Business

GST 2.0: Axis report predicts shift from capex to consumption-led growth; MSMEs, consumer sectors seen as key beneficiaries – The Times of India

The government’s announcement of Goods and Services Tax (GST) rationalisation under GST 2.0 signals a major change in India’s economic approach, moving from capex-led spending to a consumption-driven model, according to a report by Axis Securities.“The government has now shifted gears from capex-oriented spending to consumption-led spending,” the brokerage said, adding that the February 2025 Budget had already started this transition by introducing tax reliefs for rural households and the middle class.

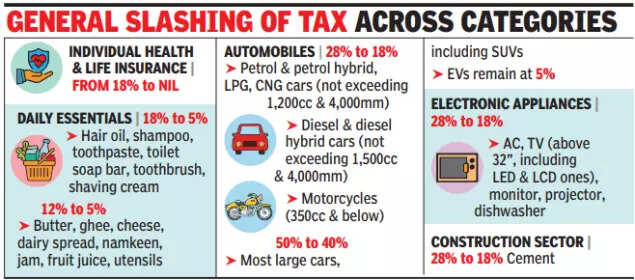

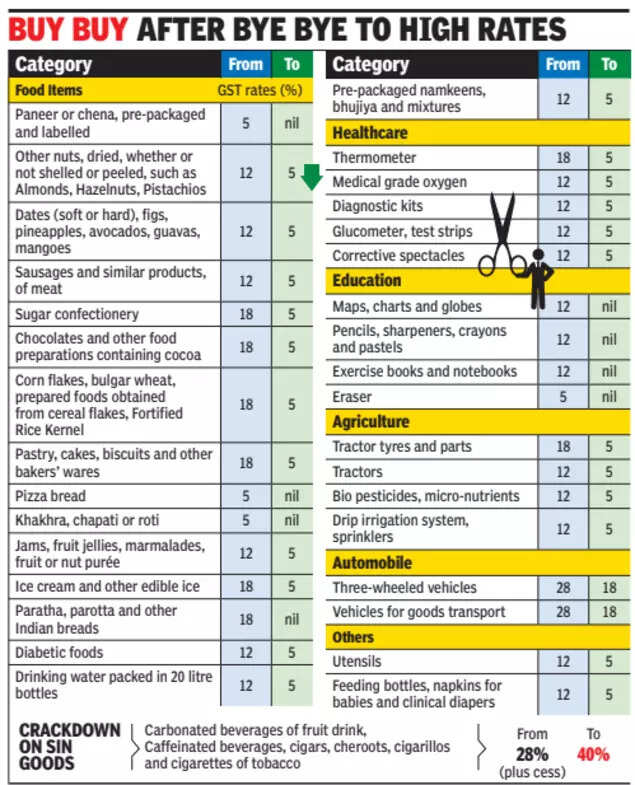

As per news agency ANI, the report noted that over the last decade, infrastructure projects like roads, bridges and metro networks defined government policy. However, GST 2.0, approved in the 56th GST Council meeting on September 3, marks a new phase aimed at boosting demand. The reforms rationalise the structure by reducing slabs from four to three, scrapping the 12% and 28% categories. Most items now fall under 5% and 18%, while a 40% slab is reserved for sin goods. Certain essentials have been placed under a Nil GST rate to directly spur consumption. These changes will take effect from September 22, coinciding with Navratri’s first day.

As per ANI, Axis Securities said the move is expected to benefit MSMEs and SMEs and revive credit growth, while boosting consumer demand in sectors such as durables, retail, FMCG, automobiles, cement, real estate, and building materials. The report added that higher discretionary income will strengthen the consumer discretionary segment, eventually reviving private capex, which has remained weak.Union commerce and industry minister Piyush Goyal also described the GST reforms as “game-changing” and the “biggest reform since independence,” reported news agency PTI. He said the move would support demand across sectors, benefit every consumer, and play an important role in India’s growth journey towards becoming a developed country by 2047.

“Every stakeholder in the country, every consumer, stands to benefit,” Goyal said, urging industry to pass on the benefits. He credited Prime Minister Narendra Modi for leading what he called the “biggest ever reform that India has seen since independence.”The minister added that the reforms, coming ahead of the festive season, are like a “Diwali gift” that will not only reduce taxes on daily essentials but also create a virtuous cycle of greater demand, investment, and job creation.

Spirit Airlines check-in Kiosks sit idle at Oakland International Airport on August 13, 2025 in Oakland, California.

Justin Sullivan | Getty Images

Spirit Airlines could shut down as early as 3 a.m. ET Saturday, according to people familiar with the matter. The carrier has failed to secure a financial lifeline to continue operating, though it hasn’t commented on the potential shutdown or its plans.

About 290 Spirit flights are scheduled for Saturday, according to aviation site Flightradar24. Another 381 are scheduled for Sunday.

Travelers with Spirit tickets could be understandably rattled. While there have been some U.S. airlines to shut down in recent years, the budget carrier is larger than most recent airline failures and links major cities like New York, Miami, Detroit and Los Angles — and many others in between — with its Airbus jets.

Here’s what travelers need to know:

You have a Spirit ticket. What should you do?

Immediately? Nothing.

Travelers who are booked on a Spirit flight, like this CNBC reporter is for later this month, are likely to receive a refund if they purchased tickets with a credit card.

If the ticket was bought with a debit card or with loyalty points, however, the chances of recovering funds are slim to none, said Henry Harteveldt, founder of Atmosphere Research Group, a travel consulting firm.

“If you’re holding a reservation for a flight on Spirit don’t proactively cancel it. Wait for the airline to announce it is shutting down,” he said.

Would Spirit be able to help you at the airport?

Don’t count on it.

Spirit has declined to comment on a potential shutdown. If it confirms an end to operations, the carrier will most likely have information on its website about travelers’ next steps.

Harteveldt said travelers shouldn’t go to the airport expecting to find Spirit staff in the event the airline ceases operations. Call centers are likely to be overwhelmed if they are still staffed.

That could leave passengers with fewer answers than they’d like, but other airlines are likely to help assist affected customers.

Airlines that offer last-minute fares, likely with some discounts, will be available to travelers at airport ticket counters.

How can another airline help?

United Airlines, JetBlue Airways, Frontier Airlines and American Airlines are among the carriers that have said they are ready to assist Spirit customers and crews if the carrier shuts down.

That could mean scheduling additional flights to carry the stranded passengers, similar to what they do during a hurricane or other natural disaster.

Why could Spirit shut down?

Spirit, known for bright yellow planes, low fares and fees for everything else, had been successful for years, but this week it’s been on the brink of liquidation after failing to reach a deal with bondholders for a $500 million government bailout from the Trump administration.

Last year Spirit filed for its second bankruptcy in less than a year, though it’s had a host of problems even before then.

A plan to be acquired by JetBlue was blocked. Rising costs upended its business model. An engine defect grounded dozens of its planes. And, more broadly, upscale travel became more popular with consumers, driving airline profits.

At the same time, big, legacy airlines were selling their own basic economy fares that were similar to what Spirit was offering, but with bigger networks.

What does this mean for travel going forward?

Airlines have been adding flights since Spirit’s bankruptcy filing last year on some of its routes and at major airports. They’re likely to keep doing so.

Experts have said they expect fares to rise, at least in some markets, if the discounter goes away, even though the carrier has shrunk substantially.

Business

Middle East crisis: Air India to make food optional, help cut price of tickets – The Times of India

NEW DELHI: Desperate times call for desperate measures. Full service Air India is planning to make meals optional on its domestic and short international (under two hour) flights. Once this “unbundling” rolls out in the next month or two, passengers opting out of meals could have upwards of Rs 250 shaved off their ticket price. While this move, say people in the know, is “on the anvil,” the airline is looking at several other unprecedented measures to fly through the severe cost-revenue turbulence caused by the unending West Asia war.While not opting for meals could lead to slightly cheaper economy tickets, AI is looking at unbundling lounge access for business class passengers because those opting out of this, could get their tickets cheaper. On an average, lounge operators charge Rs 1,100-1,400 per user at metro airports and Rs 600-700 at non metros.The average spend is about Rs 1,000 per lounge. Many business class flyers are frequent travellers who just make it to airports in time for their flight and do not head to the lounge. If unbundled, this could be a saving in their ticket cost. Banks have been reducing lounge access for credit card users for the same reason to cut their costs.“From Day One, Air India has had meals bundled in its ticket price. Now the way aviation turbine fuel (ATF) price is rising and the rupee crashing since Feb 28, ticket prices are going up. India is a price-sensitive market and raising fares beyond a point leads to a fall in traffic with many opting to travel by train or road. This has led to the rethinking to unbundle meals on some flights. Other steps are also being considered,” said people in the know.Several airlines globally have over the past few years unbundled their onboard offerings. Many international full service airlines offer a basic meal in economy while giving the option of buying gourmet meals at an additional cost. Ditto for alcoholic beverages, with cheaper beer and wines being given at no extra cost while the others being charged for. “For passengers, the distinction between full service and low cost airlines is blurring very fast,” said an industry old-timer.

A tree surgeon said he thought he “was going to die” when he suffered a powerful electric shock from an overhead line while clearing hedges in Wiltshire.

Joshua Pocknell was working just after midnight on the A3102 near Royal Wootton Bassett when the mobile lighting tower he was pushing touched an 11,000 volt overhead powerline.

The 26-year-old was seriously injured and taken to hospital, where he spent the next five weeks, workplace watchdog the Health and Safety Executive (HSE) said.

“My whole body locked and I felt hot and cramping,” Mr Pocknell said of the shock.

“I could hear the electricity in my head and thought I was going to die.

“I hit the floor and passed out, still cramping.

“I later discovered a hole had burnt through my arm and hip all the way to the bone.”

More than two years after the incident on January 19 2024, the tree surgeon said he still experiences “considerable pain”.

“My injuries were complex and challenging and there were five or six different surgeons involved in my treatment,” he said.

“I still experience considerable pain and strange bodily sensations, including nerve pain and itching.

“This incident has torn the life from beneath me and I don’t think I will be able to return to the job that I used to love.”

The regulator said it investigated the incident and found Mr Pocknell’s employer, Upton Specialised Tree Services, did not properly plan for or risk assess the dangers posed by overhead power lines.

The firm did not put up barriers or provide training in operating the mobile lighting tower.

Upton Specialised Tree Services pleaded guilty to the charge of breaching Regulation 14 of the Electricity at Work Regulations 1989 by virtue of Regulation 3, the HSE said, and was fined £60,000 and ordered to pay £6,237 in costs at Bristol Magistrates’ Court on Friday.

HSE inspector Tom Preston said: “Joshua is lucky to be alive.

“Overhead electrical power lines present extreme risks to workers, but the risks can and must be controlled.

“Work near overhead power lines should only be carried out where it can be done safely, following a suitable risk assessment, the use of barriers or safety zones, and proper training on the equipment being used.

“In this case, a worker sustained severe injuries in a traumatic incident for all concerned that was entirely preventable.

“HSE will take action against those who fail to take the steps necessary to protect people at work.”

ICE cotton witnesses sharp rise on weaker dollar, strong exports

Sydney Sweeney hard launches her romance with beau Scooter Braun

AAFA pushes for swift US House passage of key anti-counterfeiting law

-

Business1 week ago

Business1 week agoFrance Ends Airport Transit Visa Requirement for Indian Travellers | Business – The Times of India

-

Tech1 week ago

Tech1 week agoThey Wanted to Join Raya. They’ve Been on the Waiting List for Years

-

Fashion1 week ago

Fashion1 week agoCanada forms new advisory committee to strengthen US trade relations

-

Tech5 days ago

Tech5 days agoA Brain Implant for Depression Is About to Be Tested in Humans

-

Tech5 days ago

Tech5 days agoAlmost 90% of women leave tech industry within 10 years | Computer Weekly

-

Tech1 week ago

Tech1 week agoWhy Do I Like Dyson’s PencilVac So Much?

-

Entertainment1 week ago

Entertainment1 week agoAnne Hathaway makes shocking confession about Taylor Swift’s music

-

Fashion1 week ago

Fashion1 week agoNorth India cotton yarn steady despite continued push by spinners