Business

Multifamily housing leads CRE bid competition in October

Modern urban condos in Chattanooga, Tennessee

Marcia Straub | Moment | Getty Images

A version of this article first appeared in the CNBC Property Play newsletter with Diana Olick. Property Play covers new and evolving opportunities for the real estate investor, from individuals to venture capitalists, private equity funds, family offices, institutional investors and large public companies. Sign up to receive future editions, straight to your inbox.

July marked a turning point in competition for commercial real estate properties, with bids rising for the first time in more than a year. That trend continued into October.

Bidder dynamics during the month saw the second-highest monthly gain over the past year, according to JLL’s Global Bid Intensity Index. Competitiveness continues to improve, partly due to interest rate cuts by the U.S. Federal Reserve in September and October.

The index measures bidding activity in order to give a real-time view of liquidity and competitiveness in private real estate capital markets. That, in turn, is an indicator for future capital flows across investment sales transactions.

“As capital deployment accelerated during the third quarter, institutional investors are signaling increased confidence in the market, even as uncertainty persists,” said Richard Bloxam, CEO of capital markets at JLL. “We expect business confidence will continue to improve and pave the way for continued capital flow growth into 2026.”

Of all the commercial real estate sectors, multifamily housing led in competition with the strongest bidding activity. That is being driven by housing shortages across most major markets. Rental vacancy rates are still high, but more renters are expected to re-lease in the coming year because the for-sale housing market is so expensive.

JLL estimates that there is a shortage of 3.5 million housing units in the U.S. That, along with near-record-high home prices, is keeping renters in place for longer and will likely push multifamily vacancy rates lower once all the new supply makes it through the pipeline. All of that is driving continued strong conviction among multifamily investors.

There was also a significant rebound in bidding competitiveness for the industrial and logistics sector, as trade policy uncertainty settled slightly.

There was some softening in competition for retail properties simply because there were more of them for sale, so buyers had more choice. There were, however, more deals in the market. Investor demand is being driven by a rise in consumer and retail spending, for now at least.

The office sector is also well into recovery, with bid dynamics rising from all-time lows in late 2023. Investor sentiment is improving with expanding bidder pools and increased lender participation.

Near-term interest rate cuts are still in question, especially given stronger-than-expected employment figures for September, released late due to the government shutdown. Investors, however, seem to be less sensitive to the timing, as they still expect rates to come down further next year.

“While market uncertainty will continue to impact decision-making, the growth picture is looking more positive for 2026. Having worked through various junctures of uncertainty over the past year, more investors are showing a higher tolerance for risk,” Bloxam said. “Coupled with the exceptionally strong debt markets, we expect this will catalyze continued improvement in liquidity.”

The boss of insurer Aviva has cautioned that a lengthy conflict in the Middle East could send the cost of vehicle parts and repairs surging in an echo of the aftermath seen after Russia’s invasion of Ukraine.

Chief executive Amanda Blanc said the group has seen limited claims so far relating to the US-Israel war with Iran, but flagged the potential for claims costs to jump if supply chains are badly disrupted for a long time.

She said: “We have a good case study on this in terms of the Ukraine situation back in 2022 and the impact on the supply chain, which had an inflationary impact on vehicle parts and replacement vehicles.

“Obviously, if this goes on for a prolonged period of time, we would expect that this could have some impact, but to speak about this from an Aviva perspective, we are very well placed to manage that with our supply chain and our owned garage network.”

Ms Blanc added: “We will take action as necessary to make sure we look after our customers and price accordingly for any new inflationary impact.”

She said there had been “very limited” travel claims so far.

Ms Blanc added: “We have had calls from customers asking about whether they should travel and those sorts of things, and we are pointing them to the Foreign Office guidance on that.”

Full-year results from Aviva on Thursday showed annual earnings leaped 25% higher, while the firm also announced it was resuming share buybacks as it continues to benefit from its £3.7 billion takeover of Direct Line.

The group unveiled an earnings haul of £2.2 billion for 2025, up from £1.8 billion in 2024, including a £174 million contribution from Direct Line, helping the group hit its financial targets a year early.

Aviva unveiled a £350 million share buyback after putting these on hold due to the Direct Line deal, which completed last year.

Ms Blanc cheered an “outstanding performance”.

She said: “We have transformed Aviva over the last five years and whilst we have made significant progress, there is so much more to come.”

Artificial intelligence (AI) is also a big area of focus for the firm, according to Ms Blanc.

“We have clear strengths in artificial intelligence which are creating major opportunities to transform claims, underwriting and customer experience,” she said.

The firm was unable to cope during high demand, Ofwat says, leading to “immense stress” for customers.

Source link

Business

Middle East heat may ripple across India’s energy supply chain, flags Goldman Sachs – The Times of India

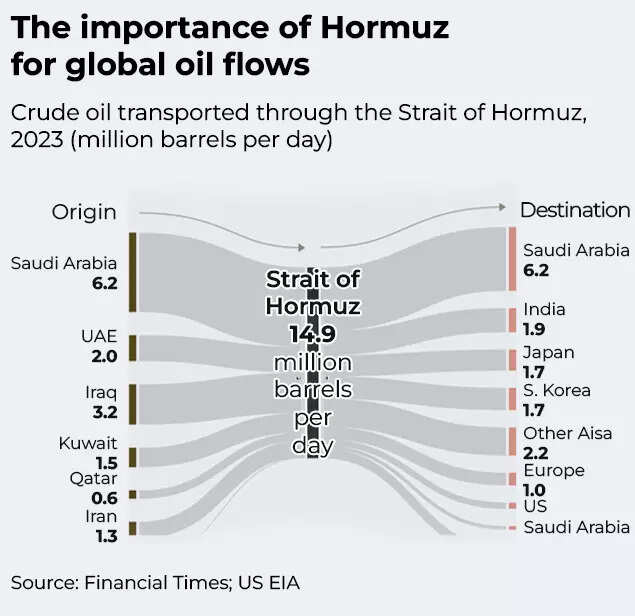

As tensions continue to heat up in the Middle East, concerns are raising about disruptions to one of the world’s most critical energy shipping routes, the Strait of Hormuz. Any disruption could significantly affect major oil-importing countries such as India, as the narrow Strait of Hormuz is central to global energy trade. The strait sees almost 20 million barrels of oil passing through each day, or about a fifth of the world’s consumption, pass through the route. The waterway also carries roughly 19% of global liquefied natural gas (LNG) shipments, making it a crucial corridor for energy-importing economies.A recent report by Goldman Sachs has flagged early signs of stress in the region. The report warned that tanker traffic through the Strait of Hormuz has already begun showing signs of disruption, with shipping firms, oil producers and insurers adopting a cautious approach following reports of damaged vessels in nearby waters.According to the firm, financial markets have already begun factoring in the geopolitical risk. Oil prices currently carry an estimated risk premium of $18-per-barrel, reflecting the potential market impact if energy flows through the Strait of Hormuz were disrupted for about a month.

Even is the oil facilities are not directly damaged, a shutdown of the shipping route could expose a significant portion of global supply. The report estimates that in an event of full closure, about 16 million barrels per day of oil flows could be affected, despite the availability of some pipeline routes designed to bypass the strait.And the risks are not limited to crude oil shipments with almost 80 million tonnes of LNG exports annually, much of it from Qatar, moving through the passage. Any prolonged disruption could tighten gas supply globally and potentially drive European benchmark gas prices back to levels seen during the 2022 energy crisis.

Asian economies stand among the most exposed to such disruptions. Major importers such as China, India, Japan and South Korea depend heavily on oil and LNG shipments that transit through the strategic corridor.While global oil inventories and spare production capacity could help cushion short-term shocks, the report warned that sustained disruption to Gulf shipping routes could trigger sharp volatility in global energy markets and push prices higher across oil, gas and refined fuel products.Market participants and governments are closely watching tanker traffic in the Strait of Hormuz, along with diplomatic and military developments involving the United States, Iran and Gulf nations, to assess whether the current disruptions remain temporary or escalate into a broader energy supply shock.

Aviva flags potential for Iran conflict to send claims costs rising

Queen Letizia shows presence and support during difficult day

Need One Pair for Hiking, Traveling, and Working Out? Try Gravel Running Shoes

India Us Trade Deal: Fresh look at India-US trade deal? May be ‘rebalanced’ if circumstances change, says Piyush Goyal – The Times of India

What are Iran’s ballistic missile capabilities?

Attock Cement’s acquisition approved | The Express Tribune

-

Politics1 week ago

Politics1 week agoWhat are Iran’s ballistic missile capabilities?

-

Business6 days ago

India Us Trade Deal: Fresh look at India-US trade deal? May be ‘rebalanced’ if circumstances change, says Piyush Goyal – The Times of India

-

Business7 days ago

Attock Cement’s acquisition approved | The Express Tribune

-

Business1 week ago

Business1 week agoHouseholds set for lower energy bills amid price cap shake-up

-

Politics1 week ago

Politics1 week agoUS arrests ex-Air Force pilot for ‘training’ Chinese military

-

Fashion7 days ago

Fashion7 days agoPolicy easing drives Argentina’s garment import surge in 2025

-

Sports6 days ago

Sports6 days agoLPGA legend shares her feelings about US women’s Olympic wins: ‘Gets me really emotional’

-

Fashion6 days ago

Fashion6 days agoTexwin Spinning showcasing premium cotton yarn range at VIATT 2026