Business

Covid inquiry hears impact on firms and staff

Ben King,

Simon Browning and

Archie Mitchell,Business reporters

Getty Images

Getty ImagesWorkers and business leaders have told the Covid-19 inquiry about the devastation they faced during the pandemic and the difficulties they faced accessing support.

Business owners described breaking into tears as they were forced either to lay off staff or shut up shop entirely, while employees told how they feared for their jobs.

The comments were included in 8,000 submissions from the public, and come as the third stage of the inquiry focuses on the measures taken to support workers’ incomes and keep businesses afloat when the pandemic struck.

According to the Treasury, £140bn was spent on support for businesses, much of it going to pay people’s wages when they were forced to stay at home.

The inquiry heard how, on his first day as chancellor in 2020, Rishi Sunak was presented with a briefing on the impact of the Covid outbreak on growth and financial stability.

Two months later, the Treasury concluded the economy was “in hibernation”, with the sharpest fall in output for nearly 100 years.

Sunak is one of the people who will appear before the inquiry, and Bank of England governor Andrew Bailey will also give evidence in the coming weeks.

Monday’s session opened with emotional video testimony from business owners and freelancers whose livelihoods were upended when Covid lockdowns started.

In the video, Lowri, an events freelancer, explained how she had become desperate as her income stopped and her freelance work vanished. She fought back tears as she explained she qualified for no support. She had a mortgage and a child at home, with “no savings” for back up.

Last week the report on the second phase of the inquiry, into political decision-making, found the government had done “too little, too late”.

The current module, expected to last until just before Christmas, will examine the unprecedented economic intervention rolled out when the first lockdown was announced in March 2020.

The largest scheme, the Coronavirus Job Retention Scheme, known as furlough, covered 11.7 million jobs between March 2020 and September 2021, at a cost of £70bn.

It paid a portion of employees’ wages to ensure they still had an income even if they could not go to work, and to keep businesses going so that they could reopen later.

There was also a support scheme for self-employed people, loan schemes for businesses and business rates relief.

Questions were raised over the scale of the financial support, the strength of safeguards against fraud and error, and whether it delayed people taking up new work roles.

In submissions to the inquiry, employees told the inquiry how they were worried of losing their jobs and faced a scramble to pay bills through the pandemic, with some missing out on furlough payments after being made redundant.

However, others said their careers were rescued by the furlough programme, while some business owners said they were saved by government support schemes and spared having to make redundancies.

As part of the submissions, the owner of a small retailer told the inquiry: “One awful day, I had to call 80% of my staff and tell them that we had to make them redundant because there was no job for them anymore.

“And I cried, I didn’t sleep all night, I was so, so, upset. I had people that had worked for me for seven, eight years, that I had to say, ‘I’m so sorry, I literally can’t afford to pay you anymore because we’ve got no business’.”

Describing flaws in the furlough system, one Northern Irish contributor said her husband lost his job in the run-up to the scheme coming to an end. “It then got extended, but he’d already been let go,” she said.

The Eat Out to Help Out scheme, which was introduced by Sunak, split opinion among bosses.

“When we reopened, it helped to get people back into the pub and it helped us increase our profits,” the finance director of a large English food and drinks firm said.

But an operations manager at a travel and hospitality firm in Wales said: “When we look back, it probably wasn’t the right thing to do, given where we were with the pandemic.”

The Covid Inquiry, chaired by Baroness Hallett, is expected to look at 10 areas in total, and provide lessons for managing future pandemics.

This phase of the inquiry will also look at the additional funding provided for public services such as the railways to keep them running during lockdowns, and support for the voluntary and community sector.

It will examine decisions on benefits, sick pay and support for vulnerable people.

Also appearing before the inquiry are:

- Former Treasury officials James Benford and Dan York-Smith

- Representatives of the charities Child Poverty Action Group, Long Covid Support and Disability UK

- Former Downing Street special adviser Ben Warner

- Former director general for analysis of the Covid-19 Taskforce, Robert Harrison.

Last week, Sunak told the BBC the government and scientific community were “operating in a highly uncertain environment”.

“I think we do need to view the decisions taken through that lens.

“But it’s important that lessons [are] learned so that we can be better prepared if there’s ever another pandemic.”

Business

Iran Conflict: Middle East tensions: Global insurers exit Iranian waters as conflict deepens – The Times of India

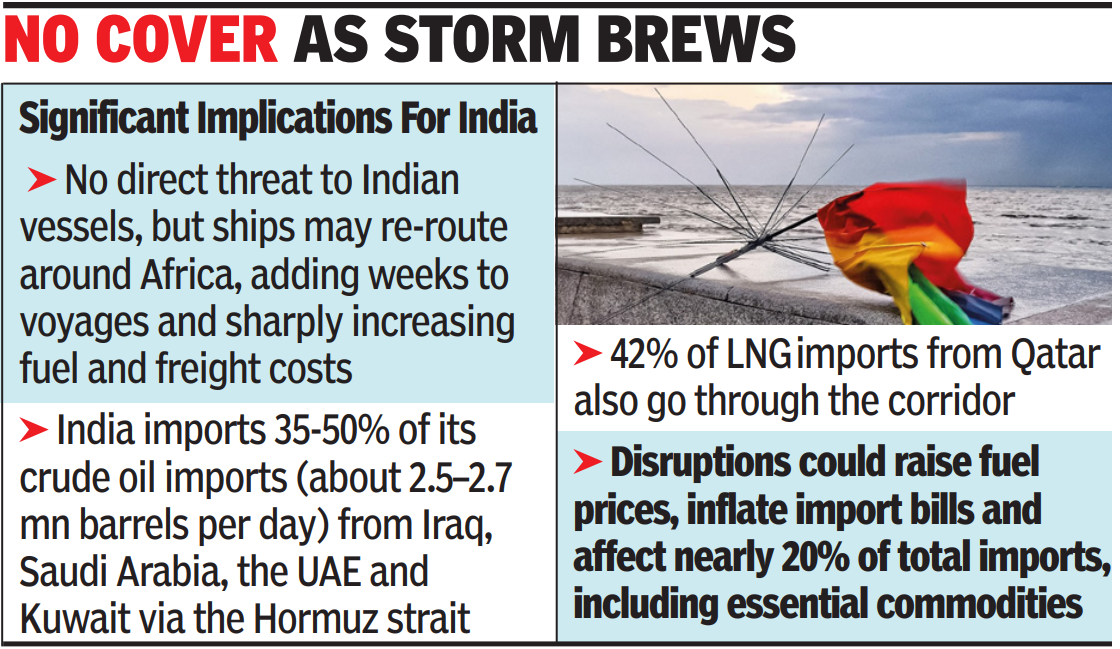

MUMBAI: India’s trade and energy supplies face fresh risks after reinsurers and Protection & Indemnity (P&I) clubs announced cancellation of war risk insurance for vessels transiting the Strait of Hormuz and Iranian waters, following an escalation in the Iran conflict. The cancellations, effective from this week, have left over 150 vessels stranded and disrupted a corridor that handles nearly one-fifth of global oil flows.P&I clubs are mutual, non-profit insurance associations owned by shipowners. They provide third-party liability cover through a pooled premium for risks such as cargo damage, pollution, crew injuries and collisions that are not covered under hull insurance. The clubs also provide legal support and dispute resolution across jurisdictions.“The industry is currently in a wait-and-watch mode, as much depends on how long the conflict persists. If it turns prolonged, insurers are likely to come together to create additional capacity for war-risk cover. Typically, there is an immediate surge in demand when hostilities break out, but that demand tends to ease quickly if the situation stabilises in a short span,” said Tapan Singhel, MD & CEO, Bajaj General Insurance.

Brokers said that in the past when international reinsurers ceased to provide cover for some risks like terrorism the Indian market had provided the capacity by building an insurance pool where domestic companies come together and share the risks. However, this tie state-owned reinsurer GIC Re, which leads domestic marine pools, has itself issued cancellation notices for marine hull war risk covers effective March 3, 2026, mirroring global reinsurers and P&I clubs. The crisis has brought marine insurance centerstage, the share of this line of non-life had shrunk to around 2% of industry premium as risks ebbed due to containarisation and more safety in transport. The size of the premium also determines the capacity of the industry to provide large covers.Their role is central to global shipping. Without P&I cover, shipowners face potentially unlimited liabilities in the event of accidents, pollution or war-related damage. In high-risk zones, the absence of insurance effectively halts voyages, as operators are unwilling to expose vessels to uninsured losses. In previous crises in the Red Sea, war risk exclusions by insurers sharply curtailed traffic and drove up freight rates.In the current episode, major P&I clubs and reinsurers have issued notices cancelling war risk cover for Iranian waters, the Persian Gulf and the Strait of Hormuz, citing tanker damage, casualties and threats from Iranian forces. Reports of VHF warnings and GPS disruptions have added to concerns. Insurers have invoked standard cancellation clauses following US and Israeli strikes on Iran, with broader policy implications if the conflict further widens.Fresh war risk cover may be available, but at sharply higher premiums. Rates that were around 0.25% of vessel value have surged multiple times, rendering transits commercially unviable for many operators. Even where cover is available, shipowners remain wary of risks such as seizures or missile strikes.

The UK economy could face a “very significant” hit from the conflict in Iran, the official budget watchdog has warned.

The Office for Budget Responsibility (OBR) said that the outlook for inflation would be “particularly uncertain” following spikes in gas and oil prices in recent days following attacks in the Middle East.

It came as the budget watchdog reduced its inflation forecast for this year, indicating that UK inflation will drop to target levels quicker than previously expected.

The OBR also cut its economic growth forecast for this year and revealed a worsening unemployment outlook for the next three years.

In its latest projections alongside the Chancellor’s spring statement, the organisation however highlighted that recent volatility in the Middle East could have an impact on a number of its projections.

The forecasts were prepared before days of recent attacks as part of an intensifying conflict between US-Israeli forces and Iran.

On Tuesday, the OBR said: “Conflict in the Middle East, which escalated as we were finalising this document, could have very significant impacts on the global and UK economies.”

David Miles, from the OBR’s budget responsibility committee, said its predictions that inflation will fall to target levels early this year have become more uncertain after jumps in oil and gas prices linked to recent attacks in the Middle East.

He said: “I think what will happen to inflation is particularly uncertain in the past few days.

“Our central expectation had been that inflation would fall back towards the Bank of England’s 2% target early this year and will be around that level at the end of the year.

“There must be more uncertainty around that right now.”

The trimmed-down inflation projections indicated that this will slow to 2.3% for 2026, down from a previous 2.5% forecast.

Experts said the lower-than-expected rate is partly down to “greater slack in the economy” and falling food and energy prices.

As a result, the OBR indicated that inflation will drop to the 2% target rate set by the Bank of England and the Government later this year.

The Bank has already suggested that inflation – the rate at which the price of goods and services rises – could fall below 2% by April.

The OBR said inflation is expected to remain at the 2% target from 2027 onwards, assuming this is not knocked off course by the potential jump in energy costs.

It came as the Chancellor Rachel Reeves told MPs in Parliament that the OBR said the UK economy would grow more slowly than previously expected in 2026, although growth will pick up in the following years.

UK gross domestic product (GDP) is expected to grow by 1.1% in 2026, as the OBR cut its previous prediction of 1.4% from last November.

The budget watchdog said the downgrade was linked to a growth slowdown late last year, loosening in the labour market and subdued data from recent business surveys.

However, it also lifted its forecasts for growth for both 2027 and 2028, with the economy to expand by 1.6% in both years.

The Chancellor said she had the “right economic plan” for the UK as she laid out her spring statement on Tuesday.

Ms Reeves also said that unemployment is “set to peak later this year” before reducing over the following years.

The OBR said that the UK unemployment rate is on track to peak at about 5.33% in 2026.

Latest data from the Office for National Statistics (ONS) showed that unemployment lifted to a five-year-high of 5.2% in the three months to December.

The OBR had previously predicted that the jobless rate would increase to 4.9% in 2026.

New forecasts show that unemployment is then on track to hit 4.9% in 2027 and 4.4% in 2028.

It had previously forecast it would be 4.6% in 2027 and 4.3% the following year.

The new forecasts have also reduced the Government’s borrowing projections for each year until 2031, in a potential boost for the Chancellor.

Reduced borrowing costs, linked to an easing in the yield on Government bonds, also meant that the Government’s headroom to meet its fiscal rules widened to £23.6 billion, compared with £21.7 billion in November’s budget.

Elliott Jordan-Doak, senior UK economist at Pantheon Macroeconomics, said: “There were few major surprises in today’s spring statement, with the Chancellor delivering the well-flagged ‘boring budget’ that we and the market were expecting.”

He added: “Chunks of the fiscal forecasts now look dated because of the rapid escalation of events in the Middle East.”

Peter Arnold, EY UK chief economist, said: “The underlying improvement in the UK’s fiscal position was supported by higher actual and expected tax receipts, driven in large part by a stronger equity market performance since November.

“There may now be doubts around how long this stock market performance can be sustained if the conflict in the Middle East is prolonged and global equity market volatility continues.”

Business

IMF says ‘too early’ to gauge West Asia conflict impact as energy prices, markets turn volatile – The Times of India

With tensions escalating in West Asia, the International Monetary Fund on Tuesday said it is closely tracking the situation but cautioned that it is “too early to assess the economic impact on the region and the global economy,” as disruptions to trade and energy markets intensify.In a statement, the IMF said it has “observed disruptions to trade and economic activity, surges in energy prices, and volatility in financial markets.”“The situation remains highly fluid and adds to an already uncertain global economic environment,” it said, reported ANI.“It is too early to assess the economic impact on the region and the global economy. That impact will depend on the extent and duration of the conflict,” the IMF added.The remarks come as governments evaluate the fallout of the widening hostilities in the region, particularly on oil supplies and global financial stability.In India, Petroleum and Natural Gas Minister Hardeep Singh Puri earlier said the country is “fully prepared amid evolving situation in the Middle East and energy supplies are robust.”He stated that “the country is well stocked with crude oil and inventories of key petroleum products including petrol, diesel and ATF to deal with short-term disruptions arising from the Middle East.”According to the minister, Indian energy companies have access to supplies that are not routed through the Strait of Hormuz, and such cargoes will remain available to mitigate any temporary disruptions affecting shipments passing through the strait.The Petroleum ministry has also set up a 24×7 Control Room to continuously monitor supply and stock positions of petroleum products across the country.The government is “reasonably comfortable in terms of stocks,” the minister said, adding that safeguarding the interests of Indian consumers remains the highest priority. Based on continuous monitoring, the government is cautiously optimistic that phased measures can be taken, if required, to further mitigate the situation.Government sources said India currently holds about eight weeks of crude oil and petroleum product inventories, including strategic reserves. They added that only about 40 per cent of India’s crude oil imports transit through the Strait of Hormuz, limiting exposure to regional disruptions.Sources maintained that the country remains in a comfortable position on energy security and is closely monitoring developments, while being prepared to manage potential supply-side challenges through adequate inventory levels and diversified sourcing.

Demi Lovato, Keke Palmer question relationship with older men

Iran Conflict: Middle East tensions: Global insurers exit Iranian waters as conflict deepens – The Times of India

Barcelona gets bigger spending cap, opens door on new signings

-

Politics6 days ago

Politics6 days agoWhat are Iran’s ballistic missile capabilities?

-

Politics6 days ago

Politics6 days agoUS arrests ex-Air Force pilot for ‘training’ Chinese military

-

Business7 days ago

Business7 days agoHouseholds set for lower energy bills amid price cap shake-up

-

Sports1 week ago

Sports1 week agoTop 50 USMNT players of 2026, ranked by club form: USMNT Player Performance Index returns

-

Sports6 days ago

Sports6 days agoSri Lanka’s Shanaka says constant criticism has affected players’ mental health

-

Business7 days ago

Business7 days agoLucid widely misses earnings expectations, forecasts continued EV growth in 2026

-

Fashion5 days ago

Fashion5 days agoPolicy easing drives Argentina’s garment import surge in 2025

-

Fashion5 days ago

Fashion5 days agoTexwin Spinning showcasing premium cotton yarn range at VIATT 2026