Business

UK inflation: What is the rate and why are prices still rising?

BBC

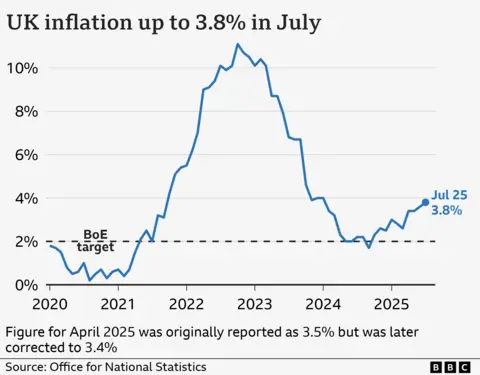

BBCPrices in the UK rose by 3.8% in the 12 months to July, driven by higher air fares, as well as increases in the cost of food.

It means inflation remains above the Bank of England’s 2% target.

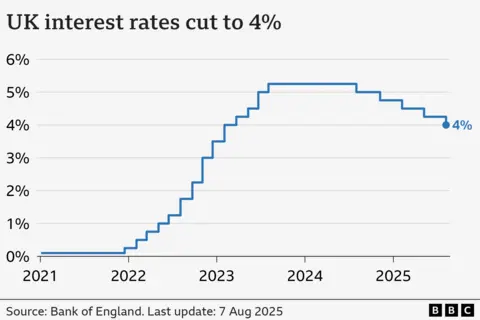

The Bank moves interest rates up and down to try to keep inflation at that level, and has cut interest rates five times since August 2024.

What is inflation?

Inflation is the increase in the price of something over time.

For example, if a bottle of milk costs £1 but is £1.05 a year later, then annual milk inflation is 5%.

How is the UK’s inflation rate measured?

The prices of hundreds of everyday items, including food and fuel, are tracked by the Office for National Statistics (ONS).

This virtual “basket of goods” is regularly updated to reflect shopping trends, with virtual reality headsets and yoga mats added in 2025, and local newspaper adverts removed.

The ONS monitors price changes over the previous 12 months to calculate inflation.

The main inflation measure is called the Consumer Prices Index (CPI), and the latest figure is published every month.

CPI was 3.8% in the year to July 2025, up from 3.6% in the 12 months to June. The July 2025 figure is the highest recorded since January 2024, when the rate was 4.0%.

The Bank also considers other measures such as “core inflation” when deciding whether and how to change rates.

This doesn’t include food or energy prices because they tend to be very volatile, so can be a better indication of longer term trends.

Core CPI was 3.8% in the 12 months to July, up slightly from 3.7% recorded in the year to June.

Why are prices still rising?

Inflation has fallen significantly since hitting 11.1% in October 2022, which was the highest rate for 40 years.

But that doesn’t mean prices are falling – just that they are rising less quickly.

Inflation soared in 2022 because oil and gas were in greater demand after the Covid pandemic, and energy prices surged again when Russia invaded Ukraine.

It then remained well above the 2% target partly because of higher food prices.

These continue to be a significant factor in the current inflation figures.

Inflation for food and non-alcoholic beverages was 4.9% in the year to July, up from 4.5% in the year to June.

Beef, sugar, chocolate, instant coffee and fruit juice saw significant price rises.

But the main factor driving the July inflation figure was higher air fares, which saw the largest July increase since the ONS began collecting that data on a monthly basis in 2001.

In addition, fuel prices fell only slightly between May and June 2025, compared to a larger drop in the same period in 2024.

Why does putting up interest rates help to lower inflation?

When inflation was well above its 2% target, the Bank of England increased interest rates to 5.25%, a 16-year high.

The idea is that if you make borrowing more expensive, people have less money to spend. People may also be encouraged to save more.

In turn, this reduces demand for goods and slows price rises.

But it is a balancing act – increasing borrowing costs risks harming the economy.

For example, homeowners face higher mortgage repayments, which can outweigh better savings deals.

Businesses also borrow less, making them less likely to create jobs. Some may cut staff and reduce investment.

In recent months inflation has remained above the Bank’s target at the same time as the economy has remained relatively flat and the jobs market has softened.

Therefore, the Bank has chosen to cut rates, despite high inflation, in an attempt to encourage people to spend more and get businesses to invest and create jobs to boost the economy.

What is happening to UK interest rates and when will they go down again?

The Bank of England began cutting rates in August 2024, and made five cuts to bring the rate down to 4%.

Bank of England governor Andrew Bailey had said that future cuts will be made gradually and carefully.

The August interest rate decision was extremely close, with the committee voting 5-4 to cut rates by a quarter percentage point.

It followed an unprecedented second vote by the Bank’s policymakers, as one economist wanted a larger cut of half a percentage point.

This suggests future interest rate decisions could also be finely balanced.

Inflation is now expected to peak at 4% in September, the Bank said in its latest Monetary Policy Report. That is twice the Bank’s target rate and above the 3.8% high it predicted in its previous report in May.

A further interest rate cut had been expected at the Bank’s meeting in November, but analysts are now less sure this will happen given the closeness of the August vote.

The Bank also has to consider the wider global economy. Mr Bailey has repeatedly warned about the unpredictable impact of US tariffs, and conflict in Israel and Iran has also created uncertainty.

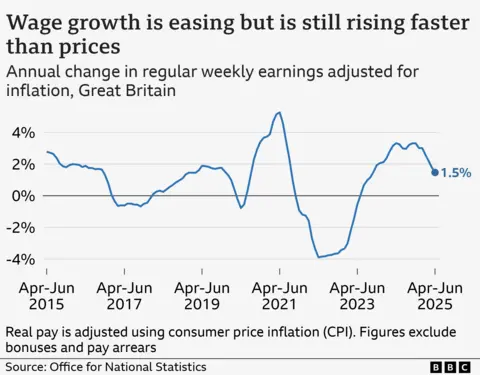

Are wages keeping up with inflation?

Annual average regular earnings growth was 5.7% for the public sector and 4.8% for the private sector.

Meanwhile, separate ONS figures showed the number of vacancies fell again to 718,000 for the May to July period, marking three continuous years of falling job openings.

The unemployment rate was 4.7% in the three months to July – the same as the three months to April.

This marked the highest level of unemployment since June 2021, and is also likely to factor into the Bank of England’s decision whether to cut rates again.

What is happening to inflation and interest rates in Europe and the US?

The US and EU countries have also been trying to limit price increases.

The inflation rate for countries using the euro was 2.1% in August, according to an early estimate.

In June 2024, the European Central Bank (ECB) cut its main interest rate from an all-time high of 4% to 3.75%, the first fall in five years.

By July 2025, after several further cuts, its key rate stood at 2%.

Inflation in the US held steady at 2.7% in July, remaining above the US central bank’s 2% target.

After a string of cuts in the latter part of 2024, the US central bank again chose not to change rates at its July 2025 meeting, the fifth hold in a row.

That leaves its key interest rate unchanged in a range of 4.25% to 4.5%.

The Federal Reserve has repeatedly come under attack from President Trump, who wants to see further interest rate cuts.

Business

Petrol and diesel prices may rise if Middle East crisis persists, says RBI Governor Sanjay Malhotra – The Times of India

Reserve Bank Governor Sanjay Malhotra has said the government may eventually have to raise petrol and diesel prices if the ongoing Middle East crisis continues for a prolonged period, PTI reported on Wednesday.Speaking at a conference in Switzerland on Tuesday, Malhotra said the disruption in oil and gas supplies due to the conflict and blockade of the Strait of Hormuz has begun impacting India, which remains heavily dependent on energy and fertiliser imports.Referring to the crisis, the RBI governor said if it continues for a longer duration, it is a “matter of time that the government will actually pass on some of these price increases”.The government has so far not increased retail petrol and diesel prices despite the conflict in West Asia that began on February 28.Malhotra also said the government has remained fiscally prudent and continues on the path of fiscal consolidation.The comments come amid rising pressure on India’s external sector due to elevated crude oil prices and a weakening rupee, which has slipped below the 95 mark against the US dollar.Prime Minister Narendra Modi had earlier called for measures such as reducing fuel consumption and lowering edible oil usage to help conserve foreign exchange reserves.As global crude oil prices surge amid the prolonged Middle East conflict and disruptions around the Strait of Hormuz, India has so far avoided major increases in petrol and diesel prices, choosing instead to absorb the pressure through state-run oil marketing companies (OMCs), tax adjustments and supply management measures.The Centre has repeatedly asserted that there is no fuel shortage in the country and no plan to introduce rationing of petrol, diesel or LPG despite disruptions in global energy shipments linked to the Iran conflict and the Strait of Hormuz crisis.“There is no need to panic. There are sufficient supplies. There is no rationing in place. It’s not going to happen,” Oil Secretary Neeraj Mittal said recently at the CII Annual Business Summit.Officials said India currently maintains around 60 days of fuel stocks and nearly 45 days of LPG inventories despite continuing volatility in global energy markets.

OMC losses mount as crude prices surge

The government’s decision to hold retail fuel prices steady despite rising international crude rates has increased pressure on state-run oil companies.According to official discussions reviewed during recent government briefings, OMCs are estimated to be losing between Rs 1,000 crore and Rs 1,200 crore every day because of elevated crude prices and unchanged pump rates.Under-recoveries are estimated to have approached nearly Rs 2 lakh crore during the first quarter of 2026.The current crisis intensified after shipping movement through the Strait of Hormuz — a key global oil transit route handling nearly one-fifth of global crude flows — came under severe disruption during the Iran conflict.Brent crude prices surged above $110 per barrel during the latest phase of the crisis, sharply increasing import costs for major oil-consuming countries like India. India imports nearly 90 per cent of its crude oil requirements, making the economy highly vulnerable to global energy price shocks.

Govt focuses on supply stability, inflation control

The Centre has simultaneously attempted to prevent inflationary shocks and avoid panic in domestic fuel markets.Officials said India has increased procurement from alternate suppliers and secured additional energy cargoes to maintain uninterrupted supplies.“We have procured from other sources. We have procured from other countries. We have increased procurement from existing countries and that has kept us going in terms of supply management in the short run,” Mittal said.The government has also absorbed part of the global price shock through excise duty adjustments on petrol and diesel. Officials estimate the revenue impact of fuel-related tax reductions at nearly Rs 1.6 lakh crore.Prime Minister Narendra Modi on Sunday (May 10) urged citizens to conserve fuel, reduce unnecessary imports and avoid wasteful consumption as rising oil prices increase pressure on India’s import bill and foreign exchange reserves. The Prime Minister also encouraged greater use of public transport, carpooling, electric vehicles and work-from-home arrangements wherever possible. The government has described these as precautionary steps rather than emergency restrictions.

Pressure likely to continue

Fuel prices remain among the most politically sensitive economic issues in India because increases in petrol and diesel rates directly affect transport costs, food prices and household budgets.While the Centre has so far avoided large retail fuel price increases, analysts say prolonged suppression of prices could further strain OMC finances if crude prices remain elevated for a longer period.

Containers at the Port of Oakland in Oakland, California, US, on Thursday, March 26, 2026.

David Paul Morris | Bloomberg | Getty Images

Months after the Supreme Court ruled some tariffs were unconstitutional, the first round of tariff refunds has begun flowing in.

Oshkosh Corporation CFO Matt Field confirmed to CNBC that the company has started receiving tariff refunds as of Tuesday.

“Following acceptance of our initial filing, we have begun receiving payments on our tariff refund claims, representing an initial portion of our total claims submitted,” Field said.

The company has not yet verified its total refund amount, Field added.

Basic Fun, the company behind Care Bears and Tonka trucks, also told CNBC it began receiving tariff refunds on Tuesday.

CEO Jay Foreman said the refunds so far have only represented 5% of the company’s total claim on its early invoices.

“We will utilize the refund dollars to help support our 2026 cash flow and invest in our team. This is the toughest time of the year for toy companies,” Foreman said in a statement. “We’ll also be announcing to our staff that we will be increasing salaries to help offset cost of living increase, announcing promotions and larger merit increases. We are reinvesting the funds in our business and people.”

Logistics companies UPS, FedEx and DHL have previously said that they will file for tariff refunds on behalf of their customers, requiring no further action from them. The first phase of tariff refunds only covers requests for entries that CBP finalized within the past 80 days, though that process could take months to reach customers.

The U.S. Customs and Border Protection said in a court filing that it anticipated paying refunds of $35.46 billion on 8.3 million shipments, as of Monday morning.

In February, the Supreme Court invalidated President Donald Trump‘s tariffs imposed under the International Emergency Economic Powers Act of 1977. In the months that followed, companies began filing for tariff refunds in a portal, called the Consolidated Administration and Processing of Entries.

In a radio interview with WABC on Tuesday morning, Trump called the tariff refund situation “crazy.”

“In theory, you have to pay the tariffs back. We’ll fight that,” Trump said. “We were taking in fortunes from people that hate us, countries and companies that hate us.”

A cyber security expert says deleting chat history could lead to a lack of accountability if things go wrong.

Source link

What It Will Take to Make AI Sustainable

Israel’s Netanyahu held meeting in UAE with president during Iran war: PM office

Army officer among five soldiers martyred, 7 terrorists killed in Balochistan operation

-

Tech5 days ago

Tech5 days agoA new frontier: Identity stack evolves for agentic systems | Computer Weekly

-

Tech5 days ago

Tech5 days ago‘Orbs,’ ‘Saucers,’ and ‘Flashes’ on the Moon: Pentagon Drops New UFO Files

-

Tech5 days ago

Tech5 days agoNick Bostrom Has a Plan for Humanity’s ‘Big Retirement’

-

Fashion5 days ago

Fashion5 days agoNew orders in German manufacturing up 5% MoM in Mar 2026: Destatis

-

Business1 week ago

Business1 week agoIndia among most resilient large EMs, better placed for future global shocks; policy reforms & strong buffers help: Moody’s – The Times of India

-

Tech6 days ago

Tech6 days agoWhat Microsoft Executives Really Thought About OpenAI in 2018

-

Sports5 days ago

Sports5 days agoShaheen Afridi achieves landmark feat during opening Test against Bangladesh

-

Tech6 days ago

Tech6 days agoThe Canvas Hack Is a New Kind of Ransomware Debacle