Business

Food price rises slow as UK inflation remains at 3.8%

Charlotte EdwardsBusiness reporter, BBC News

Getty Images

Getty ImagesFood and drinks prices in the UK are increasing at their slowest rate in more than a year, while overall inflation remains unchanged for the third month in a row.

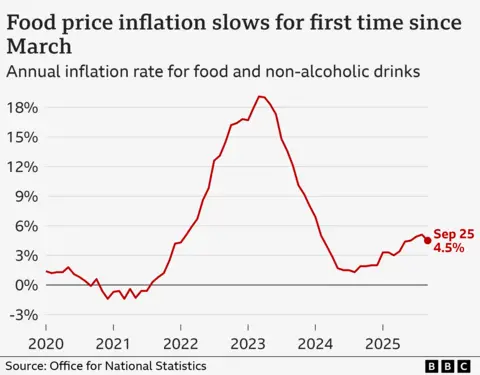

Month-on-month, the cost of food and non-alcoholic drinks actually edged down slightly in September – the first fall since May 2024. The ONS said his was likely to have been driven by increased sales and discounting by retailers.

The UK inflation rate for all items remained stable at a lower-than-expected 3.8% in the year to September, official figures show.

Chancellor Rachel Reeves said she was “not satisfied with the numbers” on inflation, while shadow chancellor Mel Stride said it was “pushing up the cost of living”.

Elaine Doran/BBC

Elaine Doran/BBCThe inflation rate for food and non-alcoholic drinks was down to 4.5% for the year to September from 5.1% in the year to August.

This means the price shoppers pay for groceries and non-alcoholic drinks is still going up, just more slowly than before.

But between August and September this year, the cost of food and non-alcoholic drinks overall actually fell by 0.2% – the first fall for 16 months.

The drop was driven by slightly cheaper vegetables, milk, cheese and eggs, bread and cereals, fish, mineral waters, soft drinks and juices.

However, the cost of specific items such as red meat and chocolate continued to rise.

Kayleigh Brannan, a mother to baby Hadley, told the BBC she had noticed the price of meat rising in particular, and that now Hadley has started eating solid foods, she expected her expenses would be going up.

“It’s not too bad at the moment but you can see the prices going up,” she said.

She added: “The maternity pay is not enough. You’ve still got the same bills, you’ve still got to pay the mortgage… obviously you have more pressure then.”

Britain’s inflation rate was also 3.8% in July and August, according to the ONS, which is still much higher than the Bank of England’s 2% target.

However, the central bank’s economists had forecast inflation to rise to 4% in September.

ONS chief economist Grant Fitzner said: “The largest upward drivers came from petrol prices and airfares, where the fall in prices eased in comparison to last year.”

He added: “These were offset by lower prices for a range of recreational and cultural purchases including live events.”

Mr Fitzner told BBC Radio 4’s Today programme that food prices were still “running quite high at 4.5%” but added “the fact that we have seen that steady increase dip a little is encouraging.”

“It is just one month’s numbers so we will have to see what transpires in future months – but nonetheless a small glimmer of hope there,” he said.

Paul Dales, chief UK economist for Capital Economics, said while food price inflation could rise further, “this will probably be the peak in inflation”.

James Walton, chief economist at the Institute of Grocery Distribution said the declining rate of food and drink inflation “aligns with our predictions that food inflation will start to moderate, and we may have seen the peak.”

“Whilst this is good news, prices for shoppers are still going up year on year, just more slowly,” he said.

Mr Walton noted that items such as red meat, coffee and chocolate are still seeing strong price increases and linked this to issues with production, such as bad weather.

Danni Hewson, AJ Bell head of financial analysis, said: “Staples like vegetables, milk, cheese and bread were all pared back a touch, though such tiny movements won’t make a huge difference to the overall bill when people reach supermarket tills.”

Dr Kris Hamer, director of insight at the British Retail Consortium, said the figures were “unlikely to raise consumer spirits as the cost of a weekly grocery shop was still “significantly higher than last year”.

“Nonetheless, consumers will have been happy to see the price of key staples such as rice, bread and cereal fall on the month,” he said.

The chancellor said she was “not satisfied with these numbers.”

“For too long, our economy has felt stuck, with people feeling like they are putting in more and getting less out,” Reeves said.

She added that she was determined to ensure the government supports people “struggling with higher bills and the cost of living challenges, deliver economic growth and build an economy that works for, and rewards, working people.”

In a post on X, the shadow chancellor said that inflation running at nearly double the Bank of England’s target was “pushing up the cost of living and punishing those Labour promised to protect”.

Stride claimed national insurance increases, government borrowing and not having “the backbone to reduce spending” were all contributing to inflation.

The overall inflation figure for September matters more than most other months.

That’s because the government usually uses this as the benchmark for the benefits uprating in April.

It means millions of people depending on benefits are likely to see a 3.8% increase in their payments next year.

The state pension will rise by more, because the annual increase for that is determined by the so-called triple lock.

This guarantees that the state pension goes up each year in line with either inflation, wage increases or 2.5% – whichever is the highest. September’s inflation figure of 3.8% is below average earnings for the relevant period (4.8%) which means the rise in wages will decide the state pension increase.

The inflation figures for the past three months were the joint-highest recorded since January 2024, when the rate was 4%, according to the ONS.

Inflation in the UK remains well below the 11.1% figure reached in October 2022, which was the highest rate for 40 years.

Musk’s loss against OpenAI is the latest in a string of courtroom defeats.

Source link

The FTSE 100 closed higher on Monday, recouping most of Friday’s hefty falls amid a calmer bond market and as Iran responded to the latest US peace proposal.

The FTSE 100 closed up 128.38 points, 1.3%, at 10,323.75. The FTSE 250 ended up 15.56 points, 0.1%, at 22,611.70, but the AIM All-Share fell 8.72 points, 1.1%, at 800.17.

Iran said it had responded to a new US proposal aimed at ending the war, adding that diplomatic exchanges continue despite Iranian media reports describing Washington’s demands as excessive, AFP reported.

Washington and Tehran have been swapping proposals in an effort to end the conflict, which the US and Israel launched on February 28, but they have held only a single round of talks despite a fragile ceasefire.

“As we announced yesterday, our concerns were conveyed to the American side,” foreign ministry spokesman Esmaeil Baqaei told a news briefing, adding that exchanges were “continuing through the Pakistani mediator”.

Mr Baqaei defended Iran’s demands, including the release of Iranian assets frozen abroad and the lifting of long-standing sanctions.

“The points raised are Iranian demands that have been firmly defended by the Iranian negotiating team in every round of negotiations,” he said.

But with no signs of clear progress, the oil price remained inflated and volatile.

Brent crude for July delivery was trading at 110.80 dollars a barrel on Monday, up compared to 108.83 at the time of the equities close in London on Friday.

After a frantic Friday, the bond markets calmed, while sterling also rebounded as investors weighed the latest political developments.

The yield on UK 10-year gilts traded at 5.14% compared to 5.17% at the same time on Friday.

The pound traded at 1.3397 dollars on Monday afternoon, up from 1.3319 on Friday. Against the euro, sterling firmed to 1.1506 euros from 1.1462 on Friday.

Prime Minister Sir Keir Starmer insisted he would not set out a timetable to leave No 10 as potential leadership challenger Andy Burnham vowed to “change Labour” if he is successful in his effort to return to Parliament.

The Prime Minister said he still wants to lead Labour into the next general election amid calls from within the party to set out a timetable for his exit.

Greater Manchester Mayor Mr Burnham hopes to be Labour’s candidate in the Makerfield by-election, which could provide him with a route back to the Commons to challenge for the party leadership and the keys to Downing Street.

Speaking to broadcasters in London, Sir Keir said he was not going to set out a timetable to stand down if Mr Burnham returns to Westminster.

He added: “I do want to fight the next election. Obviously, I recognise that after the local election results, the elections in Wales and Scotland as well, that the first task is obviously turning things around and making sure that my focus is in the right place.”

Meanwhile, the International Monetary Fund said growth in the UK economy will be stronger this year than previously thought.

The IMF updated its growth projections a month after warning of a sharp slowdown caused by the global energy shock from the US-Iran war.

The influential financial body said it was now predicting UK gross domestic product to rise by 1% in 2026, higher than the 0.8% growth it was forecasting last month.

Responding to the latest report, Chancellor Rachel Reeves said: “The IMF upgrading its growth forecasts and backing our fiscal strategy is yet more proof that this Government has the right economic plan.”

In Europe, equity markets on Monday, the Cac 40 in Paris ended up 0.4%, and the Dax 40 in Frankfurt advanced 1.5%.

In New York, the Dow Jones Industrial Average was down 0.1%, the S&P 500 fell 0.4%, and the Nasdaq Composite was 0.7% lower.

On the FTSE 100, Whitbread closed up 2.3% after Corvex Management urged the Premier Inn owner to put itself up for sale, slamming its recently announced new five-year strategic plan.

In a damning letter to Whitbread management, the New York-based activist hedge fund called the status quo “untenable” and said that the need to pursue “meaningful strategic and structural reform had become unignorable”.

As a result, Corvex, which holds a stake of around 7% in Whitbread, said the only “credible” path to unlocking value at Whitbread is a sale of the company.

Anglo America fell 1.4% as it struck a deal to sell its portfolio of steelmaking coal mines in Australia to Dhilmar for up to 3.88 billion dollars in cash.

The London-based mining house said Dhilmar will pay the FTSE 100-listing 2.3 billion dollars upfront, and the deal has a price-linked earnout of up to 1.58 billion dollars.

Anglo American chief executive officer Duncan Wanblad said: “This agreement represents another major step in the simplification of our portfolio ahead of completing our merger with Teck. Through this transaction, we will complete our exit from steelmaking coal.”

Susannah Streeter, chief investment strategist at Wealth Club, said: “This not only strengthens the balance sheet, ahead of its planned merger with Canada’s Teck Resources, but also keeps it exposed to future strength in coal prices.”

Capita shares rose 8.9% as the London-based outsourcing and business services company said adjusted revenue rose 2.9% on-year in the first four months of 2026, which it said was in line with expectations.

Looking ahead, Capita said it continues to expect a low to mid-single digit revenue climb in Capita Public Service and expects mid-teen revenue growth in its Pension Solutions business.

The biggest risers on the FTSE 100 were Centrica, up 7.70p at 196.95p, National Grid, up 43.50p at 1,231.50p, Pearson, up 37.00p at 1,136.50p, Relx, up 81.00p at 2,504.00p, and SSE, up 74.00p at 2,345.00p.

The biggest fallers on the FTSE 100 were 3i Group, down 128.00p at 2,082.00p, Airtel Africa, down 15.60p at 312.80p, Mondi, down 16.40p at 734.60p, Polar Capital Technology Trust, down 12.50p at 659.00p and Diploma, down 95.00p at 6,625.00p.

Tuesday’s global economic calendar has UK consumer and wholesale inflation figures, eurozone inflation data and the minutes of the last Federal Open Market Committee meeting.

Tuesday’s local corporate calendar has full-year results from business services group DCC, half-year numbers from supplier of specialised technical products and services, Doploma, and electricals retailer Currys.

Lloyds Banking Group is considering phasing out its Halifax brand, a move that could bring an end to the 173-year-old institution.

The Sun reports that bosses are expected to announce the end of Halifax as a standalone brand this summer.

It is understood that no definitive decisions have yet been made about the brand, which granted its first mortgage in 1853.

Should Halifax be phased out, account numbers would remain unchanged, and customers’ automatic protection under the Financial Services Compensation Scheme (FSCS) would be unaffected.

“We regularly look at the role our brands play in supporting our customers,” a spokesperson for Lloyds said.

“Our banking customers can already use any Lloyds, Halifax or Bank of Scotland branch, and see any of their products and services in any of their apps – there are no changes for our customers today.”

The Sun, citing industry insiders, reported that any transition would begin on 1 July when people will no longer be able to open new Halifax accounts online or through the app.

By October, Halifax will stop taking on new customers entirely and existing account holders will be gradually migrated to Lloyds Bank, the reports say.

Lloyds declined to comment on the potential timings for any plans.

Britain’s biggest mortgage lender made changes in 2025 that meant its three brands, Lloyds, Halifax and Bank of Scotland, could share branches and mobile banking services.

The shake-up meant some customers could access a branch that is closer to their home because they will be able to access face-to-face banking regardless of the brand.

However, the banking giant has also shut hundreds of high street branches over recent years.

It started another round of closures this month, which will see 95 branches shuttered across the three brands by March 2027.

The closures will leave the group with 610 branches in total, of which 306 are Lloyds, 238 Halifax and 66 Bank of Scotland.

Lloyds has said that all employees currently working at the affected branches will be offered alternative roles within the business or at other locations.

Halifax and Lloyds operate in the same market in England and Wales, while Bank of Scotland is the group’s only brand in the country.

Elon Musk just lost another lawsuit. Will he keep fighting?

India will become history if it attempts any future misadventure, warns defence czar

Thomas Massie faces Trump-backed challenger in GOP primary: Can he win?

-

Entertainment6 days ago

Entertainment6 days agoConan O’Brien hat tricks as Oscar host

-

Tech1 week ago

Tech1 week agoCould Contact-Tracing Apps Help With the Hantavirus? Not Really

-

Fashion5 days ago

Fashion5 days agoItaly’s Zegna Group’s Q1 growth boosted by strong organic performance

-

Entertainment1 week ago

Entertainment1 week agoMartin Short: Facing tragedy with joy

-

Entertainment1 week ago

Entertainment1 week agoTom Brady gets back at Kevin Hart during Netflix roast

-

Sports1 week ago

Sports1 week agoJacob Fatu unleashes vicious assault on Roman Reigns after World Heavyweight Championship loss at WWE Backlash

-

Entertainment1 week ago

Entertainment1 week agoMartha Stewart: How to make an omelet

-

Tech1 week ago

Tech1 week agoPapa Johns Is Getting Into Drone Delivery—but Not for Pizza