer choice, industry leaders see it very differently.

As Khaliq put it, “Practically, this favors Internal Combustion Engine (ICE) vehicles, not EVs. Importers will mostly bring in old petrol and diesel cars because they’re cheaper. That’s counterproductive, it worsens emissions, wastes limited foreign exchange, and we don’t even have mandatory emissions testing. Used EVs are rare, so the benefit is minimal for EV adoption.”

From the perspective of car reviewers and consumers, the gap between what is promised and what is delivered is even starker. Sunil Munj, co-founder of PakWheels, had a different perspective. “The truth is, despite the talk, our charging network is almost non-existent. Policies are ambitious, but the implementation is missing. Without consistent support, the market will struggle,” he said.

The contradiction is clear. On one side, policy documents speak of streamlined approvals, subsidies, and a network of charging stations that would transform the country’s mobility landscape by the end of the decade. At the same time, drivers can still count on one hand the number of working chargers in the country’s biggest cities, while dealers continue to bring in second-hand petrol cars by the shipload. For now, Pakistan’s journey with new energy vehicles sits in an uneasy middle ground, ambitious on paper, uncertain in practice, and waiting to see whether promises can turn into action.

For policymakers and automakers, the debate revolves around targets, tariffs and incentives. For ordinary drivers, the question is far simpler: will these cars make life easier, cheaper and more reliable? In cities where daily commutes stretch well past an hour and long intercity trips are routine, the real test will not be in policy documents or press conferences, but in how these vehicles fit into everyday habits and worries.

Consumer insights

For many buyers in Pakistan, the debate over new energy vehicles is not about policy frameworks or technical jargon. It is about whether these cars can realistically replace the habits formed over decades of driving petrol engines. That is why voices from within the car community carry weight, reflecting what ordinary commuters see as practical solutions.

Sunil, described PHEVs as the natural middle ground for a market like Pakistan. “I think this machine is an ideal shift from a petrol or gasoline engine towards an EV, because PHEV is right in the center. So, when you’re changing the habit of people that were used to driving gasoline cars, going 100 percent electric is a big step. PHEV gives you the long-range of petrol plus the ability to drive electric on city commutes. First step towards full electric.”

He pointed to commuting patterns as one of the strongest reasons why hybrids with electric range may fit better than pure EVs at this stage. “If I look at Karachi, a one-way, 40–50-minute drive is normal. In Lahore, inter-city drives to Faisalabad, Multan, Islamabad, even Peshawar are common. For a 100 percent EV, range anxiety is real with our weak charging network. PHEV solves that problem because you get electric range and the liberty to cover long distances on fuel.”

For Sunil, the hesitation surrounding charging is part of a natural adjustment process. He compared it to the early days of mobile phones, when users were unsure about charging habits. “Range anxiety is the biggest barrier. Just like mobile phones, when they first came, people worried about charging. Now it’s second nature. Once people get used to plugging in their car every night, PHEVs will become normal. They are the ideal step to ease consumers into new technology.”

For now, PHEVs offer a practical answer to the anxieties of daily commutes, giving drivers the reassurance of fuel with the efficiency of electricity. They point to a future where habits may gradually shift, but the direction of that shift will depend on how the industry responds. Automakers and dealers now face the challenge of matching consumer expectations with products, pricing, and infrastructure, and it is here that companies like BYD have begun to stake their claim.

Shaping the market

Pakistan’s shift toward cleaner mobility is still in its infancy, but the entry of global automakers has begun to shape how this market will look in the years ahead. Toyota, Honda, and Hyundai continue to push their conventional hybrids, while MG introduced one of the first mass-market EVs. More recently, BYD has entered with both PHEVs and EVs with launching Pakistan’s first NEV below PKR 9 million, signaling that the transition will not be limited to luxury niches.

For BYD, the decision to arrive now is tied directly to the pressures facing Pakistan. Danish Khaliq explained, “Pakistan is at a critical point. We are facing climate calamities, yet transportation is still one of the biggest consumers of imported fuel, which strains foreign exchange and harms the environment. That is why we felt the timing was right to introduce sustainable mobility. It is similar to how Pakistan skipped landline saturation and directly moved to mobile phones. We do not need to wait decades before shifting to EVs. The technology is affordable and accessible now, and we can benefit immediately.”

The question is how quickly these benefits can be realized. Khaliq noted that both EVs and PHEVs have measurable environmental gains. “The impact depends on adoption. EVs eliminate tailpipe emissions, and even with mixed-fuel electricity, emissions drop by around 80 percent. PHEVs can reduce them by 60 to 70 percent.

For adoption, three issues need tackling: product availability, charging infrastructure, and price parity. We are addressing these by rolling out charging stations through HUBCO Green, our sister concern, who has partnered with leading Oil Marketing Companies (OMCs)like PSO and Attock Petroleum PARCO Gunvor, and also by installing chargers in malls, offices, and towers. The government is supporting with new charging policies, which helps confidence in adoption.”

That confidence is tested by how the technologies are sequenced. Should Pakistan rely on conventional hybrids as a halfway step, or push more directly toward PHEVs and EVs? “Hybrid electric vehicles have small batteries and limited environmental benefit. PHEVs and EVs are what Pakistan needs, because they give real emission reductions and efficiency. Both can work together. EVs give the additional benefit of maximum tailpipe emission reductions while PHEVs address range anxiety until charging infrastructure expands,” Khaliq said.

He also reiterated the future readiness of the company’s technology. “BYD began as a battery company, which gives us an edge. Our Blade Battery is one of the safest in the world. It passes the nail penetration ‘Everest’ test where others explode. Beyond that, BYD invests heavily in R&D with 100,000 engineers working on EV platforms, making batteries denser, safer, and more efficient every year.”

The pitch to consumers is framed not only around technology but also everyday savings. “Buying a car is buying an asset, and Pakistani consumers are very informed. Our Ato 3 is already cheaper than many local hybrids. Driving 400 km on an EV costs around Rs. 2,500 to PKR 3,000 in electricity costs, compared to Rs. 10,000–12,000 in petrol. That is a three to four times savings on running costs.

Maintenance is also reduced to a half or one-third the cost of ICE vehicles since there is no requirement for engine oil and filters (oil).. We have set up after-sales centers across the largest cities in Pakistan, are continuously training local staff, and are building a state-of-the-art local assembly plant. Adopting EVs and PHEVs is not just about being futuristic. It is practical, economical, and necessary for Pakistan’s environment and energy security,” Khaliq said.

For industry observers, the arrival of new models such as the Shark 6 pickup truck could broaden the market further. Sunil Manch described it as a potential disruptor in a segment long dominated by a single option. “In Pakistan, the pickup market had almost no options besides the Vigo. The Shark offers power, fuel economy, and cabin comfort, especially rear seat comfort, which has always been poor in pickups here. This makes it ideal for Pakistani families. But the real buyer will depend on the price. If the price is right, it will disrupt the market.”

He also pointed out how safety and reassurance could expand the appeal beyond traditional buyers. “Range anxiety often discourages women drivers. With the Shark 6, the combined fuel and charge range removes that risk. Its safety features and driving comfort make it reassuring for both men and women.”

Taken together, these perspectives show how the industry is starting to respond to both opportunity and skepticism. Big names still rule Pakistan’s roads, but newer players are starting to test old assumptions about cost, performance and safety. The real measure, though, will come once these cars leave the polished floors of showrooms and settle into the routines of daily life. It is in the experiences of actual users that the promises of technology will be weighed against the realities of the road.

Life behind the wheel

Policy debates and corporate strategies tell one side of the story. The other unfolds quietly on city streets, in homes where drivers are learning what it actually means to own and maintain a PHEV or EV in Pakistan.

Ali Raza, 38, from Lahore, said his decision came after months of watching petrol prices eat into his income. Filling the tank of his old car felt like handing over half his salary each time. The numbers pushed him toward a EV, a choice he felt was both lighter on the wallet and more in step with where the world is heading.

For Raza, the vehicle is not a luxury toy but a family workhorse. “This is not my secondary car. It is the one I use every day, whether it is for dropping my kids to school, going to the office, but visiting relatives in another city, that’s still my fear. Initially people thought I would keep it as a backup, but it has now replaced my main car.”

The shift has already shown up in his household budget. “On fuel alone I save close to 30,000 rupees a month. Maintenance is another relief because there is no engine oil or filters to worry about. If I compare it with my old petrol car, the running cost is almost one-third. For the first time in years, I feel like a car is not draining my wallet.”

Yet the transition has not erased all worries. Raza admitted that resale value and after-sales service still weigh on his mind. “My biggest concern is what happens after three or four years. Will people be willing to buy it second-hand. Will parts and service be as easily available as they are for Toyota or Honda. Charging is less of an issue for me because I installed one at home, but I still wonder what will happen on a long trip outside Lahore.”

Khaliq informed that to meet long-term adoption targets, they have chosen to challenge the perception that electric means expensive. “Earlier entrants introduced luxury EVs, creating a perception that electric means expensive. We challenged that with the Ato3 at Rs. 9 million, which is even competitively priced than some of the locally assembled hybrids. We also invested in charging infrastructure ourselves and set up our own experience centers and after-sales service to give customers confidence. Our strategy is simple: competitive pricing, infrastructure development, strong after-sales, and continuous consumer education,” Khaliq explained.

The question of local capacity inevitably follows. Batteries account for a large share of an EV’s value, and whether Pakistan can one day produce them domestically remains uncertain. “Batteries make up 35 to 40 percent of an EV’s value. Initially, we will import them, as Pakistan does not yet have the scale or technology to manufacture. Once local assembly grows and applications like energy storage expand, battery assembly and later manufacturing could follow. But the first step is setting up EV assembly plants, which we are already working on,” Khaliq said.

The experiences of early adopters point to the questions that remain unanswered. What happens when thousands more make the switch. Can the infrastructure keep pace. And will the market evolve fast enough to support them.

Roadblocks on the journey

Every new technology carries its own hurdles, and Pakistan’s early encounter with NEVs is no different. For all the optimism about cleaner transport, the realities of infrastructure, affordability, and market confidence continue to weigh heavily.

For industry observers like Sunil, the most immediate concern remains charging. “Our charging network is really in bad shape right now. Even today, you can count the number of commercial chargers in Lahore, Islamabad, and Karachi. It is such a shame. But if I see the glass half full, for the first time we have surplus electricity in the country. We just need the charging units, and BYD says they will help set those up.” His words echo what many potential buyers fear most: the anxiety of not finding a reliable charging point when it is needed most.

Affordability is another obstacle. Khaliq pointed out that while wealthy early adopters may not depend on government support, broader uptake cannot happen without it. “Early adopters do not necessarily rely on subsidies, but for mass adoption, price support will be needed. Globally, there are demand-side incentives like rebates and subsidies and supply-side ones such as local assembly support through tax and duties relaxation. In Pakistan, supply-side incentives are more sustainable because they encourage local assembly and industry growth, rather than draining subsidy pools quickly.”

The frustrations are not limited to policy or infrastructure. The excitement of owning something new has not erased the day-to-day frustrations. Raza remembered how friends and family congratulated him on the savings, only for him to discover the limits of the system the first time he looked for a fast charger on the motorway. The network, he said, is patchy at best, and moments like that remind him how early Pakistan still is in this journey.

These obstacles show that adoption is not simply about technology arriving in showrooms. It is about the conditions around it, from policy execution to consumer trust

Tesco and Sainsbury’s customers are paying more than Waitrose shoppers for some common branded groceries if they are not using a loyalty scheme, analysis by Which? has found.

The watchdog compared a list of 245 branded items including Heinz, Nescafe and Mr Kipling in February, finding that it was, on average, most expensive for customers at Sainsbury’s and Tesco who were not using the Nectar or Clubcard loyalty schemes.

Which? acknowledged that most shoppers are part of a membership scheme, but said some may be unwilling to sign up to loyalty cards for reasons such as data privacy, while others have no choice because of eligibility criteria.

Tesco customers who are under 18 can not sign up to a Clubcard, although the supermarket has announced it will review this before the end of the year.

The Which? list of items was most expensive at Sainsbury’s for non-Nectar members at £942.66 – 14% more than the cheapest retailer in the study Asda, which cost £823.58.

Tesco followed behind Sainsbury’s, with its non-Clubcard price totalling 11% more than Asda at £916.56.

Which? said it did not include discounters Aldi and Lidl in the study because they did not stock a sufficiently large range of branded goods.

Both Tesco and Sainsbury’s – the UK’s two largest grocers – were more expensive for non-members of their loyalty schemes than Waitrose, which cost £899.05.

Waitrose was 9% more expensive than Asda and emerged as a “more competitive option”, Which? said.

Which? found several products that were cheaper at Waitrose, including Amoy Straight To Wok Noodles, which were on average £1.25 at both Waitrose and Morrisons but most expensive at Sainsbury’s and Tesco without a loyalty card at an average of £2.15 – a 72% difference.

Sea salt and vinegar Ryvita Thins were also cheapest on average at Waitrose at £1.25, but shoppers buying this product at Morrisons, Tesco, and Sainsbury’s without a loyalty card would all have paid an average of £2.30, making them 84% more expensive.

For customers with a Clubcard, Which? found that the same list of groceries at Tesco fell to £837.43 on average – just 2% more expensive than Asda.

Which? found various instances of branded products where the Tesco Clubcard price was the cheapest on average.

Carex Hand Wash was 95p at Tesco with a Clubcard but £1.70 at Waitrose where it was the most expensive.

Another example showed Kellogg’s Crunchy Nut cornflakes was £1.55 on average in February, while the highest average price among the supermarkets was at Waitrose where it cost £2.50.

Which? said the figures showed the “dramatic price gulf” created by loyalty pricing.

In one example at Tesco, Which? found a 200ml bottle of L’Oreal Paris Elvive Bond Repair Shampoo was double the price on average for shoppers without a Clubcard – at £13 compared to £6.50.

The higher price was also found at both Morrisons and Sainsbury’s.

Which? found that a 200g jar of Kenco Smooth coffee cost shoppers at Tesco and Sainsbury’s without a loyalty card £8.35 – the highest price on the market.

In contrast, the same jar was £7 at Waitrose and £6.32 at Asda, on average.

Similarly, Waitrose had the cheapest average price for Nescafe Gold Blend at £6.25, while non-members at Sainsbury’s were asked to pay £8.35.

Meanwhile, Which? found customers who used a Nectar card at Sainsbury’s could expect to pay only 3% more than Asda at £848.56 for the entire list of items.

Morrisons averaged 4% more expensive than Asda when using a More card and 5% more expensive without one.

Ocado was also 5% more expensive than Asda.

Which? retail editor Reena Sewraz said: “Our analysis reveals a shocking truth and shows the impact loyalty schemes have had on grocery pricing.

“Branded favourites can actually be cheaper at Waitrose than at the UK’s biggest supermarkets for shoppers who don’t use a loyalty card – something that would have seemed unthinkable until a few years ago.

“If you’ve got your heart set on specific brands, your best bet is to shop around, keep a close eye on the unit price, and stock up whenever you see a good deal – otherwise, you’re likely to end up paying way over the odds.

“While loyalty cards definitely offer some savings, if you don’t use one you’re better off heading to Asda, where the pricing is usually cheaper on a range of branded goods.”

A Sainsbury’s spokesman said: “We have invested over £1 billion in recent years to help keep prices low and we know more customers are choosing to do their shop at Sainsbury’s.

“We are committed to helping customers access great quality at lower prices and remain focused on offering outstanding value across thousands of products through our Aldi price match scheme, Nectar prices, Your Nectar Prices and our own-brand value lines.”

A spokesman for Tesco said: “It’s no secret that Tesco Clubcard unlocks exceptional savings for the 24 million UK households who have one.

“More than 80% of our sales are made with a Clubcard – but it’s just one of the ways our customers get great value.

“Though everyday low prices we keep prices consistently low on thousands of branded products, and our Aldi price match ensures shoppers can be confident they’re getting competitive prices.”

Business

MLB faces a historic shift as potential lockout, media rights and other league changes loom

Thursday’s Opening Day may be the calm before the storm for Major League Baseball.

The league’s collective bargaining agreement with its players expires at the end of this season. Owners, with the commissioner’s backing, are almost sure to push for a salary cap (which would likely come with a salary floor to get players to the negotiating table).

MLB owners have never been able to get a cap passed by the players union. It’s unclear if the end of the 2026 season will lead to a different result, but MLB Players Association Interim Executive Director Bruce Meyer told ESPN last month he expects a lockout is “all but guaranteed.”

In addition to the CBA’s expiration, there are major shifts underway for baseball media rights. One-third of the league’s teams didn’t have local TV deals in place for this season until this week.

Nine MLB teams – the Washington Nationals, Seattle Mariners, Milwaukee Brewers, St. Louis Cardinals, Miami Marlins, Tampa Bay Rays, Cincinnati Reds, Kansas City Royals, and Detroit Tigers – announced Wednesday their brand new MLB-operated team channels will be carried by DirecTV.

Most of those teams had previously been part of Main Street Sports (previously Diamond Sports Group), which operates FanDuel Sports Networks (previously Bally Sports). That entity has been teetering with liquidation, and the teams terminated their contracts with the company due to missed payments earlier this year.

A 10th team, the Atlanta Braves, is launching a new network called BravesVision. The Braves and Charter’s Spectrum announced a multiyear distribution agreement earlier this week.

MLB ideally wants the rights to all 30 teams in its control by the end of the 2028 season so that it can sell the in-market local games as a national package to a streamer. That would become the modern replacement to regional sports networks, and it would likely be a new, coveted package for streaming services such as ESPN and Amazon Prime Video.

Also at the end of the 2028 season, MLB’s national media rights for all of its packages will expire, allowing the league to redistribute games to its partners and potentially select new ones.

NBC, ESPN, Fox and a combined CBS/Turner have dominated national rights for the past few decades.

“The key in media negotiations now is having all of your rights available,” MLB Commissioner Rob Manfred told me last year. “If you have all of your content – all of your playoffs, all of your regular season – available, there will be buyers, and I’m confident there will be buyers at a higher price for us.”

Manfred has even floated the idea of expanding to 32 teams and realigning the league geographically, upending or even eliminating the American and National leagues that have existed for more than 100 years.

Soaring TV ratings

It’s, of course, unclear how much of this hypothetical change will actually come to fruition.

But the potential for transformation at MLB is greater than at any of the other Big 4 professional leagues in the U.S.

And yet, baseball isn’t struggling — on the contrary. The implementation of the pitch clock in 2023 has led to shorter games, rising attendance and higher TV ratings.

Rob Manfred, Commissioner of the MLB, attends the annual Allen and Co. Sun Valley Media and Technology Conference at the Sun Valley Resort in Sun Valley, Idaho, U.S., on July 9, 2025.

David A. Grogan | CNBC

More than 50 million people in the U.S., Canada and Japan watched Game Seven of the World Series last year – the most-watched baseball game in 34 years. MLB recently wrapped up the World Baseball Classic – a global preseason tournament – which captured nearly 11 million viewers on Fox and Fox Deportes for its final game.

MLB team valuations rose 13% from last year. The average MLB team is now worth $2.95 billion, according to CNBC Sport data.

Still, the profitability of the league is in far worse shape than it is for the NFL, NBA and NHL, according to CNBC’s calculations. In 2025, MLB’s 30 teams had an EBITDA — earnings before interest, taxes, depreciation and amortization — margin of under 2%. Team average revenue was $426 million with average EBITDA of $7 million, including non-MLB ballpark events. In contrast, the comparable margin for the NFL was 20%; the NBA, 21% and the NHL, 22%, according to CNBC’s most recent valuations.

The new CBA at the end of this season could be the first significant step toward a very different MLB. But, similar to the WNBA, which announced its new CBA earlier this week, MLB must ensure negotiations to get a new labor agreement don’t jeopardize a wave of positive momentum.

A JLR spokesperson said: “Due to a part supply challenge with a supplier, we are temporarily pausing production on certain vehicle lines at our Solihull manufacturing facility. We are working closely with that supplier to resolve the issue as quickly as possible and minimise any impact on our clients or our operations.”

China concludes Mexico tariffs create trade barriers for firms

Taylor Swift wins seven awards at iHeartRadio Music Awards 2026

How Cole Hutson is taking a role in the next wave for the Capitals

-

Fashion1 week ago

Fashion1 week agoSales at US apparel, clothing accessories stores up 4% YoY in Jan 2026

-

Fashion1 week ago

Fashion1 week agoSpain’s Inditex FY25 sales rise 3.2% to $46.28 bn amid strong demand

-

Entertainment1 week ago

Entertainment1 week agoVal Kilmer revived 1 year after death through AI

-

Politics1 week ago

Politics1 week agoIran strikes Tel Aviv with cluster-warhead missiles in retaliation of Larijani’s martyrdom

-

Sports1 week ago

Sports1 week agoMarch Madness 2026 – How to watch in SA, start time, schedule, TV channel for NCAA championship basketball tournament

-

Fashion1 week ago

Fashion1 week agoUS’ G-III Apparel’s FY26 sales fall 7% to $2.96 bn

-

Politics1 week ago

Politics1 week agoUS judge directs Trump administration to bring VOA employees back

-

Business1 week ago

Business1 week agoBrits cashing in jewellery as gold price hits record high