Business

Interest rates expected to be held by Bank of England

Kevin PeacheyCost of living correspondent

Getty Images

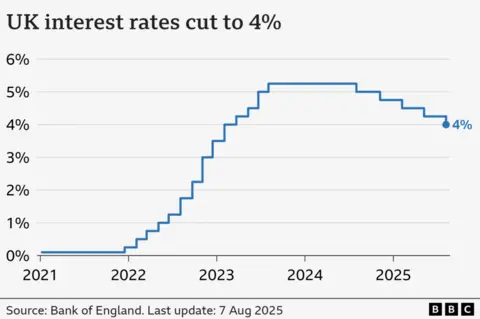

Getty ImagesInterest rates are widely expected to be held at 4% when policymakers at the Bank of England meet on Thursday.

The Bank rate, which heavily influences borrowing costs and savings rates, was cut from 4.25% to 4% by the Bank’s Monetary Policy Committee (MPC) at its last meeting in August.

It took the rate down to its lowest level for more than two years, but many analysts believe there will be no further cuts during the rest of this year.

The decision will be revealed at 12:00 BST and comes after official data on Wednesday showed prices were rising at nearly twice the target level, driven by the higher cost of food.

The rate of inflation remained at 3.8% in August, well above the 2% target. The Bank rate is policymakers’ main tool for controlling inflation.

In theory, making borrowing more expensive means people have less money to spend, which slows prices rises. However, increasing borrowing costs can also harm the economy.

Closely-watched vote

The decision to cut the Bank rate in August was taken after an unprecedented second vote by the nine members of the MPC.

Andrew Bailey, governor of the Bank, said the decision to cut interest rates was “finely balanced”.

Analysts expect Thursday’s vote to be more clear cut, with no change expected.

The relatively high rate of inflation means policymakers are unlikely to risk pushing that higher by cutting the Bank rate.

However, they do expect the inflation rate to start to drop soon, which leaves the possibility open of further interest rate cuts.

The Bank rate has a big impact on the interest homeowners face when taking out a new fixed-rate mortgage.

Lenders use the Bank rate to set their own rates. As a result, the expectation of interest rate rises can push up mortgage rates while the expectation of interest rate cuts can pull mortgage rates down.

Mortgage rates have dropped very slightly since the MPC’s last meeting in August, but further moves are uncertain, according to Rachel Springall, from the financial information service Moneyfacts.

“Many will be waiting with bated breath for the Budget. This waiting game, alongside forecasts for inflation to remain above target, makes it less likely for the Bank of England to make further rate cuts this year,” she said.

She said that savers had seen a downward trend in returns during the time when the Bank has been lowering the Bank rate.

“The average easy access [savings] rate has fallen further below 3%, so savers must act now and switch their variable rate account if it no longer pays a decent return on their hard-earned cash,” she said.

Global picture

The government would be keen to see interest rates fall further, to boost growth in the UK economy.

The Resolution Foundation think-tank, which which focuses on those on low to middle incomes, said living standards needed to improve after a “lost” 20 years of growth.

But ministers will be aware of the inflationary risk that remains in the UK, especially as prices are rising slower in countries such as the US, Germany, and France.

Thursday’s MPC decision will come after the US central bank chose to cut interest rates on Wednesday to a range of 4% to 4.25% for the first time since December.

Last Thursday, the European Central Bank chose to hold its interest its at 2%.

When you think of an investor, what kind of person comes to mind? What are their interests, their job? Are they an older man wearing a pin-striped suit and a bowler hat?

It might surprise you that the average investor age in the UK is 49 years old – down from 55 years old over the last five years.

And with more than 13 million DIY investor accounts in the UK, it’s likely that the average investor looks more like one of your mates than someone out of The Wolf of Wall Street.

The UK is historically quite wary of investing, and it’s been something that the financial industry and governments have been trying to tackle for years.

We’re starting to see the fruits of these efforts trickle through; latest Boring Money data reveals that DIY investing accounts grew over 19 per cent in the last year. Roughly one-third of the population now invests, up from about a quarter in 2020, and it’s becoming more mainstream by the day.

Start small, stay consistent – let the market do the work

It’s a common misconception that you need to have a lot of money to be an investor. The median amount invested by DIY investors is around £15,000, but you can start with as little as £1.

Neither does it have to be done in one big hit. Lots of providers allow you to set up regular investing – often £25 a month minimum, but a few let you regularly invest less.

Setting up these direct debits can also be a good idea – you drip feed into markets and average out the price which you buy at, so smoothing out any ups and downs along the way.

And you don’t have to be a maths genius or obsessively checking the markets – there are plenty of tools and account types that can do this for you.

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

ADVERTISEMENT

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

ADVERTISEMENT

Robo-advisors are automated, algorithm-driven financial planning and investment services requiring little to no human supervision. A typical robo-advisor asks questions about your financial situation and future goals when you set up the account, then will match you to one of their ready-made portfolios and automatically invest for you.

Find your investment “playlist”

If you don’t want to go down the robo-route, but aren’t sure which to pick, you can take a look at some of last year’s best-selling funds for inspiration. These four funds below appeared on multiple investment platforms’ best-selling lists every month in 2025.

They are all low-cost global collections of shares which are well diversified. Think of them like an investment playlist curated for you to serve up a bundle of shares in one easy-to-buy package.

The idea is that you can buy one product which is very broadly spread around lots of different companies which minimises the risk of any one thing going horribly wrong.

Fidelity Index World: a very cheap way to buy about 1,300 of the world’s largest companies in one go, pre-wrapped into one single investment product which costs about £1.20 a year for every £1,000 invested here.

HSBC FTSE All-World Index: a similar global option with over 3,000 companies and emerging markets too, so you get exposure to India, China and Brazil too, for example. Good if you don’t want too much exposure to the US.

Vanguard FTSE Global All Cap Index: a very diversified option. It has shares in about 7,000–8,000 companies with a small proportion in smaller companies, about 10 per cent in emerging markets, and slightly less in the US than some peers – a bit pricier than some trackers but still really good value – about £2.30 a year for every £1,000 invested here.

Vanguard LifeStrategy 100% Equity: one with a heavier British weighting – about 20 to 25 per cent invested in the UK.

Starting from scratch

If you’re a total beginner and want one of these global options to get started, you could compare platforms which will let you buy funds and won’t cost a lot for a small amount. Hargreaves Lansdown and AJ Bell are good options if you have small balances and want to buy a fund like the above. Or you can open an ISA with Vanguard and pop one of their ready-made ‘LifeStrategy’ funds into it.

If you prefer to buy and sell shares or exchange traded funds then Trading 212 and Freetrade are good low-cost ISA providers for smaller balances.

Investing has never been easier.

The average investor age is dropping, the amount you need to invest is low, and people are investing less, but more regularly. There are plenty of different platforms, things to invest in and ways to invest.

People talk about “time in the market, not timing the market” – that means if you’re in it for the long-haul, and can afford to invest small amounts regularly, you’ll be in a great place further down the line. The most important thing is to just get started and build up over time.

When investing, your capital is at risk and you may get back less than invested. Past performance doesn’t guarantee future results.

Britain’s competition watchdog has vowed to tackle fake and misleading online reviews “head on” as it launched investigations into firms including Just Eat and Autotrader.

The Competition and Markets Authority (CMA) said reviews are used by 90% of consumers when they buy over the internet and play a large part in the UK’s over £200 billion online retail sector.

But up to 50% of online reviews are fake, according to recent research by tech firm Truth Engine.

The CMA said its latest action against firms comes as part of a clampdown on fake and misleading reviews as shoppers increasingly rely on customer feedback when shopping online.

Emma Cochrane, executive director for consumer protection at the CMA, told the Press Association: “It’s so important that consumers can have trust in those reviews because we know that nine in 10 of us rely on them when we’re shopping, and that retail shopping in the UK is billions of pounds worth a year.

“It’s so important that consumers can have trust and confidence when they’re shopping online.”

Here are the CMA’s tips for spotting and avoiding fake reviews:

– Read the reviews

Shoppers often get taken in by five-star ratings without actually reading what people have to say about a product or service.

“You’ll be surprised at how many reviews sound dubious, overly vague or even totally unrelated to the item they’re supposedly endorsing,” the CMA said.

– Be alert to AI-generated reviews

Artificial intelligence (AI) can be used to make fake reviews sound fluent, polished and highly convincing.

“If a review feels a bit too slick, reads like it’s been perfectly crafted, or uses very similar wording to others, it may not reflect a real customer’s experience,” the CMA warned.

– Take a look at the other ratings

Look beyond the five-star ratings.

Three or four-star reviews are less likely to be fake, and they can be more useful to give a genuine, overall assessment.

– Check out multiple sites

Looking across several sites can help shoppers see patterns and provide a more consistent picture.

“Check a few different review sites. If you’re seeing the same kind of reviews coming up again and again, it’s more likely to be fake,” said Ms Cochrane.

The UK’s competition watchdog says it is looking at five firms in its investigation into misleading online reviews.

Source link

It has never been easier to start investing. As more take advantage, should you?

Skip the TSA Line: Where to Find Travel by Bus, Train, and Boat

Illinois defense gets tough, ousts Houston to reach Elite Eight

-

Entertainment1 week ago

Entertainment1 week agoVal Kilmer revived 1 year after death through AI

-

Fashion6 days ago

Fashion6 days agoChina’s textile & apparel exports surge 17% to $50 bn in Jan-Feb 2026

-

Business6 days ago

Business6 days agoFlipkart group CFO to leave co amid IPO plans – The Times of India

-

Sports7 days ago

Sports7 days agoRating Adidas’ 2026 World Cup away shirts: Argentina, Spain, Mexico and more

-

Business1 week ago

Business1 week agoVideo: The Effects of High Oil Prices

-

Sports7 days ago

Sports7 days agoAmerican Conference Commissioner Tim Pernetti thanks Trump for Army-Navy game executive order

-

Tech1 week ago

The Corsair 4000D RS PC Case Keeps Your System Cool

-

Tech1 week ago

Tech1 week ago‘Uncanny Valley’: Nvidia’s ‘Super Bowl of AI,’ Tesla Disappoints, and Meta’s VR Metaverse ‘Shutdown’