Business

Global Conflicts Drive Arms Industry to $679 Billion Record Revenues – SUCH TV

Sales by the world’s top 100 arms makers reached a record $679 billion last year, as conflicts in Ukraine and Gaza fueled demand, according to researchers. Production challenges, however, continued to hamper timely deliveries.

The figure represents a 5.9 percent increase from the previous year, and over the 2015–2024 period, revenues for the top 100 arms makers have grown by 26 percent, according to a report by the Stockholm International Peace Research Institute (SIPRI).

“Last year, global arms revenues reached the highest level ever recorded by SIPRI, as producers capitalized on strong demand,” said Lorenzo Scarazzato, a researcher with the SIPRI Military Expenditure and Arms Production Programme.

Regional Trends

According to SIPRI researcher Jade Guiberteau Ricard, the growth is mostly driven by Europe, though all regions saw increases except Asia and Oceania.

The surge in Europe is linked to the war in Ukraine and heightened security concerns regarding Russia.

Countries supporting Ukraine and replenishing their stockpiles have also contributed to rising demand.

Ricard added that many European nations are now seeking to modernize and expand their militaries, creating a new source of demand.

US and European Arms Makers

The United States hosts 39 of the world’s top 100 arms makers, including the top three: Lockheed Martin, RTX (formerly Raytheon Technologies), and Northrop Grumman. US companies saw combined revenues rise 3.8 percent to $334 billion, nearly half of the global total.

European arms makers (26 companies in the top 100) recorded aggregate revenues of $151 billion, a 13 percent increase.

The Czech company Czechoslovak Group recorded the sharpest rise, with revenues jumping 193 percent to $3.6 billion, benefiting from the Czech Ammunition Initiative, which supplies artillery shells to Ukraine.

However, European producers face challenges in meeting increased demand, as sourcing raw materials has become more difficult.

Companies like Airbus and France’s Safran previously sourced half of their titanium from Russia before 2022 and have had to identify new suppliers.

Additionally, Chinese export restrictions on critical minerals have forced firms such as France’s Thales and Germany’s Rheinmetall to restructure supply chains, raising costs.

Russian Arms Industry

Two Russian arms makers, Rostec and United Shipbuilding Corporation, are among the top 100, with combined revenues rising 23 percent to $31.2 billion, despite component shortages caused by international sanctions.

Domestic demand largely offset the decline in exports. However, Russia’s arms industry faces a shortage of skilled labor, limiting its ability to sustain production rates necessary for ongoing military operations.

Israeli weapons still popular

The Asia and Oceania region was the only region to see the overall revenues of the 23 companies based there go down — their combined revenues dropped 1.2 percent to $130 billion.

But the authors stressed that the picture across Asia was varied and the overall drop was the result of by a larger drop among Chinese arms makers.

“A host of corruption allegations in Chinese arms procurement led to major arms contracts being postponed or cancelled in 2024,” Nan Tian, Director of SIPRI’s Military Expenditure and Arms Production Programme, said in a statement.

Tian added that the drop deepened “uncertainty” around China’s efforts to modernise its military.

In contrast, Japanese and South Korean weapons makers saw their revenues increase, also driven by European demand.

Meanwhile, nine of the top 100 arms companies were based in the Middle East, with combined revenues of $31 billion.

The three Israeli arms companies in the ranking accounted for more than half of that, as their combined revenues grew by 16 percent to $16.2 billion.

SIPRI researcher Zubaida Karim noted in a statement that “the growing backlash over Israel’s actions in Gaza seems to have had little impact on interest in Israeli weapons”.

Business

Life sciences lab real estate is clawing back from disaster. Here’s what that means for investors

Business

Trump administration in advanced talks for a rescue package for Spirit Airlines, source says

A Spirit commercial airliner prepares to land at San Diego International Airport in San Diego, California, U.S., January 18, 2024.

Mike Blake | Reuters

The Trump administration is in advanced talks for a financing package for Spirit Airlines as the carrier is facing the risk of a liquidation, according to a person familiar with the matter.

Spirit had been facing a potentially imminent liquidation, people familiar with the matter told CNBC last week, speaking on the condition of anonymity to discuss matters that had not yet been made public. The Dania Beach, Florida-based carrier in August filed for its second Chapter 11 bankruptcy in less than a year, after it struggled to increase revenue to cover rising costs.

President Donald Trump hinted at potential government aid on Tuesday, telling CNBC’s “Squawk Box“, “Spirit’s in trouble, and I’d love somebody to buy Spirit. It’s 14,000 jobs, and maybe the federal government should help that one out.”

The White House didn’t immediately comment.

“We are hopeful that the government will recognize the needs for emergency funds especially in the current economic environment,” a spokesperson for the Associated of Flight Attendants-CWA, which represents Spirit’s cabin crews, said in a statement. “The last thing our economy needs is tens of thousands more people out of work and the last thing the travelling public needs is fewer choices in air travel.”

The terms of the financing deal weren’t immediately known. The Wall Street Journal earlier reported that the talks were in an advanced stage.

The U.S. airline industry accepted more than $50 billion in taxpayer aid to weather the Covid-19 pandemic, which is still its biggest-ever crisis, but those funds weren’t handed to one specific airline. Some of the aid gave the U.S. government stock warrants for airlines.

Airlines also received a government bailout following the Sept. 11, 2001, terrorist attacks, but that money was also for more than one company. The U.S. in 2008-2009 also bailed out the auto industry during the financial crisis and took stakes in manufacturers.

The Trump administration has taken equity stakes in some companies it deemed critical to national security like Intel and USA RareEarth, though Spirit stands out as it is in bankruptcy.

In February, Spirit said it expected to exit bankruptcy in late spring or early summer, telling a U.S. court that it would shrink and focus its planes on high-demand routes and travel periods. Pilot and flight attendant unions had also made concessions, including going on furlough in recent months, in a bid to help Spirit survive.

But jet fuel prices have nearly doubled in some parts of the U.S. since then, further adding to challenges for Spirit and the rest of the airline industry.

As a low-fare airline that also faces competition from larger carriers with their own no-frills, basic economy offerings, it has grown harder for Spirit to cover expenses. Spirit had introduced extra-legroom seats and other premium options to try to cater to higher-spending customers.

Business

Iran war: Trump sanctions waiver or not – why India continues to buy Russian oil – The Times of India

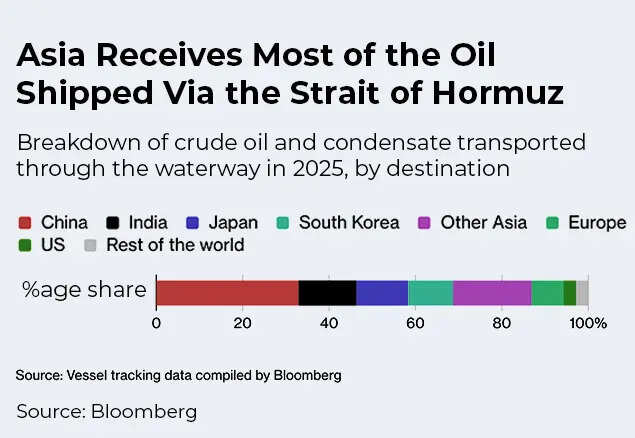

In early March, India was staring at a possible crude oil supply problem – the US-Iran war caused the Strait of Hormuz through which 20% of global crude transits to be effectively closed. To rescue came Russian crude oil! In fact, Russian crude has become a crucial support for India’s oil imports both in April and March. The import volumes are actually touching highs seen when India was bagging Russian crude at a huge discount.US President Donald Trump sanctioned two Russian oil majors towards the end of last year. This made it financially unviable for Indian refiners to continue to buy Russian crude at the same level as before, though flows of unsanctioned oil continued.However, in March, with the US sanctions waiver in effect, India has aggressively procured Russian crude, picking up millions of barrels. After the Russia-Ukraine war, Russian crude has maintained its position as the largest supplier of crude oil to India. Through Western sanctions, US President Donald Trump’s pressure and sanctions on Russian oil majors, crude from Russia has continued to flow to India, though the levels have varied.

However, experts believe that once the situation in the Middle East normalizes, India will go back to buying crude from Gulf countries, and Russia’s percentage in India’s oil imports will come down.

US sanctions waiver & India’s aggressive buying

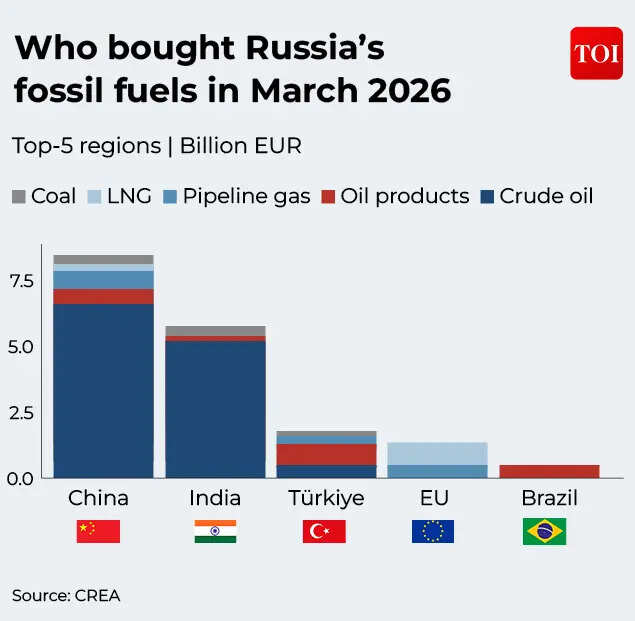

India has never officially said that it will stop buying Russian crude, and even when levels dropped after sanctions, Russia was still the biggest contributor. However, the Donald Trump administration’s decision to waive sanctions on Russian crude, and extend that waiver to May has allowed Indian refiners to step up procurement without any worries.According to the latest report from Centre for Research on Energy and Clean Air (CREA)’s analysis, while India’s total crude imports recorded a 4% reduction in March, Russian imports doubled.

“The biggest shift was in state-owned refineries’ imports from Russia, which saw a massive 148% month-on-month increase. Their imports were in fact 72% higher than March 2025, presumably due to Russian barrels being more available in the spot market, which serves as the primary source of imports for them,” says CREA.Russia’s share of India’s crude oil imports in March 2026 placed the month at the upper end of historical highs, closely mirroring peak levels seen in 2023, when Western sanctions redirected Russian oil flows toward Asia and made Moscow India’s single largest supplier.Sourav Mitra, Partner – Oil and Gas, Grant Thornton Bharat explains the emergence of Russia as a dominant supplier of crude for India.Russia’s share surged sharply in the months following the Ukraine war, peaking during several months in mid‑2023, particularly around May–June, when imports rose to about 1.9-2.0 million barrels per day and accounted for nearly 42-45% of India’s crude basket, displacing Iraq and Saudi Arabia. That dominance persisted through much of 2023, with average shares close to 40% between April and September, before easing in 2024 and early 2025 as price discounts narrowed, compliance costs increased and refiners partially rebalanced toward Middle Eastern grades.“Against this backdrop, the rebound seen in March 2026 effectively matches the 2023 peak, although the underlying drivers differed, with the latest spike largely reflecting supply disruptions in West Asia that curtailed Gulf inflows and compelled refiners to rely more heavily on available Russian cargoes. We expect that while March marks a return to near‑record dependence on Russian crude, such elevated levels are unlikely to persist once Middle Eastern supply chains stabilize,” Mitra tells TOI.

No more discounts! India paying a premium for Russian crude

What stands out is the fact that when India stepped up its procurement of Russian crude after the Ukraine war began, the oil was available at very steep discounts. This was due to European sanctions that made Russian crude available at a much lower rate than Brent. Come 2026, with oil supplies via Hormuz disrupted and global crude oil prices rising, Russia is now selling at a premium!According to Sourav Mitra of Grant Thornton Bharat, Indian refiners are currently paying a premium of about $4-6 per barrel over the Brent benchmark for Russian crude. These are some of the highest delivered premiums on Russian crude since Russia began diverting large volumes of crude to Asia after the Ukraine war, he tells TOI. “This shift is attributed to intense competition for prompt Russian cargoes as disruptions to Middle Eastern supply routes pushed refiners to prioritise assured deliveries over price. The premium contrasts starkly with February 2026, when Indian buyers were still securing Russian crude at discounts of roughly $12–$15 per barrel, shortly before conditions deteriorated in the Strait of Hormuz,” he elaborates.In fact, the turnaround is even more pronounced compared with 2022-23, when Russian crude frequently traded $20-$30 below Brent. The price inversion was reinforced by the US sanctions waiver issued in early March 2026 and effectively released millions of barrels into the market, strengthening sellers’ leverage. “As a result, India has shifted from discount‑driven buying to security‑led procurement, paying a premium to ensure supply continuity while Gulf flows remain disrupted,” he adds.

Why India continues to buy Russian crude

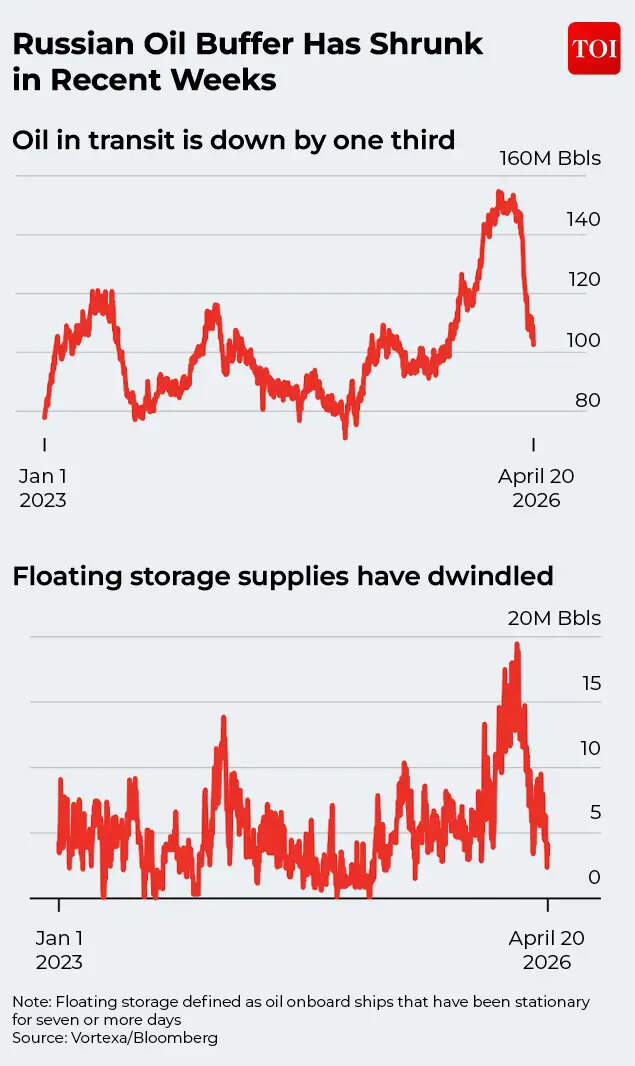

Russian oil is not going out of India’s crude imports anytime soon, experts say.However, Ivan Mathews, Head of APAC Analysis at Vortexa expects Russian crude imports to decline month-on-month in April. “Discounts on Russian crude were less competitive due to increased demand during the sanctions waiver period, which has since been extended to 16 May. This will lead to lower marginal imports for economics-driven refineries in India. Additionally, reduced crude loadings from Russia will decrease the availability of Russian barrels for imports in the coming weeks,” Mathews tells TOI.

Mitra of Grant Thornton Bharat says that Russian crude is now well integrated into India’s refining system and serves as a reliable fallback when alternative supplies tighten. Russia is likely to remain an important supplier through 2026 even as its share moderates from March’s highs and Middle Eastern flows stabilize.Sumit Ritolia, Manager Modelling and Refining at Kpler believes that Russian oil will continue to be a major part of India’s crude oil imports in the coming months as well. Currently, India’s Russian crude imports are tracking at around 1.6mbd, which is approximately 375 kbd lower than March levels.However, as Ritolia points out, this dip needs context as Nayara (≈400 kbd, fully reliant on Russian crude) has been under maintenance since the second week of April. Adjusting for this, the underlying demand signal for Russian barrels remains intact.“The flows are expected to range between 1.5-2 mbd with a slight dip possible due to ongoing infrastructure issues in Russia due to the conflict with Ukraine,” Ritolia tells TOI.Interestingly, Kpler data shows that even after US sanctions on Russian majors Lukoil and Rosneft came into effect late last year, Russia continued to be the largest supplier of crude oil to India. However, admittedly the volumes saw a sharp drop, with February levels being much lower. While the Donald Trump administration claimed finalising a trade deal contingent on India stopping crude imports from Russia, New Delhi has never said it will not buy oil from Moscow.The US first waived the sanctions in early March and then extended the waiver recently. Experts are of the view that even when the sanctions waiver lapses, Russian oil will continue to be imported, though the quantities may dip.“A key point that is often missed is that Russian oil itself is not sanctioned but certain entities, vessels, and financial channels are,” says Sumit Ritolia.According to Ritolia, Russia continues to be a core supplier for India, but in the absence of sanctions waiver procurement must strictly ensure:• No involvement of sanctioned sellers or intermediaries• Use of non-sanctioned vessels• Fully compliant financial, insurance, and trading channelsIndia is unlikely to move away from Russian crude in the near term. Instead, we should expect more documentation, tighter screening rather than a structural shift in sourcing as and when sanctions lapse, Ritolia added.

India’s Diversified Crude Supplies

But even as Russia is expected to continue being an important player in India’s crude imports, it is equally important to note that New Delhi has diversified its basket to include over 40 countries.As Sushil Mishra, Director, Crisil Intelligence points out: Historically, Russia’s share in India’s crude imports peaked at over 40%, however, it has varied in the last few years amid diversification efforts and evolving geopolitical dynamics. Improved refinery flexibilities have enabled Indian refiners to process a wider range of crude grades including those from the American, Russian, and Middle Eastern.“India continues to strengthen its energy resilience by diversifying crude sourcing and maintaining a pragmatic sourcing strategy driven by price, availability, and energy security considerations. This approach allows flexibility to adjust sourcing patterns in response to changing global market conditions and geopolitical developments,” he tells TOI.

Life sciences lab real estate is clawing back from disaster. Here’s what that means for investors

Men’s college basketball buzz: State of blue blood rebuilds

New York Bans Government Employees from Insider Trading on Prediction Markets

-

Fashion6 days ago

Fashion6 days agoFrance’s LVMH Q1 revenue falls 6%, shows resilience amid Iran war

-

Entertainment1 week ago

Entertainment1 week agoIs Claude down? Here’s why users are seeing errors

-

Sports1 week ago

Sports1 week agoPSL 11: Peshawar Zalmi win toss, opt to field first against Quetta Gladiators

-

Tech1 week ago

Tech1 week agoThe Deepfake Nudes Crisis in Schools Is Much Worse Than You Thought

-

Tech1 week ago

Tech1 week agoBremont Is Sending a Watch to the Moon’s Surface

-

Tech1 week ago

Tech1 week agoHuman-machine teaming dives underwater

-

Fashion1 week ago

Fashion1 week agoWhat no one is saying about the 2026 apparel slowdown

-

Business1 week ago

Business1 week agoBP sees ‘exceptional’ oil trading result as Iran war sends crude costs soaring