Fashion

Mid-market emerges as fashion’s new growth engine: Lectra study

Lectra, a leading provider of Industry 4.0 solutions for the fashion, automotive, and furniture industries, analysed data from Retviews, its artificial intelligence-based solution specialising in competitive intelligence and automatic benchmarking, to identify the trends and pricing strategies that brands are implementing in the Fall/Winter 2025/2026 season to cope with an ever-changing macroeconomic scenario.

“Brand strategies reflect market challenges. Today, product ranges are becoming more streamlined and collections are curated in a more intentional way. At the same time, discounting strategies are shifting: discount rates are decreasing, but promotional periods are becoming longer, as brands aim to preserve pricing power without losing momentum in a market marked by cautious consumer spending,” says Antonella Capelli, President EMEA at Lectra. “Leveraging advanced technologies to obtain and interpret current market insights is now essential for optimising strategies, ensuring consistency with consumer expectations, and, at the same time, guaranteeing solid commercial performance and efficient inventory management. At Lectra, our mission is to support brands in their digital transformation journey by providing tools and solutions that enable truly informed, data-driven decisions.”

Mid-market fashion brands are adopting premium strategies in FW25/26, with European prices rising up to 50 per cent YoY.

Accessories and handbags saw the sharpest gains, while denim and footwear posted moderate growth.

Brands are shifting towards lower but longer discount cycles to preserve pricing power amid tariffs, inflation, and cautious consumer spending.

The mid-market drives profits in fashion

In fashion, business models are undergoing a profound transformation. Mass-market players, which have always competed more directly with low-cost e-commerce giants, are facing increasing pressure due to rising costs and greater inventory risk. These factors, combined with consumers’ focus on value and product quality, mean that the fast-fashion model, characterised by very high volumes and vast assortments, has begun to show signs of slowing down.

It is therefore the mid-market that stands out as the most dynamic and growing segment, even surpassing luxury as a driver of value in the sector. To distinguish themselves from the traditional mass market, mid-market brands are also moving towards a more premium positioning, thanks to more refined designs, more carefully curated assortments, and more ambitious pricing strategies.

Inflation and the effect of tariffs in the “K-economy”

In the UK, consumer price inflation (CPI) reached 3.4% in December 2025¹, keeping shoppers cautious and price-sensitive as they plan discretionary spend.

On the other hand, tariffs introduced by the United States, with rates between 15% and 50%, have increased import costs, forcing brands to make selective price increases that risk further weakening demand.

These dynamics mean that brands are faced with the so-called “K-economy,” a dichotomy in which high-income consumers continue to buy, even increasing their spending, while others reduce it. For brands, this translates into the need to review their pricing and promotional strategies to meet the needs of different consumer segments and, above all, the lower segments that represent the main consumer base for retail.

The premium trend continues for mass brands, with more moderate but longer-lasting discounts

The trend that began in 2025, which sees mass brands moving towards a premium identity, is confirmed. This is demonstrated by the arrival of former creative directors from luxury fashion houses in high-street brand teams, as well as collaborations with prestigious designers to create dedicated capsule collections.

These choices strengthen positioning while justifying higher price points: the Retviews study highlights how, compared to 2024, mid-market brands increased prices by +50% in Europe in 2025, even doubling them in the United States.

Promotional dynamics also confirm strategies aimed at protecting price integrity while maintaining attractiveness, with more moderate but longer-lasting discounts. In Europe, for example, in the period September-December 2025, average discount levels and the number of products with reduced prices were lower than in the same period in previous years.

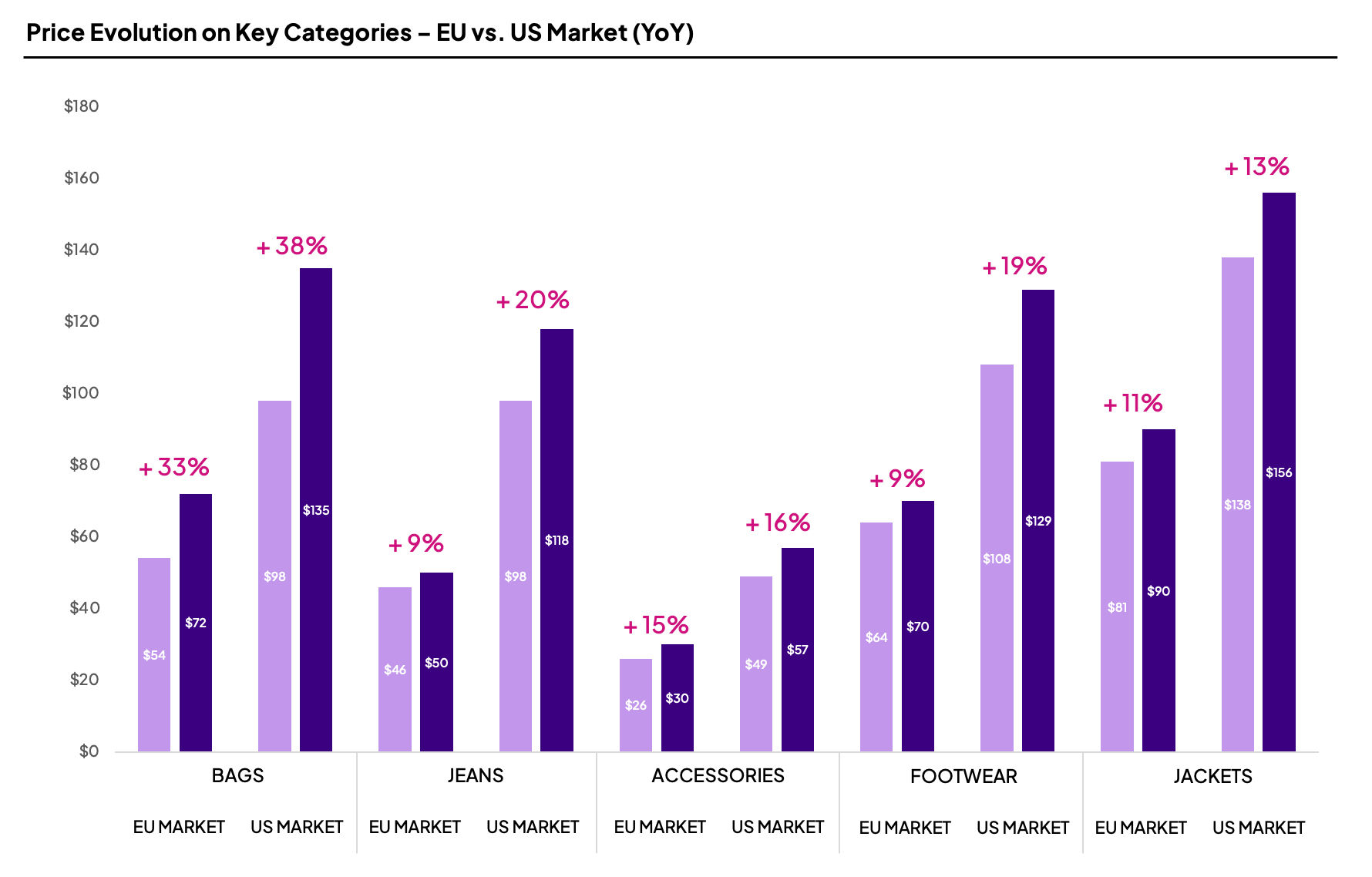

Price trends by product category

For the Fall/Winter 2025/2026 season, the Retviews study shows a general increase in prices for both Europe and the United States. However, not all product categories have increased to the same extent:

- Denim (+9% in Europe, +20% in the United States)

From low-rise to bootcut styles, jeans have historically been a universal garment for all styles and genders. This year, their timeless appeal is proving resilient, with increases in both prices and assortments year-on-year.

- Winter footwear (+9% in Europe, +19% in the United States)

Footwear prices rose significantly in all markets. The main driving factor was growth in the mass market segment, particularly among design-led mid-market brands. This repositioning strengthened pricing power, especially in categories such as footwear, where brands are leaning into highervalue product mixes. The popularity of typical fall and winter styles (such as cowboy-style western boots) has further contributed to price increases, prompting many brands to raise their price lists to capitalize on demand.

- Coats and jackets (+11% in Europe, +13% in the United States)

A must-have for the Fall/Winter season, jackets are not only seeing price increases, but also a significant expansion in the range, with fur jackets, high-necked trench coats, and leather styles making a comeback in response to growing demand for versatile yet bold garments.

- Accessories and lucky charms (+15% in Europe, +16% in the United States)

While consumers continue to prefer timeless bags, charms offer a more accessible way to personalize their look, making this micro-category particularly dynamic. Thanks to their high perceived value relative to price, accessories favor moderate price increases, which consumers are more likely to accept. It is therefore not surprising that mass-market and mid-market brands are following the example of luxury brands, which have significantly expanded the presence of bag charms in their collections, with an increase of more than 50% year-on-year in the European market.

- Handbags (+33% in Europe, +38% in the United States)

Handbags are experiencing a real boom in the mass “mid” market, driven largely by the influence of social media, where luxury fashion houses dictate trends that are then reinterpreted in the collections of major brands. In this context, the category is experiencing significant growth, with an increase in assortment presence of +27% in Europe and +10% in the United States.

Methodological note: the percentage data refer to the periods between September 1 and December 1, 2025, and the same periods for previous years.

Note: The headline, insights, and image of this press release may have been refined by the Fibre2Fashion staff; the rest of the content remains unchanged.

Fibre2Fashion News Desk (MS)

The partnership is rooted in a shared mindset: ambition, world-class performance, global relevance, and a bold confidence that defines both BOSS and the Australian Open. As a cornerstone of BOSS’s cultural strategy, the collaboration creates a powerful platform to connect with fans at scale, unlock new audiences, and showcase the full world of BOSS through its collections, ambassadors, and experiences.

BOSS will become Official Lifestyle Outfitter of the Australian Open from 2027, marking a key step in its sport and culture strategy.

The brand will dress up to 4,000 staff and elevate on- and off-court style through tailored looks, activations and merchandise, strengthening its global presence in tennis while redefining the tournament’s visual identity.

“We are absolutely excited to partner with the Australian Open, which is one of the most dynamic and globally followed sporting events worldwide,” stated Daniel Grieder, CEO of HUGO BOSS. “This collaboration is a natural fit for us, as it brings together two brands that share the same commitment to excellence, innovation, and creating extraordinary experiences. Tennis is part of BOSS’s DNA. The partnership therefore

marks an important step in our strategy to further drive the brand’s positioning at the intersection of sport, lifestyle, and global fan engagement.”

“The Australian Open has always been about more than just great tennis – it’s about atmosphere, innovation, and setting the benchmark for major sporting events worldwide,” Tennis Australia CEO Craig Tiley said. “BOSS is a global brand with impeccable credentials in sport and style, and together we will enhance how our tournament looks, feels, and connects with fans from around the world.”

In its new role as the tournament’s Official Lifestyle Outfitter, BOSS is set to transform the visual identity of the Australian Open like never before. Dressing up to 4,000 staff, officials, umpires, and ball kids, BOSS will make an unmistakable impact, setting its signature confident style from the very first moment. The result is a bold step change: a unified, elevated, and distinctly modern aesthetic that will be visible across every corner of Melbourne Park. A curated palette of refined shades, subtle nods to the brand’s tailoring expertise, and easy-wear silhouettes engineered for the Melbourne heat come together to signal a new era in tournament style – perfectly in tune with the fast-paced, high-energy spirit of the event.

BOSS branding will also be displayed around the venue, including inside the iconic Rod Laver Arena. Beyond the tournament’s courts, the collaboration will extend to exclusive replica teamwear, merchandise, and off-court capsules. Dedicated pop-up stores, immersive on-site fan activations, an elevated guest experience, and further special events will bring the BOSS attitude to every part of “The Happy Slam.” Online and in store, impactful storytelling and curated initiatives will also share the sunshine spirit of Melbourne with tennis fans around the globe.

In a powerful opening serve that ignites excitement and sets the tone for what’s to come, the brand has created bold visuals to accompany today’s announcement. Bridging the worlds of fashion and sport, the imagery reimagines tennis balls in tactile fabrics – from rich wool to soft alpaca – as a nod to BOSS’s roots in craft and tailoring.

The brand’s history in tennis dates back to the 1980s, when it embarked on a 15-year-long sponsorship of the Davis Cup, the world’s largest international team competition in men’s tennis. Most recently, BOSS has welcomed star players Taylor Fritz and Matteo Berrettini, as well as emerging talents Noma Noha Akugue and Ella Seidel, as brand ambassadors, and since 2022 has served as title sponsor of popular ATP 250 tournament the BOSS OPEN in Stuttgart. Through the Australian Open partnership, BOSS is cementing its presence in tennis at one of the world’s most prestigious tournaments and propelling its position as a leading global style authority at the intersection of sport and culture.

Note: The headline, insights, and image of this press release may have been refined by the Fibre2Fashion staff; the rest of the content remains unchanged.

Fibre2Fashion News Desk (JP)

Sovereign ratings in Southeast Asia are under risk due to the Middle East conflict. Fiscal and external metrics underpinning the ratings will be strained if the global energy market does not begin to normalise in the next few months, the credit rating agency noted.

Prolonged energy disruptions will raise fiscal and external pressures on Southeast Asian nations, according to S&P Global.

Indonesia is more vulnerable to weakening credit metrics if the war continues and energy prices remain high.

Vietnam’s strong economic growth, its booming export sector and relatively unencumbered government balance sheet will act as ballast against the energy market dislocation.

If the longer-term impact of the war is severe, the robust growth prospects of economies dependent on imported energy may also be impaired, weakening economic support for the ratings, it said.

Its base case assumes the war’s intensity will peak and the Strait of Hormuz’s effective closure will ease during April, but some disruptions are likely to persist for months.

A prolonged surge in the cost of energy imports—coupled with a loss of foreign exchange reserves—is one risk scenario that could materially weaken Vietnam’s external liquidity position, the credit rating agency said in a regulatory article.

And a sharp increase in the fiscal deficit, in the unlikely event that economic growth also decelerates abruptly, could also erode the government’s more favourable leverage profile, it noted.

If these scenarios persist beyond six months and the government is unable to mitigate the impact on credit metrics, they could erode Vietnam’s robust credit buffers at the current ratings level.

If the pressure on the economy causes capital outflows, the authorities may use foreign exchange reserves to support the exchange rate.

The budget deficit in the country could also widen if the energy disruption drags on. Outcomes will ultimately be tied to the duration of the conflict and the disruptions, it said

Meanwhile, the sovereign ratings on Indonesia (BBB/stable/A-2) are sensitive to weakening fiscal or external credit metrics resulting from the war.

Potential risks include higher energy prices raising budgetary subsidy payments, weighing on deficits; government interest payments rising if accelerating inflation fuels a further increase in market interest rates; and importing more expensive oil products widening the current account deficit (CAD).

The government’s response to the energy disruption may contain some of the damage to its fiscal performance, S&P Global Ratings noted. But, higher commodity prices could also boost government revenue. This helps to limit the increase in the size of the fiscal deficit and reduces upward pressures on the budgetary interest payment ratio.

Indonesian exports have grown this year, but the growth momentum is tempered by declining sales of energy products. With the sharp rebound in energy prices, Indonesian export growth could rise further to mitigate the increase in oil imports.

Overall, Indonesian credit metrics are likely to weaken marginally under the credit rating agency’s base case.

As a commodities exporter, Indonesia may see some mitigating developments offsetting some of the pressures on the sovereign ratings, particularly if there is a broad-based strengthening of commodities prices. This could help to turn around some of the worsening trend in the country’s credit metrics once the situation normalises.

Fibre2Fashion News Desk (DS)

The report titled ‘Impacts of the Conflict in the Middle East on African Economies’, cautions that African economies, which were slowly recovering from the severe consequences of COVID-19, the Russia-Ukraine war and rising trade tariffs, could be among the most affected by the ongoing conflicts in the Middle East.

Growth in African countries is projected to decline by up to 0.2 per cent this year due to the Middle East crisis, according to a joint policy document by the African Union Commission, the African Development Bank Group, the UN Economic Commission for Africa and the UN Development Programme.

The main effects of the conflicts on Africa include surging prices of hydrocarbons, food products and fertilisers.

Kevin Urama, chief economist and vice president for economic governance and knowledge management at AfDB who presented the report on the sidelines of the Spring Meetings of the International Monetary Fund and the World Bank in Washington, DC, recently, urged African governments not to panic or take hasty decisions that could harm their fiscal balances.

The main effects of Middle Eastern conflicts on African economies include surging prices of hydrocarbons, food products and fertilisers, noted the report.

“Eighty per cent of the oil imported into Africa comes from this region, as well as 50 per cent of refined petroleum,” said ECA executive secretary Claver Gatete.

The report recommends, in particular, strategic inflation management to ensure short-term price stability expectations. It cautions oil-exporting countries to adopt strict fiscal discipline by managing windfall revenues prudently, while strengthening debt-monitoring, and using energy reserves strategically.

Where fiscal space allows, it advises that temporary and targeted social protection measures be deployed to shield the most vulnerable populations from the crisis, added the report.

However, the report urged governments to avoid broad-based subsidies that could worsen long-term fiscal deficits, and to diversify sources of energy, inputs and food supplies.

It also recommends that African governments strengthen regional and intra-African trade in oil and fertiliser markets to enhance resilience; and ensure smooth inter-institutional coordination to harmonise strategic monetary and fiscal policies.

At the same time, the report calls upon development partners, multilateral banks and development finance institutions to provide emergency support to African countries through crisis response measures and technical assistance.

It also recommends a speedy operationalisation of the African Continental Free Trade Area (AfCFTA), while strengthening large-scale domestic capital mobilisation.

The report also suggested Africa to diversify its energy mix by accelerating investments in renewable energy and the gas sector.

Fibre2Fashion News Desk (DS)

Singer D4vd charged with murder in death of 14-year-old found in his car

Christina Applegate exhibits strength amid ‘health issues’

Stephen A. Smith makes brutal gaffe while talking about the Golden State Warriors

-

Fashion5 days ago

Fashion5 days agoFrance’s LVMH Q1 revenue falls 6%, shows resilience amid Iran war

-

Sports1 week ago

Sports1 week agoThe case for Man United’s Fernandes as Premier League’s best

-

Entertainment1 week ago

Entertainment1 week agoPalace left in shock as Prince William cancels grand ceremony

-

Business1 week ago

Business1 week agoUK could adopt EU single market rules under new legislation

-

Entertainment5 days ago

Entertainment5 days agoIs Claude down? Here’s why users are seeing errors

-

Fashion1 week ago

Fashion1 week agoEnergy emerges as biggest cost driver in textile margins

-

Business1 week ago

Business1 week agoDelta Air Lines unveils first new Delta One suite in premium cabin arms race

-

Tech1 week ago

Tech1 week agoA Lot of Shops Won’t Fix Electric Bikes. Here’s Why