Business

Here’s what to expect for commercial real estate in 2026

A version of this article first appeared in the CNBC Property Play newsletter with Diana Olick. Property Play covers new and evolving opportunities for the real estate investor, from individuals to venture capitalists, private equity funds, family offices, institutional investors and large public companies. Sign up to receive future editions, straight to your inbox.

The 2025 economy wasn’t as robust as anticipated — and that’s shaping the commercial real estate outlook for 2026. The economy has slowed down, unemployment is up and construction has taken a bit of a breather across most sectors.

This year saw increases in both tariffs and immigration restrictions. Together, those have raised costs for builders and developers. But interest rates have also come down, which is starting to unlock more capital, albeit slowly and cautiously.

Here’s what you can expect for the year ahead.

General investment

The many and varied outlook reports from just about every commercial real estate firm out there, as well as related consulting and financial services firms, use words like “new equilibrium” (Colliers), “firmer fundamentals” (Cushman & Wakefield), “ongoing recovery” (KBW) and “signs of price stability” (CoStar).

Looking at specifics for the year ahead, CRE leaders are slightly less optimistic than they were ahead of 2025, according to a Deloitte survey of 850 global chief executives and their direct reports at major real estate owner and investor organizations across 13 countries. Eighty-three percent of respondents said they expect their revenues to improve by the end of 2026 compared with 88% last year. Fewer respondents said they plan to increase spending, while more expect to keep spending flat. Still, 68% said they anticipate higher expenses in 2026.

Most respondents said they do expect the cost of capital to improve, and growth is expected across most asset classes. Overall sentiment is down from last year but well above that of 2023, according to the Deloitte survey.

Looking specifically at the U.S., the commercial real estate sector is entering 2026 with renewed momentum, clearer visibility, and growing optimism across both leasing and the capital markets landscape, according to a forecast from Cushman & Wakefield. It notes that despite uncertainty surrounding tariffs, a volatile policy backdrop, tightening immigration and episodes of financial market stress this year, the economy was more resilient than expected, driven in large part by artificial intelligence.

“As we head into 2026, the tone has shifted meaningfully,” said Kevin Thorpe, chief economist at Cushman & Wakefield. “There is still risk on both sides of the outlook, but we’ve moved past the peak levels of uncertainty, and confidence in the CRE sector is building. Capital is flowing again, interest rates are moving lower, and leasing fundamentals are generally stabilizing or improving. If 2025 was a test of resilience, 2026 has real potential to reward it.”

Capital is reengaging, according to Colliers, which predicts the industry is, “entering a new equilibrium.” Forecasters there point to the bottoming out of office demand and new growth in industrial, thanks, again, to AI.

PwC also emphasizes that capital began flowing again in the second half of this year, “but selectively.”

“The deal environment rewards those who can combine data-driven insight with strategic conviction. For clients, the challenge—and the opportunity—is to navigate a landscape where liquidity, technology, and consolidation are redefining the meaning of value creation in real assets,” according to a PwC report.

The share of investors who say they expect to increase their commercial real estate investments over the next six months fell in the fourth quarter of this year from the previous quarter in every sector except retail, according to a survey from John Burns Research and Consulting. Multifamily investor sentiment weakened for the fourth consecutive quarter.

“Investors cited headwinds that included elevated interest rates, economic uncertainty, and local regulatory burdens. 49% of investors expect to hold their CRE exposure at the current level over the next 6 months, in line with the past two quarters,” according to the report.

Capital markets

“Capital Markets Reawakening” – that’s the headline from Colliers, which says pricing has found a floor and deal velocity is rising. Colliers forecasts a 15% to 20% increase in sales volume in 2026 as institutional and cross-border capital reenters the market.

Capitalization rates seem to be ready to move lower next year, according to a forecast from CoStar. Its data is already showing hints of this in the multifamily and industrial sectors, where vacancies have peaked and rent growth is picking up.

CoStar also notes deal activity is picking up, with third-quarter sales volume up more than 40% year over year, and banks are “easing back into commercial real estate lending,” according to the report.

Bond markets are following suit, showing new appetite for risk. CoStar points to the narrowing spread between government and corporate bond yields to roughly 1 percentage point (well below the historical average), “typically a precursor to greater real estate investment and firming prices.”

This tracks with the Cushman & Wakefield outlook, which also notes that in 2025 debt costs eased, lenders reentered the market and institutional capital returned, “supporting a broad-based revival in deal activity.”

Lending was up 35% year over year, institutional sales activity increased 17% through October, and pricing has “largely reset, presenting the market with compelling opportunities for yield and income generation,” Cushman & Wakefield found.

Specific sectors

The office market is now widely believed to have bottomed, and assets are showing early signs of price stability.

Vacancy rates are expected to drop below 18% as more tenants return to the market, leverage expiring leases and prioritize hospitality-driven workplaces that support hybrid work, according to Colliers.

There will continue to be a flight to quality in office, as Class A buildings in many markets are now nearly fully occupied. Office construction is also at its lowest level in more than three decades, according to Yardi.

Cushman & Wakefield forecasts continued growth in San Francisco; San Jose, California; Austin, Texas; New York; Atlanta; Dallas; and Nashville, Tennessee, which posted strong positive absorption in 2025, supported by AI expansion and diversified job growth.

“For large office users looking to secure high-quality space, the message is clear: if you find the right space, act decisively,” said James Bohnaker, principal economist at Cushman & Wakefield. “There is strong demand for new, high-quality space and not enough of it to go around. And given the limited construction pipeline, it’s going to get even tighter.”

Industrial has also seen a huge drop in construction, down 63% since 2022, according to the Colliers report. Vacancy is peaking and net absorption is set to jump to 220 million square feet, as reshoring, manufacturing and data centers fuel demand.

Retail is already undergoing a major shift in how and where companies are leasing space, according to Brandon Svec, national director of U.S. retail analytics at CoStar.

He points to nearly 26 million square feet of ground floor retail leased in nontraditional properties in the first three quarters of 2025, including multifamily, student housing, hospitality and office.

Retailers are embracing smaller footprints, with the average retail lease signed over the past four quarters falling below 3,500 square feet for the first time since CoStar began tracking this in 2016. This is being driven largely by restaurant and service operators such as Starbucks, Chipotle, Chick-fil-A, Jersey Mike’s, Dunkin’ and McDonald’s, according to Svec, who noted the growing appeal of walkable, mixed-use retail environments over traditional big-box formats. He does have a warning though.

“Significant uncertainty remains around the impact of tariffs on an already fragile consumer. While suppliers and retailers have largely absorbed these costs to date, many have signaled that price increases are imminent. With consumers already showing some signs of spending fatigue, tariff-related price hikes could further strain household budgets and dampen discretionary spending,” Svec wrote in a report.

Multifamily rents are starting to ease, as a record level of new supply continues to make it through the pipeline.

“Multifamily has led investment sales volume since 2015, and there are no signs of this changing. However, its share of total volume is expected to ease somewhat as investors allocate more capital to office, data centers, and retail,” according to the Colliers report.

Data centers have been the darling of 2025, with demand significantly outpacing supply. Deloitte called the sector, “a clear bright spot in the U.S. commercial real estate landscape.” It pointed to nine major global markets where 100% of the new construction pipeline is already fully pre-leased.

Data centers do, however, face headwinds in financing, grid capacity, zoning and local politics.

“Friction is building as communities push back on data center development. A few projects have already been abandoned, and more are expected to be shelved in 2026,” according to the Colliers forecast.

REITs

Public-to-private REIT transactions and portfolio mergers are likely to dominate in the year ahead as listed valuations lag private market pricing, according to a report from PwC. That will be driven by considerations of scale, governance credibility and cost of capital.

“Expect accelerated M&A as capital concentrates, AI exposes inefficiencies, and platforms converge—real assets are entering a new phase defined by intelligence, integration, and scale-driven opportunity,” wrote Tim Bodner, global real estate deals leader at PwC.

As for the real estate investment trust stocks, they were the real laggards of 2025, but could be poised to outperform in 2026, according to a forecast from Nareit, the REIT industry association. It points to a divergence between stock market valuations and REIT valuations and an ongoing divergence between public and private real estate valuations.

“These will close, and one or both could happen in 2026. If they do, we expect REITs to outperform based on our own historical analysis and their ongoing strong operational performance and balance sheets,” the report said.

As governments across the world restricted the movements of their citizens during Covid lockdowns from 2020, people spent more time online. We bought more online and socialised more online, and this brought us closer to the people who want to scam us. At the same time, realistic video impersonations, voices, websites, and texts became more commonplace, and scammers increased their use of social media including WhatsApp.

Business

NaBFID signs pact with PDCOR to expand advisory support for state projects – The Times of India

The National Bank for Financing Infrastructure and Development (NaBFID) has signed a Memorandum of Agreement with Projects Development Company of Rajasthan Limited (PDCOR) to strengthen advisory services for state and city-level infrastructure projects.The agreement will also allow both institutions to jointly explore financing and transaction advisory opportunities, including transaction structuring, commercial and technical due diligence, and support for financial closure of projects undertaken by state governments and urban local bodies across India, according to PTI.“This collaboration seeks to enhance access to long-term institutional finance for State Governments and Urban Local Bodies, while strengthening the infrastructure advisory and financing ecosystem,” Rajkiran Rai G., Managing Director of NaBFID, said.He added that the partnership would help both institutions jointly pursue project advisory opportunities, develop replicable financing frameworks, accelerate financial closures and mobilise capital across the infrastructure value chain.Monika Kalia, DMD-CFO, NaBFID, said the tie-up would leverage the strengths of both organisations to provide much-needed advisory support to states and urban local bodies for impactful urban infrastructure projects.Dileep Chingapurath, Chief Executive Officer, PDCOR, said the agreement would address the long-felt need for end-to-end professional support to structure and mobilise sustainable financing solutions, particularly for state governments and their agencies.“Through this collaboration, both institutions aim to enhance the quality of project preparation, mobilise institutional capital more effectively and accelerate the implementation of sustainable infrastructure projects across states and municipalities,” he said.NaBFID is a Development Financial Institution focused on long-term infrastructure financing, while PDCOR is an undertaking of the Government of Rajasthan.

Business

Explained: On way to 4th largest, how India slipped to 6th rank & what it means for 3rd largest economy dream – The Times of India

In April 2025 when the International Monetary Fund (IMF) released its World Economic Outlook, India was seen overtaking Japan to become the world’s fourth largest economy by the end of 2025-26. One year later, India has slipped to the sixth position on the largest economies rankings, with the United Kingdom reclaiming its spot as the fifth largest economy.In fact, IMF’s latest World Economic Outlook (April 2026) sees India sitting at the sixth spot this financial year too. This projection comes even as India has grown better than expected in FY26 and is seen retaining its tag of being the world’s fastest growing major economy.What has led to the sudden fall? Why has India dropped to the sixth position, falling behind the UK, instead of overtaking Japan to become the fourth largest economy? And what does this setback mean for its dream of becoming the third largest economy by the end of this decade? We decode:

Data drive: India projected as 4th largest, but fell to 6th spot

First let’s look at some IMF data to see which way the Indian economy was headed in April 2025, and what the April 2026 outlook data suggestsAs per April 2025 estimates of IMF, India’s economy would have been at $4601.225 billion at the end of FY 2025-26, overtaking Japan which was estimated at $4373.091 billion. The UK at the 6th spot was projected to have a nominal GDP of $4040.844 billion.However, as per the April 2026 estimates, India’s economy had a nominal GDP of $4,153 billion at the end of FY 2025-26, with the UK overtaking it with $4,265 billion GDP. Japan’s GDP is seen at $4,379 billion.As the above estimates show, India’s GDP estimates have seen a drop over one year, while UK’s nominal GDP has grown better than expected. Japan has been steady.So, what went wrong? Blame the rupee and GDP data itself!

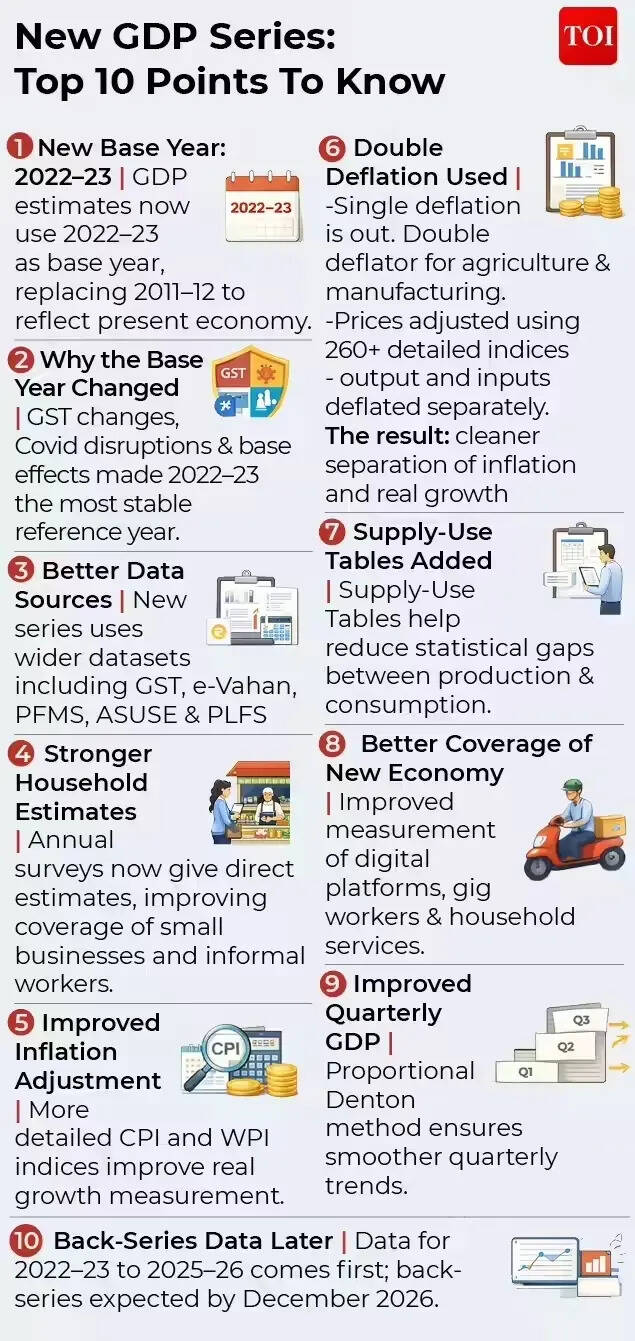

Rupee Depreciation Blow & New GDP Series

The first thing to understand is that IMF’s data on the size of a country’s nominal GDP is in dollar terms. Hence, with global rankings based on dollar‑denominated GDP, they are highly sensitive to exchange rate movements. The biggest party pooper for India’s dream of becoming the fourth largest has been the rupee’s slide. The Indian currency has depreciated more than expected over the last year, dropping from 84.57 versus the US dollar in 2024 to 88.48 in 2025, as per IMF data. The IMF estimates see it at 92.59 this year.Several factors have contributed to the rupee’s decline, including capital outflows, uncertainty related to India-US trade deal up until February, and the recent Middle East conflict which has raised crude oil prices and India’s import bill. Also, the RBI while actively managing volatility in the forex market, is not targeting any particular level of the rupee.Arun Singh, Chief Economist, Dun & Bradstreet India says that India’s recent slip to sixth place in global GDP rankings does not reflect a weakening of the economy, but is largely the result of currency conversion effects and a one‑time statistical revision.The rupee’s depreciation from 2024 to 2026, has mechanically compressed India’s GDP in dollar terms, effectively halving apparent growth despite strong domestic expansion, says Arun Singh.According to Ranen Banerjee, Partner and Leader, Economic Advisory Services, PwC India, GDP in US dollar terms would shave off with rupee depreciation. “We have had almost 7-8% depreciation over the last few months owing to the conflict and portfolio outflows. Thus, in effect in US dollar terms, it is close to shaving out almost a year’s nominal GDP,” he tells TOI.And it’s not just about the Indian economy. The United Kingdom which has overtaken India to bag the 5th spot again also has economic factors working in its favour. UK’s GDP growth at 0.5% has recently beaten forecasts of 0.1% by a wide margin. Not only that, its currency – pound – has actually appreciated against the US dollar.The second factor that has impacted the rankings is India’s adoption of a new base year for its latest GDP series. As per the new data, which also makes use of a more refined methodology, the size of India’s nominal GDP in rupee terms has gone down. Sample this: As per the older base year of 2011-12, India’s GDP at the end of 2025-26 would have been Rs 35,713,886 crore. But under the new series, it is estimated to be Rs 34,547,157 crore. The new calculation methodology and base year revision presents a more accurate picture of the size of the Indian economy.Hence the currency effect has been compounded by a one‑time downward revision following India’s shift to a new GDP base year, which has lowered reported nominal levels without affecting real activity.

Does India’s drop to 6th indicate fundamental weakness?

Experts are confident that India’s growth story is intact and fundamentally strong, a fact that is reflected in projections of it continuing to be the world’s fastest growing major economy. They see technical factors behind the current slip, rather than any deterioration in economic fundamentals.It’s also interesting to note that while India will be the sixth largest economy in FY27, in the upcoming financial year, it is likely to overtake both the UK, and Japan to bag the fourth spot.Arun Singh of Dun & Bradstreet India explains this resilience with numbers:IMF World Economic Outlook (April 2026) data show that India’s GDP at current prices in domestic currency rose strongly from ₹318 trillion in 2024 to ₹346.5 trillion in 2025 and further to ₹384.5 trillion in 2026, translating into robust nominal growth of about 8.9% in 2024–25 and nearly 11% in 2025–26, among the fastest globally. In contrast, other large economies recorded more moderate domestic nominal growth – around 5% in the US, roughly 4% in China, 3–5% in the UK, 3–3.5% in Germany, and lower or volatile growth in Japan – underscoring India’s strong underlying momentum. In times of global economic turmoil, while GDP growth is expected to take some hit, most agencies and experts have pegged India’s growth to be strong. Incidentally, the IMF has even marginally raised its GDP growth forecast for FY27 to 6.5% despite the ongoing Middle East conflict.

“In India, growth for 2025 is revised upward by 1.0 percentage point relative to October, to 7.6 percent, reflecting the better-than-expected outturn in the second and third quarters of the fiscal year and sustained strong momentum in the fourth quarter,” IMF said in its latest outlook. “For 2026, growth is revised upward moderately by 0.3 percentage point (0.1 percentage point relative to January) to 6.5 percent, led by positive contributions from the carryover of the strong 2025 outturn and the decline in additional US tariffs on Indian goods from 50 to 10 percent, which outweigh the adverse impact of the Middle East conflict. Growth is projected to stay at 6.5 percent in 2027,” it added.

Will India become 3rd largest anytime soon?

The rupee depreciation and the nominal GDP revision has also pushed back India’s dream of becoming the third largest economy by the end of this decade. In the October 2025 estimates, IMF had said that India will overtake Germany to become third largest by FY30. However, the April 2026 projections see it reaching the third rank only by FY 2030-31.Experts point to the rupee’s depreciation versus the dollar to note that the road ahead is likely to be uncertain. Madan Sabnavis, Chief economist, Bank of Baroda is confident that India will continue to do well in the coming years.“We will definitely improve in terms of GDP growth which will be higher than that of other countries especially UK and Japan which are just above us. However, the rupee value will finally determine how India gets placed on the global scale,” he told TOI.Ranen Banerjee of PwC India sees rupee beginning to get support with the conflict containment, relatively lower oil prices and portfolio flow reversals with valuations getting attractive in recent times. “Thus, we should not be experiencing any further sharp depreciation of the rupee in the immediate term provided the conflict does not escalate and oil prices relatively softening from their highs and come down to a range of $85-90 a barrel,” he says.For Arun Singh of Dun & Bradstreet, looking ahead, India’s relative position in US dollar‑based GDP rankings will remain highly sensitive to currency movements rather than domestic growth dynamics. “Continued global dollar strength or capital‑flow volatility may cause periodic slippage in rankings despite robust fundamentals. Sustaining external macro stability and limiting undue rupee volatility will be crucial for India’s strong growth performance to translate more fully into higher global economic rankings,” Arun Singh told TOI.The Indian economy, largely driven by domestic fundamentals, is not immune to external shocks. High US tariffs of 50% from August 2025 to early February, and the ongoing US-Iran war have spelt back-to-back shocks for the economy. Even as experts stress on the resilience of the growth story, the vulnerability to higher crude oil prices, and other global supply chain disruptions is a reality. In such a scenario, India may well have to contend with fluctuating world rankings, while banking on its strong GDP growth to tide over disruptions.

Oklahoma wins 4th NCAA women’s gymnastics title in 5 years

Scams have grown more sophisticated, but people are fighting back

Netflix star targeted by imposters after suspicious social media activity

-

Politics1 week ago

Politics1 week agoIndian airlines hit hardest after Dubai limits foreign flights until May 31

-

Entertainment6 days ago

Entertainment6 days agoPalace left in shock as Prince William cancels grand ceremony

-

Politics1 week ago

Politics1 week agoChinese, Taiwanese will unite, Xi tells Taiwan opposition leader

-

Sports6 days ago

Sports6 days agoThe case for Man United’s Fernandes as Premier League’s best

-

Business6 days ago

Business6 days agoUK could adopt EU single market rules under new legislation

-

Entertainment1 week ago

Entertainment1 week agoDua Lipa hits major career high ahead of wedding with Callum Turner

-

Business1 week ago

Business1 week agoThe FAA wants gamers to apply for air traffic control jobs

-

Sports1 week ago

Sports1 week agoLamar Jackson hits back at critics with faithful message on social media