Business

Social security benefits to rise 2.8%: Retirees to see $56 monthly boost; senior citizens say increase not enough – The Times of India

The Social Security administration on Friday announced that its benefits will increase by 2.8% in 2026, giving retirees an average monthly boost of more than $56. The rise reflects moderating inflation after several years of higher cost-of-living adjustments (COLA).The increase will take effect in January for nearly 71 million Social Security recipients, while about 7.5 million people receiving Supplemental Security Income will see higher payments starting December 31.The announcement, which was scheduled for last week, was delayed due to the US federal government shutdown.Recipients saw a 2.5% increase in 2025 and a 3.2% rise in 2024, following a historic 8.7% jump in 2023 driven by record-high inflation. The COLA is funded by payroll taxes collected from workers and employers, up to an annual salary cap that will rise to $184,500 in 2026 from $176,100 in 2025.Social Security Administration Commissioner Frank Bisignano said in a statement that the annual adjustment “is one way we are working to make sure benefits reflect today’s economic realities and continue to provide a foundation of security.” However, many seniors believe the increase won’t be enough to meet rising living costs, reported AP.Polling from AARP shows that many older Americans share that concern. Only 22% of Americans over 50 believe a COLA of around 3% is enough to keep up with inflation, while 77% disagree. According to the MIT Living Wage Calculator, a single adult living in Florence, South Carolina, spends about $10,184 annually on housing, $3,053 on medical expenses and $3,839 on food.Emerson Sprick, director of retirement and labor policy at the Bipartisan Policy Center, said in a statement that cost-of-living increases “can’t solve all the financial challenges households face or all the shortcomings of the program.”The latest adjustment comes as the Social Security Administration faces internal challenges and uncertainty about the program’s long-term future. In July, Treasury Secretary Scott Bessent said the Republican administration was committed to protecting Social Security, hours after comments suggesting that a new children’s savings program signed by President Donald Trump was “a back door for privatising Social Security,” as quoted by AP.

Interest rates are widely expected to remain at 3.75% as Bank of England policymakers prioritise curbing above-target inflation while also monitoring economic growth, according to expert analysis.

The Bank’s Monetary Policy Committee (MPC) is anticipated to leave borrowing costs unchanged when it announces its latest decision on Thursday, marking its first interest rate setting meeting of the year.

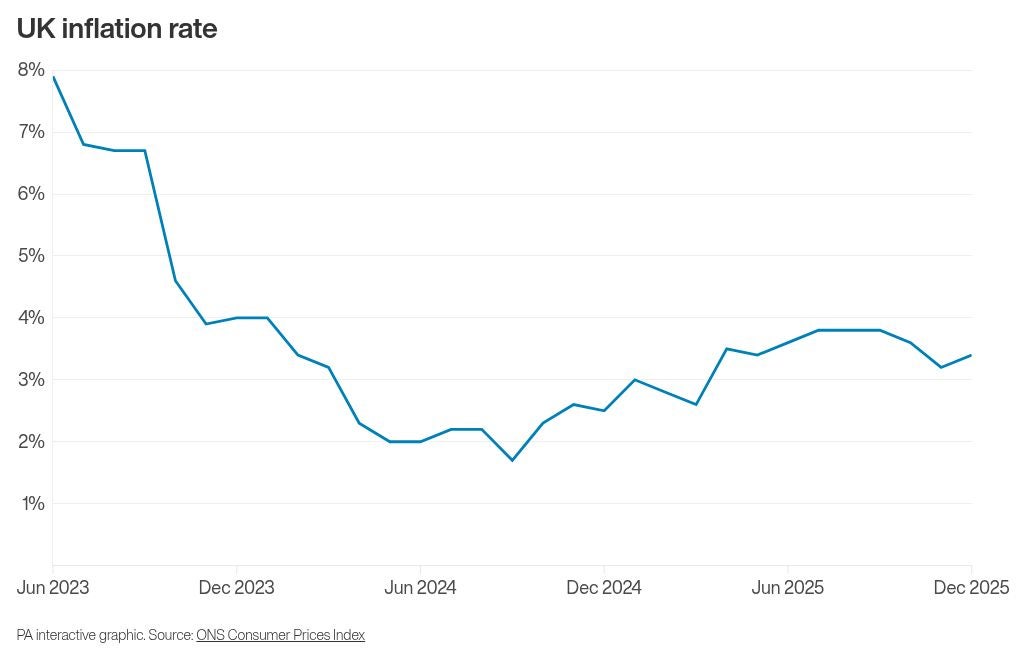

This follows a rate cut delivered before Christmas, which was the fourth such reduction.

At the time, Governor Andrew Bailey noted that the UK had “passed the recent peak in inflation and it has continued to fall”, enabling the MPC to ease borrowing costs. However, he cautioned that any further cuts would be a “closer call”.

Since that decision, official data has revealed that inflation unexpectedly rebounded in December, rising for the first time in five months.

The Consumer Prices Index (CPI) inflation rate reached 3.4% for the month, an increase from 3.2% in November, with factors such as tobacco duties and airfares contributing to the upward pressure on prices.

Economists suggest this inflation uptick is likely to reinforce the MPC’s inclination to keep rates steady this month.

Philip Shaw, an analyst for Investec, stated: “The principal reason to hold off from easing again is that at 3.4% in December, inflation remains well above the 2% target.”

He added: “But with the stance of policy less restrictive than previously, there are greater risks that further easing is unwarranted.”

Shaw also highlighted other data points the MPC would consider, including gross domestic product (GDP), which saw a return to growth of 0.3% in November – a potentially encouraging sign for policymakers.

Matt Swannell, chief economic advisor to the EY ITEM Club, affirmed: “Keeping bank rate unchanged at 3.75% at next week’s meeting looks a near-certainty.”

He noted that while some MPC members who favoured a cut in December still have concerns about persistent wage growth and inflation, recent data has not been compelling enough to prompt back-to-back reductions.

Edward Allenby, senior economic advisor at Oxford Economics, forecasts the next rate cut to occur in April.

He explained: “The MPC will continue to face a delicate balancing act between supporting growth and preventing inflation from becoming entrenched, with forthcoming data on pay settlements likely to play a decisive role in shaping the next policy move.”

The Bank’s policymakers have consistently voiced concerns regarding the pace of wage increases in the UK, which can fuel overall inflation.

India’s budget focuses on infrastructure and defence spending and tax breaks for data-centre investments.

Source link

Business

New Income Tax Act 2025 to come into effect from April 1, key reliefs announced in Budget 2026

New Delhi: Finance Minister Nirmala Sitharaman on Sunday said that the Income Tax Act 2025 will come into effect from April 1, 2026, and the I-T forms have been redesigned such that ordinary citizens can comply without difficulty for ease of living.

The new measures include exemption on insurance interest awards, nil deduction certificates for small taxpayers, and extension of the ITR filing deadline for non-audit cases to August 31.

Individuals with ITR 1 and ITR 2 will continue to file I-T returns till July 31.

“In July 2024, I announced a comprehensive review of the Income Tax Act 1961. This was completed in record time, and the Income Tax Act 2025 will come into effect from April 1, 2026. The forms have been redesigned such that ordinary citizens can comply without difficulty, for) ease of living,” she said while presenting the Budget 2026-27

In a move that directly eases cash-flow pressure on individuals making overseas payments, the Union Budget announced lower tax collection at source across key categories.

“I propose to reduce the TCS rate on the sale of overseas tour programme packages from the current 5 per cent and 20 per cent to 2 per cent without any stipulation of amount. I propose to reduce the TCS rate for pursuing education and for medical purposes from 5 per cent to 2 per cent,” said Sitharaman.

She clarified withholding on services, adding that “supply of manpower services is proposed to be specifically brought within the ambit of payment contractors for the purpose of TDS to avoid ambiguity”.

“Thus, TDS on these services will be at the rate of either 1 per cent or 2 per cent only,” she mentioned during her Budget speech.

The Budget also proposes a tax holiday for foreign cloud companies using data centres in India till 2047.

Netflix’s exciting February line up revealed

Netherlands’ goods exports to US fall 4.7% in Jan-Oct 2025

I Tested 10 Popular Date-Night Boxes With My Hinge Dates

-

Sports5 days ago

Sports5 days agoPSL 11: Local players’ category renewals unveiled ahead of auction

-

Tech1 week ago

Tech1 week agoStrap One of Our Favorite Action Cameras to Your Helmet or a Floaty

-

Sports1 week ago

Sports1 week agoWanted Olympian-turned-fugitive Ryan Wedding in custody, sources say

-

Entertainment1 week ago

Entertainment1 week agoThree dead after suicide blast targets peace committee leader’s home in DI Khan

-

Tech1 week ago

Tech1 week agoThis Mega Snowstorm Will Be a Test for the US Supply Chain

-

Sports1 week ago

Sports1 week agoStorylines shaping the 2025-26 men’s college basketball season

-

Fashion1 week ago

Fashion1 week agoSpain’s apparel imports up 7.10% in Jan-Oct as sourcing realigns

-

Entertainment1 week ago

Entertainment1 week agoUFC Head Dana White credits Trump for putting UFC ‘on the map’