Business

Isas, cars and pensions – how the Budget affects you?

Kevin PeacheyCost of living correspondent

Getty Images

Getty ImagesChancellor Rachel Reeves is announcing her Budget, but details were published early by the official forecaster.

Here are the key measures and how they will affect you and your money.

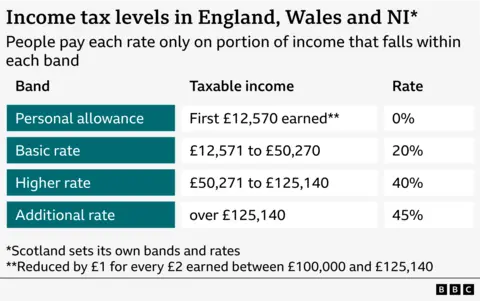

You may pay more tax

The amount of income at which you pay different rates of income tax will still not be increased in line with rising prices.

Instead the bands – known as tax thresholds – will stay frozen until 2031. That is three years longer than previously planned.

This means any kind of pay rise could drag you into a higher tax bracket, or see a greater proportion of your income taxed than would otherwise be expected.

Scotland has its own income tax rates.

You may not earn enough to pay income tax, so VAT, paid when buying goods and services, may hit you harder and that’s been left unchanged.

Driving an electric car will be more expensive

Electric vehicle and hybrid car drivers will be taxed for using the road from 2028.

EV drivers will be charged per mile, on top of other road taxes, in new road pricing.

Calculating the number of miles that drivers cover is difficult.

But fuel duty will continue to be frozen.

You will get a rise if you’re on low pay

The chancellor confirmed increases in April for those on minimum wages.

It means:

- Eligible workers aged 21 and over on the National Living Wage will receive £12.71 an hour, up from £12.21

- If you are aged 18, 19 or 20, the National Minimum Wage increase to £10.85 an hour, up from £10

- For those aged 16 or 17, the minimum wage will rise to £8 an hour, up from £7.55

The separate apprentice rate which applies to eligible people under 19 – or those over 19 in the first year of an apprenticeship – will also increase to £8 an hour, from £7.55.

If your home is worth £2m you will pay more tax

Anyone who lives in a home valued at £2m or more in England will face a council tax surcharge from April 2028.

There will be four price bands with the surcharge rising from £2,500 for a property valued in the £2m to £2.5m band, to £7,500 for a property valued in the highest band of £5m or more

While known as a mansion tax, it may also capture homes in expensive areas, and will be levied on about 100,000 properties, primarily in London and south east England.

The move will require the valuation of homes in the top council tax bands – F, G and H – for the first time since 1991.

You can check your council tax band here if you are in England and Wales, Scotland, and Northern Ireland.

Travelling by train in England won’t cost you more

Regulated rail fares in England will be frozen until March 2027 – the first time they have been left unchanged for 30 years.

These fares include season tickets covering most commuter routes, some off-peak return tickets on long-distance journeys and flexible tickets for travel in and around major cities.

Getty Images

Getty ImagesThe freeze only relates to travel in England, and also only applies to services run by England-based train operating companies.

Train operators are free to set prices for unregulated fares.

The bus fare cap of £3 for a single journey, covering most bus journeys in England, is already in place until March 2027.

Saving in a cash Isa will be restricted

The amount of money that can be saved tax-free each year in a cash Isa (Individual Savings Account) will be reduced from £20,000 to £12,000 a year for the under 65s.

Ministers want people to invest more, which comes with greater risk but could help boost growth – a key objective for the government.

There are questions over whether people would naturally put their money into stocks and shares Isas as a result of the less generous tax break on cash Isas.

About a quarter of those who save money into a cash Isa currently save more than £12,000 a year.

But many of those are pensioners, and the chancellor said the over-65s will still be able to save up to £20,000 in cash.

Separately, the Help to Save scheme, which helps those on low incomes and on universal credit to put money aside, will be extended from 2028.

If you have three children you may get more money

At present, parents can only claim universal credit or tax credits for their first two children.

The chancellor says this two-child cap will be scrapped in April next year.

A limit on what you can save into a pension through salary sacrifice

A third of private sector employees and a tenth of public sector workers use a salary sacrifice scheme for their pension savings.

These workers give up a portion of their salary in return for their employer paying the equivalent amount into their pension. The benefit to both employee and employee is that they make savings in national insurance.

A £2,000-a-year cap on the amount that can be put into pensions through this salary sacrifice arrangement will be in place from April 2029.

Employees would still get income tax relief on their pension contributions, but some argue the move will reduce pension saving incentives.

Most benefits and the state pension will rise

Some benefits, including all the main disability benefits, such as personal independence payment, attendance allowance and disability living allowance, as well as carer’s allowance will rise by 3.8% in April, in line with rising prices.

There will be a string of changes to universal credit in April, following announcements made earlier by the government.

The state pension in April will rise by 4.8% in line with average wages, which means:

- the new flat-rate state pension – for those who reached state pension age after April 2016 – will increase to £241.30 a week, or £12,547.60 a year, a rise of £574.60

- the old basic state pension – for those who reached state pension age before April 2016 – will go up to £184.90 a week, or £9,614.80 a year, a rise of £439.40

In general, you need 35 years of qualifying contributions to get a full state pension.

This brings the state pension closer to being subject to income tax – a source of some debate. It will also reignite discussions over the “fairness” of the so-called triple lock.

More on the milkshake tax, prescription charges and Motability

A range of other measures in the Budget had already become clear or been announced in recent days. They included:

- The UK tax on fizzy drinks will be extended to milk-based products in 2028, taking in pre-packaged milkshakes and coffees that are high in sugar. This may push up prices, or lead to ingredient changes

- The cost of a single NHS prescription in England will be frozen at £9.90 for the second year in a row in April

- Disabled people who have a car through the Motability scheme will no longer be allowed “premium” vehicles such as BMWs, Mercedes, Audi, Alfa Romeo and Lexus

- England’s mayors could be given the powers to charge a levy on overnight stays, sometimes referred to as a ‘tourist tax’. Mayors would decide the level of the charge, and how to spend the money in their areas, under the plans which will be consulted upon

Visa Inc. signage on the floor of the New York Stock Exchange (NYSE) in New York, US, on Wednesday, Jan. 28, 2026.

Michael Nagle | Bloomberg | Getty Images

Visa is launching six new tools using artificial intelligence to modernize the process of disputing credit card charges, the company told CNBC exclusively.

The digital payments company said the tools are designed to reduce the costs and frustration of “outdated” dispute processes for multiple entities involved in the payments process: merchants, issuers and acquirers.

“Some of the challenges are these back-office systems are still largely manual,” Andrew Torre, Visa’s president of value-added services, told CNBC. “We really had to think differently about how we approach this at scale.”

In 2025, Torre said, Visa processed more than 103 million charge disputes globally, marking a 35% increase since 2019.

“Our goal is to streamline this as much as possible,” Torre said. “We’d love to be able to see that growth rate come down.”

Visa’s new tools are part of a larger push by major banks and financial institutions to incorporate AI into their businesses — both internally and in consumer-facing applications. JPMorgan Chase and Goldman Sachs have both said they’re already using AI to hire fewer people. BNY spent $3.8 billion on technology in 2025, or about 19% of its revenue.

Visa said three of its six new tools focus on merchants, allowing them to address potential disputes before they escalate, managing disputes with generative AI responses and providing a deeper level of detail on order insights to manage confusion over unfamiliar charges.

For example, Torre said, many disputes are borne out of cardholders not recognizing a specific charge on their statements. With the new tool, Visa will be able to provide further details to financial institutions to show cardholders that data at a deeper level, according to the company.

The other three tools are built for issuers and acquirers, using predictive AI models to aid in case-by-case analysis, analyzing documents for summaries and auto fill and establishing an AI-powered dispute platform to manage the entire process in one location, Visa said.

“We’ll be able to get them insights and data so they can move from being reactive to proactive,” Torre said.

Torre said Visa’s new AI tools are part of a broader host of solutions for consumers, including a subscription manager announced last week that allows cardholders to cancel unnecessary subscriptions directly on the manager.

The automation will save time, money and unnecessary confusion for both parties, he added. Most of the tools will be generally available later this year, the company said.

“We really believe that disputes in this solution makes it much easier to manage and resolve,” Torre said. “We think it has better outcomes for everyone.”

Food bills are set to soar as much as 10 per cent this year as a direct consequence of the Iran war, a key industry body has warned.

The Food and Drink Federation (FDF), which represents 12,000 food and drink manufacturers, has hiked its inflation forecast for the year from 3.2 per cent to between nine and 10 per cent.

During the 2022 cost of living crisis, food inflation rose at a rate of 10.9 per cent, figures from the Food and Drink Federation (FDF) show, while the following year was even worse at 14.6 per cent.

Since then, it had dropped back to 2.7 per cent (2024) and 4.2 per cent (2025), but while this year had originally been forecast to deliver food inflation of 3.2 per cent, the latest assessment is that it will instead see a huge rise in the second half of 2026.

The FDF said the current situation is “unprecedented and hard to predict”, but it’s “clear that food inflation is going to rise in the months ahead”.

How much that adds to the average bill depends on the size and frequency of a consumer’s usual grocery habits, but on average, bills could rise by around £588, according to some estimates.

Consumer rights and review site Which? frequently assesses UK supermarkets for cost, and at the start of 2026, an average basket of 89 shopping products cost £161.56 at Aldi and up to £217.02 at Waitrose.

Assuming food inflation lands at the mid-point of the FDF forecast, 9.5 per cent, and that all products and supermarkets applied that uplift equally, that would move the costs of those shops up to £176.91 and £237.64 respectively.

Research from confused.com suggested the average UK household spent £119 each week on food shopping, which is £6,188 each year; a 9.5 per cent uplift to that equates to an extra £588 annually, or a total of just over £130 per week and £6,775 annually.

Chancellor Rachel Reeves is due to meet with some supermarket chiefs on Wednesday, including Sainsbury’s and Tesco, over discussions to assess the upcoming impact of price rises on the cost of living. The Treasury has described it as a “fact-finding” conversation.

Last month, Asda boss Allan Leighton called on Labour to do more to help businesses after creating “a lot of constraints” for them.

For food manufacturers, there is both a concern now and another yet to come in terms of energy cost rises.

Diesel – used in farm machinery – is up by 80 per cent since the start of the war, while fertiliser costs could increase further, as well as supply being constrained. The FDF also points to lost sales due to cancelled shipments to the Middle East, with UK firms regularly exporting cheese, cereals, chocolate and more to the region.

Dr Liliana Danila, chief economist at The Food and Drink Federation, said: “The food and drink sector is already feeling the force of this geopolitical shock. As one of the UK’s energy-intensive industries, manufacturers are facing mounting energy bills, rising transport and packaging costs and disruption across key supply chains.

“These pressures are hitting simultaneously and are a significant challenge for businesses to absorb.

“The current situation is unprecedented and hard to predict; however, given the scale and speed of these cost increases, and despite companies’ best efforts not to pass price increases on, it’s clear that food inflation is going to rise in the months ahead.”

The FDF says its upgraded inflation figures were based on “assumptions that the Strait of Hormuz opens to cargo traffic within the next two to three weeks”, as has been suggested by Donald Trump this week, and that most commodities, including oil, gas and fertiliser production, return to normal within a year.

In the past few months, the FDF has repeatedly called for the government to offer support to businesses in the sector from rising energy bills in the same way as it does to those in some other manufacturing areas.

GST collections: India’s net Goods and Services Tax (GST) collections increased to Rs 1.78 lakh crore in March 2026, marking a rise of 8.2% compared to the previous month, according to official figures released on Wednesday.Gross GST revenue for March stood at Rs 2 lakh crore, which is an 8.8% increase over the same month last year.Abhishek Jain, Indirect Tax Head & Partner, KPMG says, “GST collections continue to show steady 9% annual growth, supported by strong import activity this month and consistent compliance. While export refunds have eased this month but remain healthy overall for the year”Refunds during the month totalled Rs 0.22 lakh crore, up 13.8% on a year-on-year basis, which resulted in net GST collections of Rs 1.78 lakh crore.Domestic GST revenue reached Rs 1.46 lakh crore, registering a growth of 5.9%, while revenue from imports was recorded at Rs 0.54 lakh crore, rising sharply by 17.8% during the period.Post-settlement GST figures across states presented a varied trend. While industrially advanced states recorded strong growth, several others reported a decline.Maharashtra contributed the highest amount to the overall collections at Rs 0.13 lakh crore on a pre-settlement basis, followed by Karnataka and Gujarat.Among states showing an increase in post-settlement SGST collections were Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Gujarat, Maharashtra, Karnataka, Kerala, Tamil Nadu, Telangana and Andhra Pradesh, among others.On the other hand, states such as Jammu and Kashmir, Chandigarh, Delhi, Arunachal Pradesh, Meghalaya, Assam, West Bengal, Jharkhand, Odisha, Chhattisgarh and Madhya Pradesh, among others, registered a decline in post-settlement SGST revenues.

Apparel retailer Uniqlo signs landmark deal with Los Angeles Dodgers

Visa launches new AI tools to manage the charge dispute process

New Zealand’s apparel imports down 11% to $216 mn in Jan-Feb

-

Politics1 week ago

Politics1 week agoAfghanistan announces release of detained US citizen

-

Sports1 week ago

Sports1 week agoBroadcast industry CEO says consolidation is ‘essential’ to compete for NFL soaring media rights prices

-

Tech1 week ago

Tech1 week agoCan a Home Appliance Fix the Problem of Soft-Plastic Waste?

-

Business1 week ago

Business1 week agoProperty Play: Home flippers see smallest profits since the Great Recession, real estate data firm says

-

Entertainment1 week ago

Entertainment1 week agoUN warns migratory freshwater fish numbers are spiralling

-

Business1 week ago

Business1 week agoGold prices soar in Pakistan – SUCH TV

-

Fashion1 week ago

Fashion1 week agoICE cotton slips on weaker crude, profit booking

-

Business1 week ago

Business1 week agoMore women are entering wealth management, but few are in advisory roles, study finds