Business

Reeves says Budget will be ‘fair’ as tax rises expected

Jennifer Meierhans,Business reporter and

Henry Zeffman,Chief political correspondent

PA Media

PA MediaChancellor Rachel Reeves has said she will make “necessary choices” in the Budget after the “world has thrown more challenges our way”.

Her Downing Street speech did not rule out a U-turn on Labour’s general election manifesto pledge not to hike income tax, VAT or National Insurance.

When journalists explicitly asked if the government was set to break that pledge she did not answer directly but said she was “setting the context for the Budget”.

Ahead of the speech, shadow chancellor Sir Mel Stride dubbed it an “emergency press conference”, adding “higher taxes are on the way” and called for Reeves to be sacked if she “breaks her promises yet again”.

If there was any doubt about tax rises before this speech, there isn’t now.

Yet Reeves repeatedly refused to get into the specifics of which taxes might go up.

Instead she began the work of explaining why a year after delivering a tax-raising Budget and vowing not to come back for more, she is in fact coming back for more.

The chancellor said she would do what is necessary, not what is popular.

The reasons she gave were poor productivity, for which she blamed Conservative government policy including Brexit, austerity and short-sighted decisions to cut infrastructure spending, persistently high global inflation and the uncertainty unleashed by Donald Trump’s tariffs.

In short, Reeves’ argument is that the failings of others are being visited upon this government, and that it falls to her to confront decisions her predecessors ducked.

She pledged to come up with a “Budget for growth with fairness at its heart” aimed at bringing down NHS waiting lists, the national debt and the cost of living.

“It is important that people understand the circumstances we are facing, the principles guiding my choices – and why I believe they will be the right choices for the country,” she said.

There are some in government who want this to be a one-and-done Budget, in that they do not want to come back again and again every year, eking out a bit more money in tax to meet the requirements of the independent forecast.

That is seen as an argument for raising billions of pounds through increasing at least one of the income tax rates.

However, no chancellor has increased the basic rate in 50 years and it would be a big risk politically, especially with public trust in politics in general, and Prime Minister Sir Keir Starmer in particular, so low.

There is also the question of whether the prime minister and chancellor could land the argument that none of this was foreseeable before last year’s Budget.

The message from Reeves echoed comments made by Sir Keir to a group of Labour MPs on Monday night.

He told those gathered that the Budget would be “a Labour Budget built on Labour values” and that the government would “make the tough but fair decisions to renew our country and build it for the long term”.

It comes as the Resolution Foundation, which has close links to Labour and was previously run by Treasury minister Torsten Bell, said avoiding changes to VAT, NI or income tax “would do more harm than good”.

Hiking income tax would be the “best option” for raising cash, it said, but suggested it should be offset by a 2p cut to employee national insurance, which would “raise £6 billion overall while protecting most workers from this tax rise”.

Extending the freeze in personal tax thresholds for two more years beyond April 2028 would also raise £7.5 billion, its pre-Budget analysis suggested.

The government’s official forecaster, the Office for Budget Responsibility (OBR), is widely expected to downgrade its productivity forecasts for the UK at the end of the month. That could add as much as £20bn to the amount the chancellor will need to find if she is to meet her self-imposed “non-negotiable” rules for government finances.

The two main rules are:

- Not to borrow to fund day-to-day public spending by the end of this parliament

- To get government debt falling as a share of national income by the end of this parliament

The Treasury declined to comment on “speculation” ahead of the OBR’s final forecast, which will be published on 26 November alongside the Budget.

However, the chancellor confirmed last week that both tax rises and spending cuts are options as she aims to give herself “sufficient headroom” against future economic shocks.

Reeves said in her speech on Tuesday that her commitment to her fiscal rules was “iron-clad”.

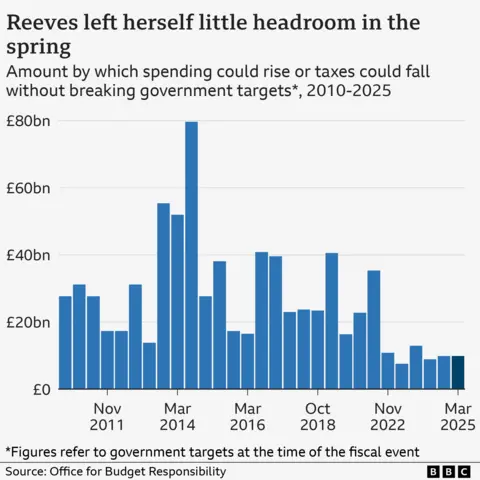

The Resolution Foundation urged the chancellor to use the Budget to give herself more fiscal headroom, meaning how much leeway she has to increase spending or cut taxes without being forced to break her own rules.

After the last Budget, Reeves had £9.9bn of headroom – but the think tank said subsequent policy U-turns and changes in the economic outlook have turned that into a £4bn black hole.

The group said Reeves should double the level of headroom to £20bn in order to “send a clear message to markets that she is serious about fixing the public finances, which in turn should reduce medium-term borrowing costs and make future fiscal events less fraught”.

Last month, the Institute for Fiscal Studies (IFS) said there was a “strong case” to increase fiscal headroom.

The think tank said the lack of a bigger buffer created instability, and could leave the chancellor “limping from one forecast to the next”.

Motorists are facing higher fuel prices ahead of Easter break due to the conflict in the Middle East, the RAC says.

Source link

Business

E-cheques coming soon? RBI unveils Payments Vision 2028, plans wider oversight of digital players – The Times of India

The Reserve Bank of India (RBI) on Friday unveiled its ‘Payments Vision 2028’ document, outlining a roadmap that includes exploring electronic cheques, expanding regulatory oversight to digital platforms, and strengthening safeguards in the fast-growing payments ecosystem, PTI reported.The central bank said it will examine the introduction of e-cheques to combine the advantages of paper instruments with the speed and reliability of digital payments. “To leverage the unique benefits of paper-based instruments and the speed and reliability of electronic payments, and cater to new business use cases, the introduction of electronic cheques in India shall be explored,” the RBI said.Alongside, the RBI is considering widening the regulatory ambit to include entities such as e-commerce marketplaces and centralised platforms that play a growing role in facilitating digital transactions.“In addition, e-commerce marketplaces and centralized platforms have been assuming significant responsibilities that could have implications on the orderly functioning of the payments ecosystem. These aspects shall be examined in detail and, if required, the scope of direct regulations shall be extended to cover such entities,” the document said.The vision document also proposes allowing users to enable or disable transactions across digital payment modes, similar to controls available for card transactions.To address fraud risks, the RBI is exploring a “shared responsibility framework” under which both the issuing bank and the beneficiary bank would share liability in cases of unauthorised digital transactions.The central bank also plans to review cheque design and security features, introduce a Domestic Legal Entity Identifier (DLEI) framework for better transaction traceability, and bring in a Cyber Key Risk Indicators (KRI) framework for non-bank payment system operators.Other initiatives include exploring white-label solutions in the Aadhaar Enabled Payment System (AePS), developing interoperability in the Trade Receivables e-Discounting System (TReDS), and introducing a ‘Payments Switching Service’ to ease customer migration across platforms.The RBI said it will also review the cross-border payments ecosystem to improve efficiency and streamline authorisation processes, alongside publishing periodic reports on global and domestic payment trends.Additionally, the central bank aims to enhance access to payment data and reimagine the card payments ecosystem by promoting secure tokenisation, improved transparency in pricing, and greater choice for users and merchants.

Hyderabad: Pharma player Hetero on Friday said it has rolled out exports of its generic semaglutide injection portfolio as part of a multi-year plan to widen access to treatments for type 2 diabetes and obesity in more than 75 countries.The Hyderabad-based pharmaceutical company said initial rollouts are under way in Africa, Asia and the Middle East, with additional launches planned in other markets subject to regulatory approvals.The injectable therapies will be sold under the brand names Truglyx, Rolmodl and Moto G. Semaglutide belongs to the GLP-1 class of medicines, which are used in diabetes care and weight management.Hetero said the export launch is part of its broader strategy to improve access to advanced cardio-metabolic therapies, particularly in emerging markets.The company said the products will be offered in multi-dose disposable pen devices designed in line with innovator formats and will be available in several strengths, including 0.25 mg, 0.5 mg, 1 mg, 2 mg, 1.7 mg and 2.4 mg, allowing dosing flexibility for both diabetes and obesity treatment.Hetero said it is also awaiting approval from India’s Central Drugs Standard Control Organisation (CDSCO) after completing clinical trials in type 2 diabetes and obesity and plans an India launch after regulatory clearance.Hetero managing director Dr Vamsi Krishna Bandi said the company aims to provide high-quality, affordable generic semaglutide through a single global product platform backed by its manufacturing and development capabilities.He said Hetero would use its commercial networks across Asia, the Middle East, Africa and Latin America to support supply and access. The Hyderabad-headquartered Hetero operates in more than 145 countries and employs over 30,000 people.

FIFA clears Fulham’s Diop, Ajax’s Bounida to play for Morocco

Iranian Hackers Breached Kash Patel’s Email—but Not the FBI’s

Tiger Woods involved in rollover crash in Florida less than 2 weeks before Masters: reports

-

Business7 days ago

Business7 days agoFlipkart group CFO to leave co amid IPO plans – The Times of India

-

Fashion7 days ago

Fashion7 days agoChina’s textile & apparel exports surge 17% to $50 bn in Jan-Feb 2026

-

Sports1 week ago

Sports1 week agoRating Adidas’ 2026 World Cup away shirts: Argentina, Spain, Mexico and more

-

Business1 week ago

Business1 week agoVideo: The Effects of High Oil Prices

-

Sports7 days ago

Sports7 days agoAmerican Conference Commissioner Tim Pernetti thanks Trump for Army-Navy game executive order

-

Fashion1 week ago

Fashion1 week agoThe hidden $1.62 war tax now embedded in every garment you source

-

Tech1 week ago

The Corsair 4000D RS PC Case Keeps Your System Cool

-

Tech1 week ago

Tech1 week ago‘Uncanny Valley’: Nvidia’s ‘Super Bowl of AI,’ Tesla Disappoints, and Meta’s VR Metaverse ‘Shutdown’