Business

“India Will Not Only Meet But Possibly Exceed IMFs Estimates,” Says Union Minister Piyush On India’s Booming GDP

New Delhi: Union Minister of Commerce & Industry, Piyush Goyal highlighted on Wednesday the International Monetary Fund’s (IMF) recent revision of India’s growth estimate, which increased from 6.4% to 6.6% for this year, stating that this upward revision is an indication to India’s strengthened economy, driven by increased consumer spending, accelerated investment in infrastructure, and a confident business atmosphere.

He also attributed the growth to the government’s proactive measures, including reduced GST rates, which have led to increased consumer spending and GST collection. Goyal futher showed optimism, stating that with a 7.8% GDP growth in the first quarter, India is set not only to meet but possibly exceed the IMF’s estimates, firming its position as one of the world’s fastest-growing economies.

While speaking to reporters outside the Indian Chemicals and Petrochemical Conclave 2025 held at Bharat Mandapam, Goyal said, “The International Monetary Fund (IMF) has recently revised its growth estimates for India, increasing the projected growth rate from 6.4% to 6.6% for this year. This reflects India’s strengthened economy, the country’s confident atmosphere, increased consumer spending due to reduced GST rates, and accelerated investment in infrastructure. While global growth is expected to weaken to 3.2% this year, India’s growth is nearly double that rate. The first quarter saw a 7.8% GDP growth rate, and it is anticipated that India will not only meet but possibly exceed the IMF’s estimates, continuing to be one of the world’s fastest-growing economies. PM Modi’s vision for a developed India by 2047 seems promising.”

Goyal also highlighted the recent surge in GST collection in September, following the rate cuts, and attributed it to Prime Minister Modi’s vision for a developed India by 2047.

“Despite initial concerns about reduced spending and GST collection in August due to anticipated GST rate cuts, September saw increased GST collection, and the market witnessed a surge in consumer spending post the rate cuts. PM Modi has gifted the Indian consumers, especially the lower and middle classes, with these economic benefits.” Goyal added.

On Wednesday, Minister Goyal addressed the distinguished captains of industry at the Indian Chemicals and Petrochemical Conclave 2025 held at Bharat Mandapam, New Delhi, emphasising India’s pathway to global leadership through innovation, technology, and competitiveness.

Applauding the sector’s vital role in nation-building, Goyal said that the chemicals and petrochemicals industry is “omnipresent in every facet of modern life, from agriculture to automobiles, healthcare to infrastructure and must be at the forefront of developing cutting-edge solutions that power India’s growth.”

Reflecting on India’s vision for Viksit Bharat @2047, the Minister called upon industry leaders to set ambitious goals, urging the sector to aspire to become a USD 1 trillion industry by 2040, thereby contributing significantly to India’s target of a USD 35 trillion economy by 2047.

“Our biggest challenge as a nation is that we often don’t aim big enough,” Goyal said. “Innovation, science, and research must be the backbone of India’s progress. The chemicals and petrochemicals sector has the potential to be a global champion in technology-driven growth and sustainability.”

He noted that advanced nations have achieved prosperity through long-term investments in research and development, and India must similarly anchor its growth in innovation. Goyal highlighted that even oil-rich nations are diversifying into renewable energy and clean technologies, recognising that the future belongs to value-added, sustainable industries.

Acknowledging the industry’s strategic importance to the economy, he emphasised collaboration across the value chain and the need for greater self-reliance in critical materials, while also integrating with global markets to enhance competitiveness.

“We must support each other within our value chains, strengthen domestic capabilities, and at the same time, engage confidently with the world,” the Minister added. “A vibrant, innovative chemicals and petrochemicals sector will be central to India’s journey toward becoming a developed economy.”

CII s report on “People Powering Progress: Building India’s Chemical Workforce for a USD 1 Trillion Industry” was released during the Special Plenary Session with Piyush Goyal, Hon’ble Minister of Commerce and Industry, at the 7th edition of Indian Chemicals and Petrochemicals Conference 2025.

The report captures insights on the transformative potential of India’s chemical industry with projections to reach USD 400-450 billion by 2030 and potentially USD 850-1,000 billion by 2040, driven by global supply chain dynamics, domestic demand, and technological advancements. The sector, contributing 7% to India’s GDP and 14% of industrial output, serves as a catalyst for growth across a wide range of sectors.

R Mukundan, President Designate, CII; Chairman, CII National Committee on Chemicals and Petrochemicals; and Managing Director & CEO, Tata Chemicals Ltd., underlined the role of trade and technology partnerships in shaping the sector’s global positioning.

Opportunities opened through Free Trade Agreements (FTAs) enable the strengthening of the ecosystem for R&D, technology partnerships, and trade linkages. These efforts foster customer development and position the chemical industry as a resilient, future-ready global player. Collaboration and partnerships in research and technology will power India’s next leap, strengthening our ecosystem for R&D and global collaboration to make India a chemical manufacturing powerhouse.

Salil Singhal, Chairman of the CII Indian Chemicals and Petrochemicals Conference, Member of the SCALE Committee, and Chairman Emeritus of PI Industries, welcomed recent policy reforms that support the industry. The unveiling of the HSN Code Mapping Guidebook, along with simplified regulatory pathways, strengthened credentials, and empowered MSMEs, marks a landmark reform.

These initiatives bring clarity, precision, and responsiveness to policy frameworks, creating opportunities for meaningful participation in India’s growth story, particularly in the chemical sector.

Chandrajit Banerjee, Director General, CII, highlighted the critical role of government initiatives in strengthening the sector’s competitiveness. The chemical sector’s significant contribution to manufacturing is widely recognised. Within the broad spectrum of Make in India, initiatives such as the Production Linked Incentive (PLI) scheme, PM Gati Shakti, and the National Logistics Policy have played a crucial role in integrating the chemicals and petrochemicals industry into India’s broader manufacturing ecosystem.

Business

NaBFID signs pact with PDCOR to expand advisory support for state projects – The Times of India

The National Bank for Financing Infrastructure and Development (NaBFID) has signed a Memorandum of Agreement with Projects Development Company of Rajasthan Limited (PDCOR) to strengthen advisory services for state and city-level infrastructure projects.The agreement will also allow both institutions to jointly explore financing and transaction advisory opportunities, including transaction structuring, commercial and technical due diligence, and support for financial closure of projects undertaken by state governments and urban local bodies across India, according to PTI.“This collaboration seeks to enhance access to long-term institutional finance for State Governments and Urban Local Bodies, while strengthening the infrastructure advisory and financing ecosystem,” Rajkiran Rai G., Managing Director of NaBFID, said.He added that the partnership would help both institutions jointly pursue project advisory opportunities, develop replicable financing frameworks, accelerate financial closures and mobilise capital across the infrastructure value chain.Monika Kalia, DMD-CFO, NaBFID, said the tie-up would leverage the strengths of both organisations to provide much-needed advisory support to states and urban local bodies for impactful urban infrastructure projects.Dileep Chingapurath, Chief Executive Officer, PDCOR, said the agreement would address the long-felt need for end-to-end professional support to structure and mobilise sustainable financing solutions, particularly for state governments and their agencies.“Through this collaboration, both institutions aim to enhance the quality of project preparation, mobilise institutional capital more effectively and accelerate the implementation of sustainable infrastructure projects across states and municipalities,” he said.NaBFID is a Development Financial Institution focused on long-term infrastructure financing, while PDCOR is an undertaking of the Government of Rajasthan.

Business

Explained: On way to 4th largest, how India slipped to 6th rank & what it means for 3rd largest economy dream – The Times of India

In April 2025 when the International Monetary Fund (IMF) released its World Economic Outlook, India was seen overtaking Japan to become the world’s fourth largest economy by the end of 2025-26. One year later, India has slipped to the sixth position on the largest economies rankings, with the United Kingdom reclaiming its spot as the fifth largest economy.In fact, IMF’s latest World Economic Outlook (April 2026) sees India sitting at the sixth spot this financial year too. This projection comes even as India has grown better than expected in FY26 and is seen retaining its tag of being the world’s fastest growing major economy.What has led to the sudden fall? Why has India dropped to the sixth position, falling behind the UK, instead of overtaking Japan to become the fourth largest economy? And what does this setback mean for its dream of becoming the third largest economy by the end of this decade? We decode:

Data drive: India projected as 4th largest, but fell to 6th spot

First let’s look at some IMF data to see which way the Indian economy was headed in April 2025, and what the April 2026 outlook data suggestsAs per April 2025 estimates of IMF, India’s economy would have been at $4601.225 billion at the end of FY 2025-26, overtaking Japan which was estimated at $4373.091 billion. The UK at the 6th spot was projected to have a nominal GDP of $4040.844 billion.However, as per the April 2026 estimates, India’s economy had a nominal GDP of $4,153 billion at the end of FY 2025-26, with the UK overtaking it with $4,265 billion GDP. Japan’s GDP is seen at $4,379 billion.As the above estimates show, India’s GDP estimates have seen a drop over one year, while UK’s nominal GDP has grown better than expected. Japan has been steady.So, what went wrong? Blame the rupee and GDP data itself!

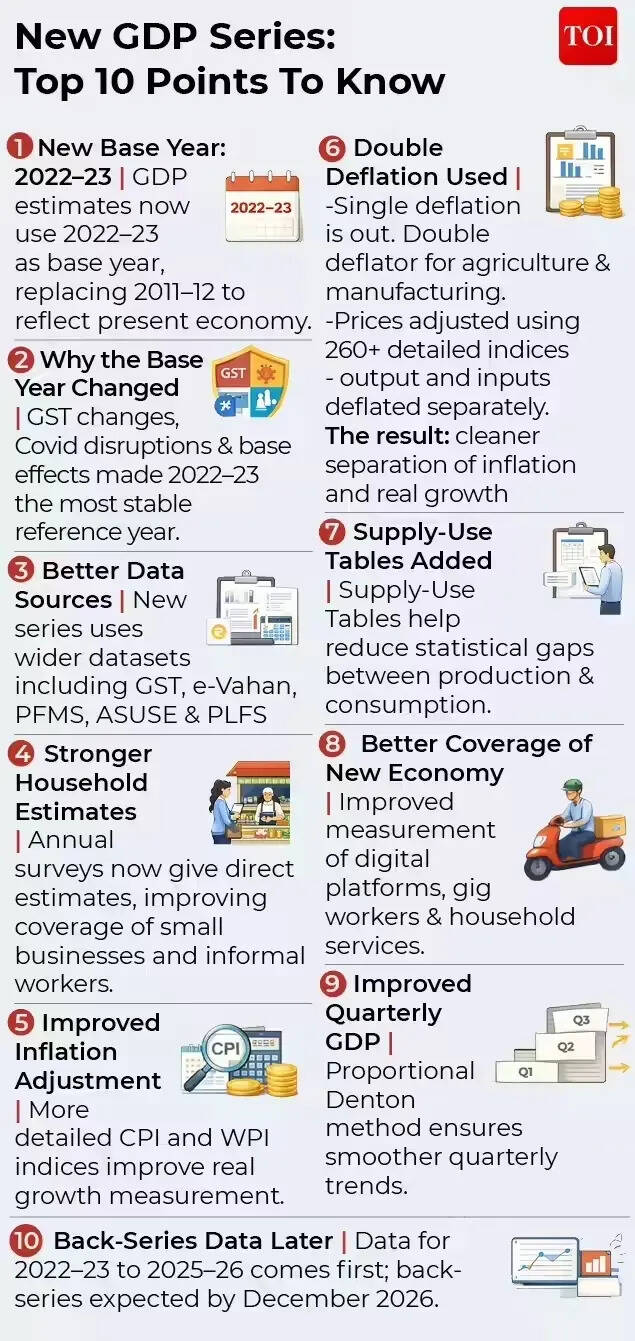

Rupee Depreciation Blow & New GDP Series

The first thing to understand is that IMF’s data on the size of a country’s nominal GDP is in dollar terms. Hence, with global rankings based on dollar‑denominated GDP, they are highly sensitive to exchange rate movements. The biggest party pooper for India’s dream of becoming the fourth largest has been the rupee’s slide. The Indian currency has depreciated more than expected over the last year, dropping from 84.57 versus the US dollar in 2024 to 88.48 in 2025, as per IMF data. The IMF estimates see it at 92.59 this year.Several factors have contributed to the rupee’s decline, including capital outflows, uncertainty related to India-US trade deal up until February, and the recent Middle East conflict which has raised crude oil prices and India’s import bill. Also, the RBI while actively managing volatility in the forex market, is not targeting any particular level of the rupee.Arun Singh, Chief Economist, Dun & Bradstreet India says that India’s recent slip to sixth place in global GDP rankings does not reflect a weakening of the economy, but is largely the result of currency conversion effects and a one‑time statistical revision.The rupee’s depreciation from 2024 to 2026, has mechanically compressed India’s GDP in dollar terms, effectively halving apparent growth despite strong domestic expansion, says Arun Singh.According to Ranen Banerjee, Partner and Leader, Economic Advisory Services, PwC India, GDP in US dollar terms would shave off with rupee depreciation. “We have had almost 7-8% depreciation over the last few months owing to the conflict and portfolio outflows. Thus, in effect in US dollar terms, it is close to shaving out almost a year’s nominal GDP,” he tells TOI.And it’s not just about the Indian economy. The United Kingdom which has overtaken India to bag the 5th spot again also has economic factors working in its favour. UK’s GDP growth at 0.5% has recently beaten forecasts of 0.1% by a wide margin. Not only that, its currency – pound – has actually appreciated against the US dollar.The second factor that has impacted the rankings is India’s adoption of a new base year for its latest GDP series. As per the new data, which also makes use of a more refined methodology, the size of India’s nominal GDP in rupee terms has gone down. Sample this: As per the older base year of 2011-12, India’s GDP at the end of 2025-26 would have been Rs 35,713,886 crore. But under the new series, it is estimated to be Rs 34,547,157 crore. The new calculation methodology and base year revision presents a more accurate picture of the size of the Indian economy.Hence the currency effect has been compounded by a one‑time downward revision following India’s shift to a new GDP base year, which has lowered reported nominal levels without affecting real activity.

Does India’s drop to 6th indicate fundamental weakness?

Experts are confident that India’s growth story is intact and fundamentally strong, a fact that is reflected in projections of it continuing to be the world’s fastest growing major economy. They see technical factors behind the current slip, rather than any deterioration in economic fundamentals.It’s also interesting to note that while India will be the sixth largest economy in FY27, in the upcoming financial year, it is likely to overtake both the UK, and Japan to bag the fourth spot.Arun Singh of Dun & Bradstreet India explains this resilience with numbers:IMF World Economic Outlook (April 2026) data show that India’s GDP at current prices in domestic currency rose strongly from ₹318 trillion in 2024 to ₹346.5 trillion in 2025 and further to ₹384.5 trillion in 2026, translating into robust nominal growth of about 8.9% in 2024–25 and nearly 11% in 2025–26, among the fastest globally. In contrast, other large economies recorded more moderate domestic nominal growth – around 5% in the US, roughly 4% in China, 3–5% in the UK, 3–3.5% in Germany, and lower or volatile growth in Japan – underscoring India’s strong underlying momentum. In times of global economic turmoil, while GDP growth is expected to take some hit, most agencies and experts have pegged India’s growth to be strong. Incidentally, the IMF has even marginally raised its GDP growth forecast for FY27 to 6.5% despite the ongoing Middle East conflict.

“In India, growth for 2025 is revised upward by 1.0 percentage point relative to October, to 7.6 percent, reflecting the better-than-expected outturn in the second and third quarters of the fiscal year and sustained strong momentum in the fourth quarter,” IMF said in its latest outlook. “For 2026, growth is revised upward moderately by 0.3 percentage point (0.1 percentage point relative to January) to 6.5 percent, led by positive contributions from the carryover of the strong 2025 outturn and the decline in additional US tariffs on Indian goods from 50 to 10 percent, which outweigh the adverse impact of the Middle East conflict. Growth is projected to stay at 6.5 percent in 2027,” it added.

Will India become 3rd largest anytime soon?

The rupee depreciation and the nominal GDP revision has also pushed back India’s dream of becoming the third largest economy by the end of this decade. In the October 2025 estimates, IMF had said that India will overtake Germany to become third largest by FY30. However, the April 2026 projections see it reaching the third rank only by FY 2030-31.Experts point to the rupee’s depreciation versus the dollar to note that the road ahead is likely to be uncertain. Madan Sabnavis, Chief economist, Bank of Baroda is confident that India will continue to do well in the coming years.“We will definitely improve in terms of GDP growth which will be higher than that of other countries especially UK and Japan which are just above us. However, the rupee value will finally determine how India gets placed on the global scale,” he told TOI.Ranen Banerjee of PwC India sees rupee beginning to get support with the conflict containment, relatively lower oil prices and portfolio flow reversals with valuations getting attractive in recent times. “Thus, we should not be experiencing any further sharp depreciation of the rupee in the immediate term provided the conflict does not escalate and oil prices relatively softening from their highs and come down to a range of $85-90 a barrel,” he says.For Arun Singh of Dun & Bradstreet, looking ahead, India’s relative position in US dollar‑based GDP rankings will remain highly sensitive to currency movements rather than domestic growth dynamics. “Continued global dollar strength or capital‑flow volatility may cause periodic slippage in rankings despite robust fundamentals. Sustaining external macro stability and limiting undue rupee volatility will be crucial for India’s strong growth performance to translate more fully into higher global economic rankings,” Arun Singh told TOI.The Indian economy, largely driven by domestic fundamentals, is not immune to external shocks. High US tariffs of 50% from August 2025 to early February, and the ongoing US-Iran war have spelt back-to-back shocks for the economy. Even as experts stress on the resilience of the growth story, the vulnerability to higher crude oil prices, and other global supply chain disruptions is a reality. In such a scenario, India may well have to contend with fluctuating world rankings, while banking on its strong GDP growth to tide over disruptions.

new video loaded: Why Your Paycheck Feels Smaller

By Ben Casselman, Nour Idriss, Sutton Raphael and Stephanie Swart

April 18, 2026

Ariana Grande teases new era after ‘Eternal Sunshine’ with cryptic video

I don’t regret gifting Nobel prize to Trump: Venezuela’s Machado

NaBFID signs pact with PDCOR to expand advisory support for state projects – The Times of India

-

Politics1 week ago

Politics1 week agoIndian airlines hit hardest after Dubai limits foreign flights until May 31

-

Entertainment6 days ago

Entertainment6 days agoPalace left in shock as Prince William cancels grand ceremony

-

Sports5 days ago

Sports5 days agoThe case for Man United’s Fernandes as Premier League’s best

-

Politics1 week ago

Politics1 week agoChinese, Taiwanese will unite, Xi tells Taiwan opposition leader

-

Entertainment1 week ago

Entertainment1 week agoDua Lipa hits major career high ahead of wedding with Callum Turner

-

Business1 week ago

Business1 week agoThe FAA wants gamers to apply for air traffic control jobs

-

Business5 days ago

Business5 days agoUK could adopt EU single market rules under new legislation

-

Sports1 week ago

Sports1 week agoLamar Jackson hits back at critics with faithful message on social media