Fashion

$6 bn of India’s T&A exports to the EU concentrated in 20 HS codes

Analysis at the product level

Over $6 billion of India’s textile and apparel exports to the EU are concentrated in just 20 four-digit HS codes, out of a total export base of ~$7.5 billion, making the India–EU FTA a sharply product-specific opportunity rather than a broad-based boost.

Finished apparel emerges as the primary beneficiary, as tariff parity improves India’s competitiveness against other Asian suppliers.

India and the European Union have signed the long-awaited Free Trade Agreement (FTA), with the pact expected to come into force in early 2027 (or earlier) following ratification. While trade flows will remain largely unchanged in the near term, product-wise export data indicates that the agreement could reshape India’s textile and apparel exports to the EU over the medium term, with gains concentrated in finished apparel rather than intermediate products.

India’s EU-facing textile and apparel exports are highly concentrated. The top 20 four-digit HS codes account for more than $6 billion, out of total textile and apparel exports of roughly $7.5 billion to the EU, underscoring where the FTA’s eventual impact is likely to be most visible.

Apparel dominates India’s EU export basket

Finished apparel forms the backbone of India’s textile and apparel exports to the EU, led by women’s wear, knitted garments, and core woven apparel. Home textiles represent the second pillar, while yarns, fabrics, and fibre-based products contribute a smaller share in value terms.

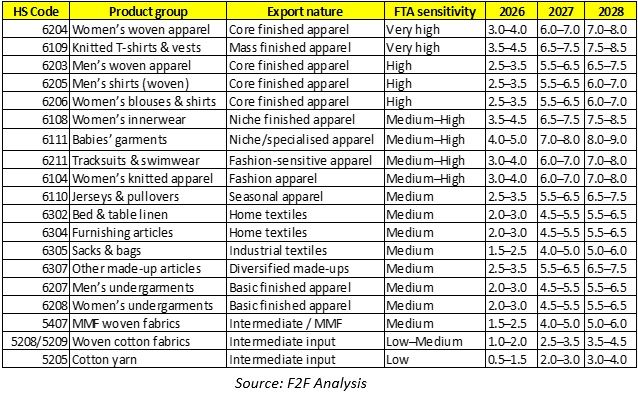

Table 1: India’s total Textile and Apparel exports to the EU-27 – Top 20 four-digit HS codes (2025)

Export growth in 2026 is expected to remain moderate as buyers focus on audits, compliance checks, and limited pilot orders ahead of implementation. A clearer divergence is expected from 2027, once tariff concessions take effect, with finished apparel emerging as the most responsive category.

Table 2: India–EU textile exports – Product-wise growth outlook (YoY growth %, indicative)

What to watch till 2027

Product readiness is expected to improve fastest in high-volume apparel categories, while home textiles see incremental upgrades rather than greenfield expansion. Compliance alignment, particularly on sustainability and traceability will be a key differentiator, with cotton-based segments better positioned than MMF apparel. Buyer engagement is likely to intensify through audits and pilot orders ahead of implementation, while competing suppliers such as Bangladesh and Vietnam are expected to defend share through pricing and buyer integration rather than capacity expansion. Final tariff schedules and rules of origin will determine which products benefit first.

The India–EU FTA signals a medium-term reset, not an immediate surge. With over $6 billion concentrated in the top 20 product groups, finished apparel is best positioned to lead post-2027 gains, while home textiles compound steadily and intermediates remain less responsive.

Fibre2Fashion News Desk (AA)