Business

Fundamental shift from savers to investors: What Indian households are doing with their money? – The Times of India

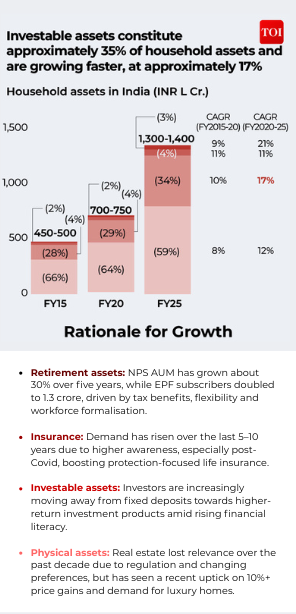

For years, Indian families have saved in gold, stored cash, and put money in tangible assets to safeguard their future. But now, there’s a noticeable shift is visible as more Indian households are moving away from old saving ways and putting their money to work through investments.India’s total household wealth, by the end of FY25, stood at Rs 1,300-1,400 lakh crore. Of this, investable financial assets stand at almost 35% of the total, growing at nearly 17% over the past five years, according to a recent Bain–Groww report, titled How India Invests.

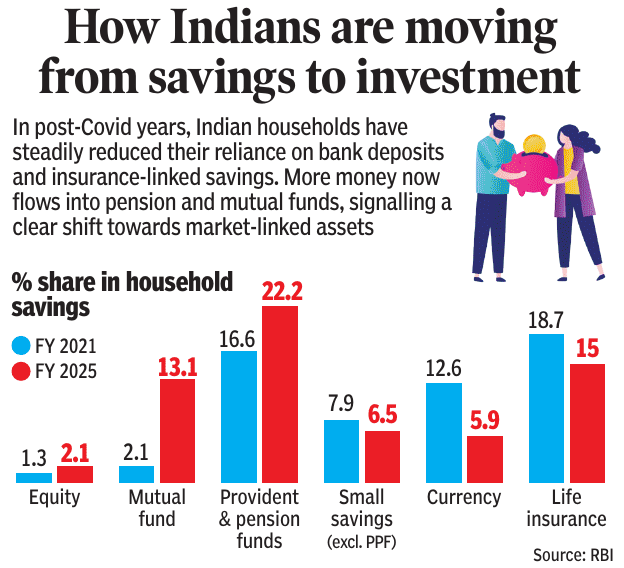

Household wealth has gone through a shift since the Covid era. Indians have moved from traditional fixed deposits toward market-linked instruments like mutual funds, pension funds and listed equities, which are growing at a fast rate, far outpacing deposits growth.Over the last five years, individual investor base in the country has expanded sharply, going from around 3 crore investors in 2019 to over 12 crore by 2025, according to the Market Pulse December 2025 report by the National Stock Exchange of India (NSE), India. In 2025 alone, households invested a whopping Rs 4.5 lakh crore into equity markets, both directly and indirectly through mutual funds. This, pushed the overall household investment in equities since 2020 to around Rs 17 lakh crore. In FY25, mutual fund assets under management (AUM) held by individuals reached Rs 41 lakh crore, driven by double participation by households, going from 5–6% to 10–11%, and increasing popularity of systematic investment plans (SIPs).According to RBI data, equity formed 1.3% of household savings in FY2021, but its share increased to 2.1% by FY2025. Similarly, mutual funds recorded a significant jump over the same period, with their share rising sharply from 2.1% to 13.1%. Contributions to provident and pension funds also grew, increasing from 16.6% in FY2021 to 22.2% in FY2025.In contrast, traditional savings instruments saw a decline. Small savings, excluding PPF, fell from 7.9% to 6.5%, while the share of currency in household savings dropped steeply from 12.6% to 5.9%. Life insurance also witnessed a reduction, with its share slipping from 18.7% in FY2021 to 15% in FY2025.Gradually, households reduced their dependence on bank deposits and insurance-based savings. Instead, investments in pension schemes and mutual funds have gathered pace, pointing to a broader shift towards market-linked financial products.

Mutual funds, stocks, SIPs: Who is choosing what?

Salaried households show a clear preference for mutual funds, particularly through SIPs, reflecting a tilt toward disciplined, professionally managed investing aligned with long-term financial goals, according to the Bain report. In contrast, business owners display a stronger inclination toward direct equity investments, marked by higher trading frequency and a greater appetite for risk. Within mutual funds, SIPs remain the dominant entry route, while lump-sum investments are steadily gaining traction as investors mature, build market confidence, and increase their risk tolerance.

Interest in investing spiked after Covid?

Covid didn’t just change daily life, it changed how Indians invest. Retail participation in the stock market rose sharply after the pandemic, driven by a mix of high liquidity, lower household spending during lockdowns and the flexibility of work-from-home, Rohit Shah, Certified Financial Planner and founder of Getting You Rich told TOI. Shweta Rajani, head of mutual funds at Anand Rathi Wealth Limited, pointed out that mutual funds made up only 4–5% of household financial assets between FY15 and FY20, but this share nearly doubled from around 5% in FY20 to close to 10% by FY25. At the same time, direct equity investments also grew sharply, rising from about 4% of household assets in FY20 to around 9% by FY25. “Together, these shifts indicate a clear move away from traditional savings instruments towards market-linked investments, indicating investors are comfortable with equity as an asset,” the expert added.Meanwhile, Nirav Karkera, head of research at Fisdom believes that Covid acted more as an accelerator than a starting point as the shift had already begun after demonetisation. The switch made Indians comfortable with digital payments and later with digital investing. By the time the pandemic arrived, systems such as Aadhaar-based KYC, easy online transactions and awareness campaigns like Mutual Fund Sahi Hai had removed most barriers. “When the pandemic hit, investors suddenly had the time and urgency to reflect on their personal finances. More importantly, the infrastructure to execute decisions with almost zero friction already existed. Willingness, ability and accessibility came together and translated into action. The sharp and mostly linear market recovery that followed further strengthened confidence, pulled in fence-sitters and accelerated the broader financialisation of household assets that was underway,” Nirav added.

Change in India’s risk appetite

India’s shift from saving to investing is being driven less by thrill-seeking and more by necessity, experts said. Traditional savings instruments are increasingly failing to protect wealth, as post-tax returns often fall below inflation, steadily eroding purchasing power. “What looks like rising risk appetite is partly a change in the understanding of risk itself,” said Karkera, adding that investors now see the risk of staying idle and falling behind as greater than the risk of market volatility. This shift has been reinforced by deeper financial awareness, easier access to investing through fintech platforms, and stronger regulation, said Rajani. The expert further noted that SIPs, simplified KYC and digital onboarding have lowered entry barriers, while a generational change is reshaping attitudes, older investors prioritised capital preservation, but younger earners, facing higher inflation and lower real interest rates, are more focused on long-term wealth creation using growth assets. However Shah cautioned that rising participation does not always mean better risk management. “Four structural factors drive this shift: financial literacy campaigns, fintech accessibility reducing entry barriers, higher equity allocations in mutual fund inflows, and rising per capita incomes. Yet risk appetite may be overstated. Data on retail trading patterns shows concentration in speculative segments, suggesting investors confuse market participation with risk management. Many haven’t weathered a bear market, leading to underestimation of downside volatility,” Shah told TOI.

Here’s what is driving the investors:

A combination of demographic change, regulatory support, digital access and strong market returns has accelerated India’s move from traditional savings to investing.

Demographic changesYounger investors are driving India’s shift from traditional savings to investing, with NSE data showing that more than half newly registered investors are below 30. At the same time, women are steadily increasing their presence in financial markets. As of November 2025, women account for nearly a quarter of India’s investor base, with their share in the NSE’s individual investor pool remaining stable at almost 24%.Digital transformationDigital platforms have emerged as the main entry point for retail investors in the country, with almost 80% of direct equity investors and around 35% of mutual fund investors investing through digital channels. According to the Bain report, driven by app-based onboarding, paperless KYC and fintech-led distribution, platforms such as Groww, Zerodha and Upstox have simplified investing, brought in millions of first-time investors, and together account for almost 80% of India’s retail equity investor base.Going beyond metro citiesInvestment activity is increasingly coming from smaller cities. Around 55–60% of new SIP registrations now originate from B30 cities, highlighting the growing role of Tier-2 and Tier-3 regions in driving mutual fund growth.Rising financial literacy and awarenessThe spread of regional and digital financial content across YouTube, Instagram and fintech platforms has made investing concepts more accessible. Regulatory awareness campaigns by AMFI — including “Mutual Funds Sahi Hai” and “Bharat Nivesh Yatra” — have further boosted investor education.Market performance reinforcing trustSustained returns have strengthened long-term investor confidence. The Nifty 50 and Sensex delivered 10–15% returns over the last decade, while equity-oriented mutual funds have significantly outperformed traditional fixed deposits over the past five years.

Women and GenZ hit investment markets

GenZYounger investors are emerging as key drivers of the shift from traditional savings to investment. Data from the NSE shows that more than half, almost 56%, of newly registered investors are below 30. Mutual fund trends also reflected this shift, with 55% of investors under 40 and the 20–30 age group emerging as the fastest-growing segment in the top 100 cities.Comparing the contribution of GenZ and millennials, Rohit Shah said that according to the data, both cohorts contribute meaningfully, but with distinct patterns.“GenZ dominates app-based trading volumes due to digital nativity and lower capital requirements. Millennials drive mutual fund and long-term investments through larger disposable incomes and established goals.” He further added, after the market expansion happening after the pandemic, benefited both simultaneously, “making it difficult to isolate one generation as the primary driver. The real story lies in democratization across age groups, not generational dominance.The equity shift is broad-based across age groups according to AMFI’s age-wise distribution of individual investor AUM. Gen Z investors (under 25 years) have allocated nearly 65% of their assets to equity, Rajani told TOI. Millennials (25–44 years), meanwhile, “show the highest equity allocation at approximately 75.5%, and importantly, even investors above 58 years of age maintain a meaningful equity allocation of around 54%”Nirav Karkera, head of research at Fisdom, highlighted a different approach, saying that while millennials currently lead the equity surge, the baton is likely to pass to Gen Z in the coming years. “Gen Z is still in the early stage of their earning life, where consumption tends to dominate. At the same time, they are arguably the most financially aware generation we have seen. They understand the language of money much earlier than millennials did at their age. Once their incomes rise and they have surplus capital, they are likely to play an even bigger role than millennials in shaping investment patterns. For now, millennials are doing the heavy lifting, but the baton looks set to pass smoothly to Gen Z.”WomenAs of November 2025, women account for nearly a quarter of India’s investor base, highlighting their growing presence in financial markets. Data from NSE shows that over the corresponding period, women’s share in the individual investor base has remained stable at 24.7% over the corresponding period. Among the top five states by registered investors, Maharashtra leads with women comprising 28.8% of its investor pool, up from 25.6% in FY23, followed closely by Gujarat at 28.1% (26.6% in FY23). In contrast, Uttar Pradesh, despite being the second-largest state by investor count, continues to lag, with women forming 18.9% of investors, though this marks an improvement from 16.9% in FY23.Encouragingly, nearly 53% of Indian states now report female investor participation above the national average, compared to 44% in FY23. Smaller regions are emerging as frontrunners in gender inclusion, with Goa (33.1%), Mizoram (32.4%), Chandigarh (32.2%), Sikkim (31.1%) and Delhi (30.9%) leading the way – reflecting rising financial awareness, greater workforce participation, and improved access to investment avenues among women. Mutual funds also saw rising participation from women, particularly in B30 cities, where the share of women investors climbed from 20% to 25% over the past five years. In the top 30 cities, women now make up nearly 35% of mutual fund investors as of FY25, accompanied by a sharper rise in average MF folio sizes between FY19 and FY24.

Short-term or long-term: Where are Indians putting their money?

Indian investors are participating across both short-term trading and long-term wealth building, but experts say the balance is slowly tilting toward the latter. In the immediate post-Covid phase, many first-time investors entered markets with speculative intent. However, that period helped break psychological barriers. “Once investors experienced volatility firsthand rather than hearing about it abstractly, they started building familiarity, confidence and a basic understanding of market behaviour,” said Karkera, adding that the early rush acted as a gateway to more mature participation.Rajani told TOI that the trend is driven by long term objectives rather than short term. The expert pointed to AMFI’s SIP holding-period analysis, which shows that the share of SIP assets held for over five years has jumped from 11% to 29% in the past five years, while investments held for less than a year have fallen sharply from 41% to 23%.Meanwhile Shah said that even though “retail trading volumes have grown exponentially—NSE data shows consistent month-on-month increases in F&O participation. Simultaneously, mutual fund SIP adoption remains strong, but it’s overshadowed by trading activity. With fixed deposit yields compressed by falling interest rates, investors are chasing equity returns without corresponding time horizons. The evidence suggests a bifurcation: disciplined SIP investors versus growing trading populations driven by short-term performance metrics.”

Are there any risks for the investment express?

Shah warned that many new investors entered the market during a long bull run, and historically, market corrections of 30–50% happen every 7–10 years. Therefore, a prolonged downturn could lead to panic selling, especially among first-time investors with little experience of market volatility. Meanwhile, in the short term, market ups and downs may push some investors to move money into safer options like debt funds. Investors also tend to chase assets that have done well recently, such as gold and silver. However, Rajani pointed out that these shifts are temporary and not a fundamental change. “Over the long term, the broader trend toward equity investing is expected to continue as investors looking for inflation-beating returns to meet long-term financial goals.”Karkera also highlighted that even though risks remain, they are manageable. He noted that lower equity returns or bouts of market volatility could cause short-term, speculative investors to step back, and better performance in fixed-income or real assets may temporarily pull some money away from equities. However, the larger shift is firmly in place thanks to improved investor awareness, growing digital access. “Growth may pause or plateau intermittently, but the long-term trajectory of retail participation still feels upward.”

Still room to grow

Despite the rapid shift, India continues to lag developed markets. Mutual funds and equities account for just 15–20% of household investable assets, compared with 50–60% in countries like the US and Canada, highlighting significant headroom for future growth.As the Bain report notes: Over the next decade, mutual fund AUM is projected to cross Rs 300 lakh crore, while direct equity holdings could approach Rs 250 lakh crore, supported by deeper penetration in tier-2 and tier-3 cities, regulatory reforms and investor education initiatives.

: Nifty50 recovers from losses, goes above 24,400; BSE Sensex up over 300 points – The Times of India")

: Nifty50 opens above 23,100; BSE Sensex rises over 700 points as oil goes below 0 – The Times of India")

: Nifty50 opens above 23,200; BSE Sensex up over 700 points – The Times of India")

: Nifty50 opens below 23,600; BSE Sensex down over 900 points on continuing US-Iran war – The Times of India")

The Government has been urged to stick to its pledge to ban ticket touting amid concerns the policy will be left out of next month’s King’s Speech.

In November, the Government announced that new rules making it illegal to resell tickets for live events for profit would end the “industrial-scale” touting that has caused misery for millions of fans.

Ministers confirmed plans to make it illegal for tickets to concerts, theatre, comedy, sport and other live events to be resold for more than their original cost.

The Labour manifesto promised stronger protections to stop consumers being scammed or priced out of events by touts, who frequently use bots to buy tickets in bulk the moment they go on sale, which they can then sell on for huge mark-ups on secondary ticketing websites.

The proposed rules make it illegal for tickets to be sold at a price above the face value – defined as the original price plus unavoidable fees including service charges.

Service fees will be capped to prevent the price limit being undermined by platforms, which will have a legal duty to monitor and enforce compliance, and individuals will be banned from reselling more tickets than they were entitled to buy in the initial sale.

A host of globally renowned artists have backed the plan, including Radiohead, Dua Lipa and Coldplay.

Following a report in the Guardian that the minister responsible for the policy, Ian Murray, had told music industry groups not to worry if the measure was not part of the King’s Speech on May 13, the Government said it required new primary legislation that it was working to deliver at the earliest opportunity.

A Government spokeswoman said: “Ticket touts are a blight on the live events industry, causing misery for millions of fans.

“We set out decisive plans last year to stamp out touting once and for all, and we are committed to delivering on these for the benefit of fans and industry.”

The music industry and Which? raised concerns about the suggestion of any delay, as sites appeared to show touts selling tickets for the Radio 1 Big Weekend in Sunderland well above the two-ticket limit for buyers and at vastly inflated prices.

Annabella Coldrick, chief executive of the Music Managers Forum, said: “2026 was supposed to mark this Government moving ‘from announcements to action’ but we have little evidence of this to date.

“A ban on ticket touting was one of only two music-related commitments in the Labour manifesto, alongside fixing EU touring.

“These are widely supported, pro-growth measures that will deliver tangible benefits to the British public. However, if ticket resale legislation is not presented in the King’s Speech, it will have the opposite effect and continue to cost those constituents hundreds of millions of pounds a year.

“This Government needs to stand by its promises and get it done.”

Adam Webb, campaign manager at FanFair Alliance, said: “The Government has a big decision to make: will they ‘put fans first’ or not?

“Last November, ministers committed to ‘bold new measures’ to ban online ticket touting and support consumers.

“Enacting these measures should be a no-brainer but, if legislation is not presented in the upcoming King’s Speech, the cycle of industrial-scale exploitation will continue.”

Lisa Webb, consumer law expert at Which?, said: “The Government has promised to put fans first but, if this legislation is not included in the King’s Speech, the only ones celebrating will be the rip-off secondary ticketing websites and online touts.”

The approval came as Donald Trump is to attend a dinner with billionaire Paramount backers the Ellisons.

Source link

Business

France Ends Airport Transit Visa Requirement for Indian Travellers | Business – The Times of India

France has lifted the airport transit visa requirement for Indian nationals with effect from April 10, the French Embassy in India announced on Thursday.Indian nationals holding ordinary passports are no longer required to obtain an airport transit visa when passing through the international zone of airports located on French territory during a layover en route to a third country.The change follows a decree amending the 2010 regulations on documents and visas required for the entry of foreigners into French territory. The decree was adopted and published in the French Official Gazette (Journal Officiel) on April 9, 2026.MEA welcomes the moveThe Ministry of External Affairs welcomed the announcement.“We welcome the announcement on the operationalisation of visa-free transit for Indian nationals transiting through French airports,” MEA Spokesperson Randhir Jaiswal said.He recalled that the removal of the transit visa requirement for Indian passport holders was agreed between Prime Minister Narendra Modi and French President Emmanuel Macron during their meeting in Mumbai in February this year.“The government of France has now operationalized this agreement,” Jaiswal added.Who benefitsThe measure applies to Indian nationals transiting through mainland France exclusively by air, remaining in the international airport zone without entering French territory.President Macron had announced during his visit to India in February that measures would be taken to ease travel for Indian nationals via France.

Poll

What do you think is the main advantage of this visa policy change?

The updated procedures have been reflected on the France-Visas platform.

How ‘Michael’ continues to smash the box office despite backlash

Ministers urged to stick to ticket tout ban amid fears of delay

Warner Bros shareholders approve Paramount’s $111bn takeover

-

Fashion1 week ago

Fashion1 week agoFrance’s LVMH Q1 revenue falls 6%, shows resilience amid Iran war

-

Entertainment1 week ago

Entertainment1 week agoIs Claude down? Here’s why users are seeing errors

-

Sports1 week ago

Sports1 week agoPSL 11: Peshawar Zalmi win toss, opt to field first against Quetta Gladiators

-

Tech1 week ago

Tech1 week agoThe Deepfake Nudes Crisis in Schools Is Much Worse Than You Thought

-

Business1 week ago

Business1 week agoStandard Life buys rival in £2b deal to create savings giant

-

Tech1 week ago

Tech1 week agoCYBERUK ’26: UK lagging on legal protections for cyber pros | Computer Weekly

-

Sports1 week ago

Sports1 week agoWorld Cup kit ranking: Which teams will look best in 2026?

-

Tech1 week ago

Tech1 week agoCyber Essentials closes the MFA loophole but leaves some organisations adrift | Computer Weekly