Business

Interest rates cut to 3.75% but further reductions to be ‘closer call’

Michael RaceBusiness reporter

Getty Images

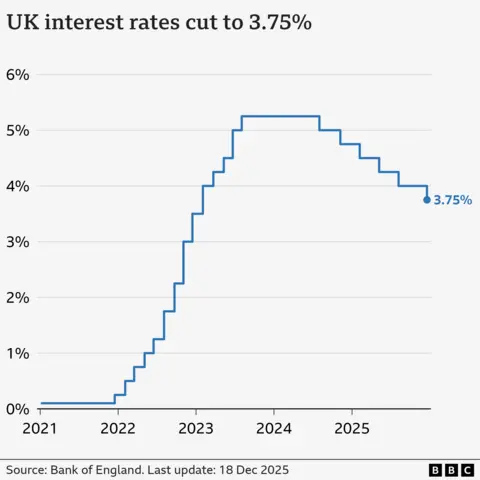

Getty ImagesInterest rates have been cut to 3.75%, the lowest level in almost three years, but further reductions are set to be a “closer call”, the Bank of England has said.

In a knife-edge vote, policymakers voted 5-4 in favour to lower rates from 4% reflecting concerns over rising unemployment and weak economic growth.

The Bank said rates were “likely to continue on a gradual downward path”, but warned judgements on further cuts next year would more contested.

Inflation is now expected to fall “closer to 2%” – the Bank’s target – next year, which is sooner than previous forecasts. However, the economy is predicted to see zero growth in the final few months of this year.

The decision to lower borrowing costs from 4% was widely expected, after figures this week showed inflation, the rate prices rise at, slowed further to 3.2% in the year to November.

“We still think rates are on a gradual path downward but with every cut we make, how much further we go becomes a closer call,” said the Bank’s governor, Andrew Bailey.

While the cut is likely to be good news for people looking to borrow cash or secure a mortgage, savers could see a reduction on their returns.

About 500,000 homeowners have a mortgage that “tracks” the Bank of England’s rate, and Thursday’s cut is likely to mean a typical reduction of £29 in monthly repayments.

Homeowners on standard variable rates are also likely to see lower payments, although the vast majority of mortgage customers have fixed-rate deals so are not affected by the latest decision.

The Bank said that, following the tax and spending policies announced in last month’s Budget and easing oil and gas prices, inflation was likely to fall close to 2% in the spring/summer of next year. Previously it did not expect this to happen until 2027.

Chancellor Rachel Reeves announced the government would cut £150 off household energy bills in the Budget, as well as freeze fuel duty and rail fares.

However, the Bank said weaker economic growth in November had led it to expect zero growth for the final few months of this year.

It said information gathered from businesses around the country suggested a “lacklustre economy”, with firms concerned by the speculation ahead of the Budget.

The Bank said consumers remained “cautious and keenly focused on value for money”, adding that food shops were “smaller than usual”.

“Some supermarkets have been concerned that the Budget will dampen spending on Christmas food and drink, but discounters say that early sales of lowered priced seasonal food are solid so far,” it added.

Latest figures showed the price of food was the main driver behind November’s drop in inflation.

The inflation rate has fallen in recent months, but this drop does not mean that prices are falling, rather they are rising at a slower rate.

Mr Bailey reiterated that the Bank believed inflation had passed its peak.

Reacting to the Bank’s decision, the chancellor said it was the “sixth interest rate cut since the election – that’s the fastest pace of cuts in 17 years, good news for families with mortgages and businesses with loans”.

But shadow chancellor Mel Stride said while lower interest rates would be “welcome news for many families”, the cut reflected “growing concerns about the weakness of our economy”.

“The economic mismanagement of Rachel Reeves has left the Bank of England with an impossible dilemma, balancing high inflation against a fragile economy.”

EPA

EPAThe Bank, which is independent of the government, sets interest rates in an attempt to try to keep consumer price rises under control.

The theory behind increasing interest rates to tackle inflation is that by making borrowing more expensive, more people will cut back on spending and that leads to demand for goods falling and price rises easing.

But it is a balancing act, as high interest rates can harm the economy as businesses hold off from investing in production and jobs.

The government has made growing the economy its main priority as part of its efforts to boost living standards.

In its most recent Monetary Policy Report, the Bank predicted UK economic growth would be 1.5% this year, but forecast it would fall to 1.2% next year before rising to 1.6% in 2027 and 1.8% in 2028.

Get our flagship newsletter with all the headlines you need to start the day. Sign up here.

Business

Stock market this week: Middle East tensions, oil prices, FII flows & more — what will guide Dalal Street

Dalal Street is heading into the new trading week with global uncertainty firmly in focus, as investors keep a close watch on the evolving situation in the Middle East, fluctuations in crude oil prices and the behaviour of foreign investors. Analysts said that sentiment is likely to remain fragile and heavily influenced by developments in negotiations between the United States and Iran, while movements in the rupee, global equities and the US dollar are also expected to shape market direction in the days ahead.Trading activity during the week is also expected to be shaped by the rupee’s movement against the US dollar, while investors continue to assess the impact of global uncertainty on risk appetite. Markets will remain closed on Thursday for Bakri Id.A key trigger for sentiment emerged over the weekend after US Secretary of State Marco Rubio said negotiations between Washington and Tehran had shown some progress, raising expectations that the ongoing conflict in West Asia could move closer to resolution.Ajit Mishra, SVP, Research at Religare Broking Ltd, said investors would closely track developments tied to crude oil, global currencies and bond markets. “This week is expected to remain highly sensitive to global macroeconomic developments and currency movements. Investors will also monitor crude oil prices, developments in US-Iran negotiations, and the trajectory of the US dollar and bond yields, all of which are expected to influence foreign flows and overall risk appetite,” he said.Apart from geopolitical developments, the Reserve Bank’s decision to transfer a record Rs 2.87 lakh crore dividend to the government for the year ended March 2026 is also expected to remain in focus. The announcement comes at a time when rising import costs and supply chain pressures linked to the West Asia conflict continue to weigh on the economy.According to Mishra, market participants are expected to evaluate how the RBI payout could affect liquidity conditions, fiscal flexibility and government spending in the months ahead.Ponmudi R, CEO of Enrich Money, said market behaviour in the coming sessions is expected to remain sensitive to fresh headlines surrounding diplomatic negotiations and oil prices. “Markets are expected to remain volatile and heavily headline-driven in the coming week, with investor attention firmly focused on developments surrounding the US–Iran situation, broader diplomatic negotiations and movements in crude oil prices,” he said.“While hopes of a diplomatic breakthrough and easing geopolitical tensions have improved sentiment modestly, investors continue to remain cautious as uncertainty surrounding the final outcome of the negotiations remains elevated,” Ponmudi added.He further said investors are expected to watch institutional flows, global equity trends, macroeconomic indicators and the rupee for further market cues. “With global uncertainty still elevated, market participants are likely to remain selective and cautious despite the recent improvement in sentiment,” he said.Vinod Nair, Head of Research at Geojit Investments Limited, said markets would require stronger support factors to build a more constructive setup. According to him, a meaningful decline in crude oil prices, steady foreign institutional investor flows and stable Q1FY27 earnings expectations without major downgrades would be important for sustained momentum.In the previous week, the BSE benchmark index rose 177.36 points, or 0.23%, while the NSE Nifty advanced 75.8 points, or 0.32%.

Reforms are needed of the welfare system to tackle the high numbers of young people not in work or education, says Alan Milburn.

Source link

Pets at Home investors will be hoping the retailer’s new boss can lay out a strategy to return it to profit growth despite a challenging consumer backdrop.

Shares in the company currently sit close to its lowest level for almost seven years following a recent downturn in the group’s retail arm.

The dip in the group’s performance contributed to the departure of previous chief executive Lyssa McGowan late last year.

In March, former Waitrose boss James Bailey took the reins in a bid to drive a turnaround in performance.

Shareholders will be hoping the new boss can show early signs of improvement and a long-term strategy to drive growth in Pets at Home’s update on Wednesday May 27.

The pet products retailer and vet chain is expected to report an underlying pre-tax profit of around £93 million for the year to March, according to analysts.

It would represent a roughly 30% fall from last year, after the company came under pressure from weak demand for discretionary products.

Analysts have said investors will be looking at early trading in the current financial year to see how consumer spending is holding up.

AJ Bell’s investment director Russ Mould said: “Pets at Home could badly do with some renewed pep.

“Under executive chair Ian Burke, who has returned to a non-executive role after leading the business on an interim basis, Pets at Home laid out a plan to fix a retail business which has been badly affected by a reduction in discretionary spend on toys and treats for Britons’ furry and feathered friends.

“The country may have a reputation for loving their animal companions but in an environment where households are having to watch their pennies, these nice-to-have items were off the list.”

The group has also seen sales of pet food and similar products face fierce pricing competition from non-specialist retailers, such as supermarkets.

It has since cut prices among around 1,000 products in order to help drive activity, with cash-strapped shoppers looking for value.

Data from the Office for National Statistics (ONS) showed that UK retail sales volumes dropped to an 11-month low in April, with a 1.3% fall for the month.

Pets at Home is predicted to report revenues of £1.47 billion for the past year, just marginally lower than £1.482 billion reported last year.

Lena Dunham reveals rare detail about first interaction with Luis Felber

WWE Hall of Famer Nikki Bella opens up about what she wants fans to remember her for when she retires

Taylor Swift’s next plans revealed as ‘Showgirl’ era nears end

-

Entertainment1 week ago

Entertainment1 week agoWhere Pete Davidson, Elsie Hewitt stand after breakup: Details revealed

-

Politics1 week ago

Politics1 week agoRising diesel costs from Iran war strain US school budgets

-

Tech1 week ago

Tech1 week agoWhy Is Your Grill So Dumb? The Best Grills Set Temp Like an Oven

-

Tech1 week ago

Tech1 week agoGreg Brockman Officially Takes Control of OpenAI’s Products in Latest Shakeup

-

Tech1 week ago

Tech1 week agoThis Solar-Powered Smart Sprinkler Keeps My Lawn Watered Without Any Power Cables

-

Fashion1 week ago

Fashion1 week agoRMG trade bodies seek policy support from Bangladesh PM

-

Tech1 week ago

Tech1 week agoTesla Reveals New Details About Robotaxi Crashes—and the Humans Involved

-

Fashion6 days ago

Fashion6 days agoNigeria Kwara Garment Factory, KWS Garment Production Village ink pact