Business

UK inflation: What is the rate and why are prices still rising?

BBC

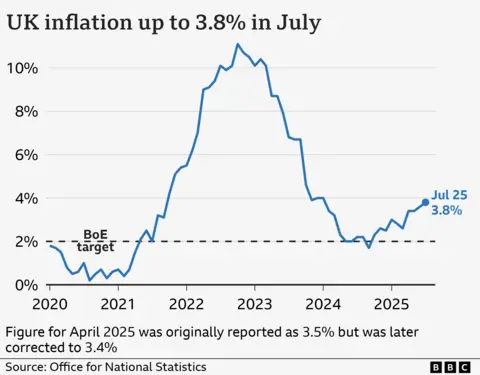

BBCPrices in the UK rose by 3.8% in the 12 months to July, driven by higher air fares, as well as increases in the cost of food.

It means inflation remains above the Bank of England’s 2% target.

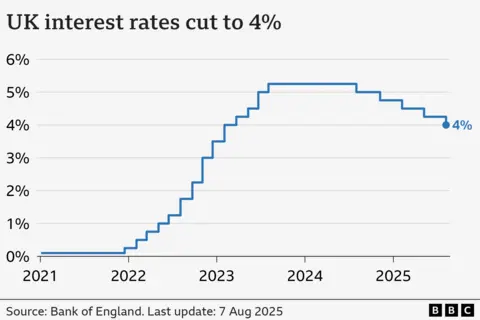

The Bank moves interest rates up and down to try to keep inflation at that level, and has cut interest rates five times since August 2024.

What is inflation?

Inflation is the increase in the price of something over time.

For example, if a bottle of milk costs £1 but is £1.05 a year later, then annual milk inflation is 5%.

How is the UK’s inflation rate measured?

The prices of hundreds of everyday items, including food and fuel, are tracked by the Office for National Statistics (ONS).

This virtual “basket of goods” is regularly updated to reflect shopping trends, with virtual reality headsets and yoga mats added in 2025, and local newspaper adverts removed.

The ONS monitors price changes over the previous 12 months to calculate inflation.

The main inflation measure is called the Consumer Prices Index (CPI), and the latest figure is published every month.

CPI was 3.8% in the year to July 2025, up from 3.6% in the 12 months to June. The July 2025 figure is the highest recorded since January 2024, when the rate was 4.0%.

The Bank also considers other measures such as “core inflation” when deciding whether and how to change rates.

This doesn’t include food or energy prices because they tend to be very volatile, so can be a better indication of longer term trends.

Core CPI was 3.8% in the 12 months to July, up slightly from 3.7% recorded in the year to June.

Why are prices still rising?

Inflation has fallen significantly since hitting 11.1% in October 2022, which was the highest rate for 40 years.

But that doesn’t mean prices are falling – just that they are rising less quickly.

Inflation soared in 2022 because oil and gas were in greater demand after the Covid pandemic, and energy prices surged again when Russia invaded Ukraine.

It then remained well above the 2% target partly because of higher food prices.

These continue to be a significant factor in the current inflation figures.

Inflation for food and non-alcoholic beverages was 4.9% in the year to July, up from 4.5% in the year to June.

Beef, sugar, chocolate, instant coffee and fruit juice saw significant price rises.

But the main factor driving the July inflation figure was higher air fares, which saw the largest July increase since the ONS began collecting that data on a monthly basis in 2001.

In addition, fuel prices fell only slightly between May and June 2025, compared to a larger drop in the same period in 2024.

Why does putting up interest rates help to lower inflation?

When inflation was well above its 2% target, the Bank of England increased interest rates to 5.25%, a 16-year high.

The idea is that if you make borrowing more expensive, people have less money to spend. People may also be encouraged to save more.

In turn, this reduces demand for goods and slows price rises.

But it is a balancing act – increasing borrowing costs risks harming the economy.

For example, homeowners face higher mortgage repayments, which can outweigh better savings deals.

Businesses also borrow less, making them less likely to create jobs. Some may cut staff and reduce investment.

In recent months inflation has remained above the Bank’s target at the same time as the economy has remained relatively flat and the jobs market has softened.

Therefore, the Bank has chosen to cut rates, despite high inflation, in an attempt to encourage people to spend more and get businesses to invest and create jobs to boost the economy.

What is happening to UK interest rates and when will they go down again?

The Bank of England began cutting rates in August 2024, and made five cuts to bring the rate down to 4%.

Bank of England governor Andrew Bailey had said that future cuts will be made gradually and carefully.

The August interest rate decision was extremely close, with the committee voting 5-4 to cut rates by a quarter percentage point.

It followed an unprecedented second vote by the Bank’s policymakers, as one economist wanted a larger cut of half a percentage point.

This suggests future interest rate decisions could also be finely balanced.

Inflation is now expected to peak at 4% in September, the Bank said in its latest Monetary Policy Report. That is twice the Bank’s target rate and above the 3.8% high it predicted in its previous report in May.

A further interest rate cut had been expected at the Bank’s meeting in November, but analysts are now less sure this will happen given the closeness of the August vote.

The Bank also has to consider the wider global economy. Mr Bailey has repeatedly warned about the unpredictable impact of US tariffs, and conflict in Israel and Iran has also created uncertainty.

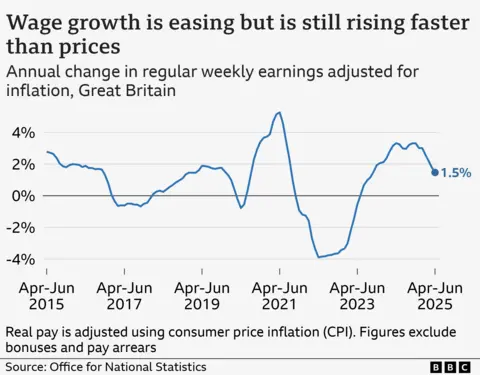

Are wages keeping up with inflation?

Annual average regular earnings growth was 5.7% for the public sector and 4.8% for the private sector.

Meanwhile, separate ONS figures showed the number of vacancies fell again to 718,000 for the May to July period, marking three continuous years of falling job openings.

The unemployment rate was 4.7% in the three months to July – the same as the three months to April.

This marked the highest level of unemployment since June 2021, and is also likely to factor into the Bank of England’s decision whether to cut rates again.

What is happening to inflation and interest rates in Europe and the US?

The US and EU countries have also been trying to limit price increases.

The inflation rate for countries using the euro was 2.1% in August, according to an early estimate.

In June 2024, the European Central Bank (ECB) cut its main interest rate from an all-time high of 4% to 3.75%, the first fall in five years.

By July 2025, after several further cuts, its key rate stood at 2%.

Inflation in the US held steady at 2.7% in July, remaining above the US central bank’s 2% target.

After a string of cuts in the latter part of 2024, the US central bank again chose not to change rates at its July 2025 meeting, the fifth hold in a row.

That leaves its key interest rate unchanged in a range of 4.25% to 4.5%.

The Federal Reserve has repeatedly come under attack from President Trump, who wants to see further interest rate cuts.

Go Digit General Insurance on Saturday said it has received a demand notice of about Rs 170 crore for short payment of goods and services tax (GST) for nearly five years. The company has received an order copy from the Office of the Commissioner of GST & Central Excise, Chennai South Commissionerate on March 6, confirming GST demand of Rs 154.80 crore levying penalty of Rs 15.48 crore and Interest u/s 50 of CGST Act, 2017 for the period July 2017 to March 2022, the insurer said in a regulatory filing. The company is in the process of evaluating the legal advice on the implications and would file an appeal, it said.

Business

India–US trade ties: Piyush Goyal says India secured best deal among competing nations – The Times of India

Commerce and industry minister Piyush Goyal on Saturday said India has secured the best trade deal with the United States among competing nations, highlighting the strength of the economic and strategic partnership between the two countries, reported PTI.Speaking at the Raisina Dialogue 2026 in New Delhi, Goyal said India and the US share a “very powerful” relationship, adding that the world’s largest economy remains an important partner for New Delhi.

“It has been a fantastic journey. We have the best of relations. You would have observed that through the last year, President Donald Trump has always had the best things to say about India as a country, and about Prime Minister (Narendra) Modi. We have fantastic relations with our counterparts there.“Even within your family, sometimes you can have one or two misunderstandings. It’s a part of the course. I think it’s a very, very powerful relationship that the US and India share. And we got the best deal amongst all the nations with whom we compete,” Goyal said.He added that the two countries are strategic partners and the largest democracies in the world, noting that the US, with a $30 trillion economy, remains central to global trade.“We have a large responsibility cast on both our nations. They are the world’s largest economy, USD 30 trillion economy, nobody can wish them away,” he said.Explaining the significance of trade agreements, Goyal said such deals are meant to secure preferential access for a country’s goods and services compared to competitors.“What’s a trade deal? You are trying to get a preference or a preferential access for yourself, your goods, your services, compared to your competitor. And we got the best deal amongst all the competing nations. I mean whether it’s in our neighbourhood Pakistan or Bangladesh. If we look at the Asian region, we got the best deal amongst all of the competitors…” he said.The minister added that the India-US partnership extends beyond trade, encompassing technology cooperation, critical minerals, defence ties and investments.“There’s a huge technology overlay on it. There’s a huge critical minerals partnership, there’s a defense partnership, there’s a huge amount of investments that flow into India from the US. So it’s a partnership of two countries which is going to define the future,” he said.His remarks come as India and the US have finalised the framework for the first phase of a bilateral trade agreement, under which Washington had announced it would reduce reciprocal tariffs on India to 18 per cent.However, after the US Supreme Court struck down the tariffs, President Donald Trump imposed a 10 per cent tariff on all countries from February 24 for 150 days.A meeting between the chief negotiators of the two countries to finalise the legal text of the agreement has also been postponed.Under the proposed deal, India will eliminate or reduce tariffs on US industrial goods and a range of American agricultural products, including dried distillers’ grains (DDGs), red sorghum for animal feed, tree nuts, fresh and processed fruits, soybean oil, wine and spirits, among others.India has also indicated that it plans to purchase $500 billion worth of US energy products, aircraft and aircraft parts, precious metals, technology products and coking coal over the next five years.Goyal also referred to the nine free trade agreements finalised by the Modi government, saying they were negotiated while safeguarding domestic interests.“These nine free trade agreements, I can say on record with all the courage that I have on my command with all the responsibility that in not a single trade deal, has India compromised on any sensitivity of any of our stakeholders,” he said.Opposition parties, however, have alleged that the government has compromised the interests of farmers in the India-US trade pact.Goyal said opening the auto sector under certain FTAs would expand consumer choice and create employment opportunities.“Demand for this industry is growing at an average of 8 per cent. So you can imagine how much more scope we have to create jobs,” he said.He added that while companies from FTA partner countries may initially export cars to test the Indian market, they would eventually need to manufacture locally once demand is established.“Initially they can sell, say, 5,000 cars or 10,000 cars, to test the market, find the distraction — and then come and manufacture here,” he said.He added that the government’s broader objective is to build a global network of trade partnerships through multiple FTAs.

A few years ago, Grace Guo began to crave places in New York City where hanging out with friends didn’t have to involve alcohol.

Newly sober and surrounded by friends who also chose not to drink, Guo said she wanted alternatives to the typical social scene. After some research, she landed on Bathhouse and Othership: social wellness clubs designed to create communities around improving health.

“Honestly, it kind of just feels like going to a spa together and spending an afternoon together. I think for me, it just feels much better rather than staying out late at night,” Guo told CNBC.

She’s one of a growing number of people seeking out membership clubs and other places that are structured around maintaining health while also acting as a spot to foster connection.

And those spaces are becoming booming businesses, too. Bathhouse, which opened in 2019 in Brooklyn, New York, told CNBC exclusively that it expects to hit around $120 million in revenue by the end of this year. It declined to disclose any of its other financials, as did Othership.

Many of these types of companies are privately held, but publicly traded gym chain Life Time also began doubling down on premium wellness a few years ago. While investors initially did not like that reallocation of resources, it’s now paying off, with Life Time’s stock more than doubling since October 2023.

Companies old and new are trying to reach consumers like Guo. The 31-year-old said she’s seen an increased focus on health, wellness and peacefulness in her own social life and in those around her, as she searches for so-called third spaces with that focus.

“I’m kind of like, where can I go to try to plug into a community, or where can I go to express a particular interest that I have and find like-minded people?” Guo said. “It’s finding a group of like-minded people, but then also having the space and the novelty to try something or to pursue something.”

At Othership, between spending time in the sauna and the cold plunge and choosing a popular evening time slot, Guo said the environment of health-focused socializing spoke to her.

“Having a space to go to where it kind of shocks us out of our routine and complacency is really important, and I think probably the biggest thing is just the fact that it overcomes a lot of the inertia of doing something,” Guo said.

‘Loneliness is an epidemic’

Bathhouse pools

Source: Bathhouse

The concept of third spaces isn’t new. The term was first coined by sociologist Ray Oldenburg in his 1989 book, “The Great Good Place,” to refer to spaces outside of the home, or the first place, and work, the second place, where people gather and form relationships.

That definition came to encompass places like neighborhood coffee shops, libraries, bars and more, where people from different backgrounds came together in an informal setting with relatively low barriers to access.

But somewhere in the past few years, that definition has evolved, and the importance of third spaces has blossomed.

Richard Kyte, a professor at Viterbo University in Wisconsin and the author of “Finding Your Third Place,” said he’s been teaching courses on third places for nearly two decades, but only noticed the term becoming mainstream in the past few years.

That turning point, Kyte said, also coincided with the pandemic, which sent the world into lockdowns and practically eliminated social gatherings for a period while redefining them for the long term.

“During that time, all of a sudden, we were talking more about the cost of loneliness, the cost of social isolation. It really came home to us during the pandemic that this was not healthy,” Kyte told CNBC. “And at the same time that we were noticing that we need these places more, we were seeing that so many of them were closing. That kind of spurred a renewed interest.”

It’s a trend that’s also been compounded by an increasingly digital-forward society, he added, as younger generations crave more than just social media connections even with the rise of artificial intelligence and chatbots.

“We’ve got all of this huge investment in technology that increases the ease and desirability of being independent,” Kyte said, citing AI companies promoting products that pose as friends. “When we have people turning more to their screens instead of looking to find fulfillment through social interaction, it just takes all these people out of the pool.”

According to Cigna’s 2025 “Loneliness in America” report, 67% of Gen Zers reported feeling lonely, along with 65% of millennials. A 2024 Harvard survey found that 67% of adults feel social and emotional loneliness because they are not part of meaningful groups.

Harry Taylor first founded Othership alongside his wife and friends to create a space that incorporated the wellness trend while combating that isolation.

“We understand that there’s a huge market for people to meet other people. Loneliness is an epidemic right now,” Taylor told CNBC. “We realized, just through doing this, it has the capacity for people to come together and just be themselves, be vulnerable.”

What’s old is new

Third spaces have evolved to encompass specific purposes, justifying the price tag that often comes with them, since some membership clubs can thousands of dollars per month.

Wellness, specifically, has seen a recent boom, becoming one of the top categories for gifting items last holiday season. Equinox chairman Harvey Spevak told CNBC last month that “health is the new luxury,” with the global wellness market expected to reach nearly $10 trillion by 2030, according to estimates from the Global Wellness Institute.

Bathhouse, which operates roughly 90,000 square feet of facilities in New York City, offers a wellness experience based on the bathhouse legacy of Europe. The space has saunas and cold plunges, both guided and unguided, starting at $40 for a drop-in session. The company’s two New York locations see roughly 1,000 customers each day.

“It was really apparent that there was no bathhouse-like concept that was really oriented towards a modern consumer, especially not in America,” co-founder Travis Talmadge told CNBC.

Talmadge said he and his co-founder were focused on creating a human experience, tapping into each person’s body while also building community around the shared activities.

“Our spaces are really large scale, so one of the nice things is that everybody kind of feels like a background actor on set, where there’s just so many people moving around,” Talmadge said. “You can have this really personal time, either by yourself or with somebody else, but then you’re in this environment with a lot of people doing the same thing.”

Talmadge said the company has seen a “surplus of demand” and runs at a “very healthy margin,” with plans to open seven more locations through 2027.

It’s just one of many wellness spaces growing in popularity.

Othership is also tapping into a wellness mindset, incorporating practices from various cultures to address the “physical, mental emotional and spiritual.” It has locations in New York and Canada, with plans for more growth.

At Othership, members can choose between three options: a free-flow session, designed to allow members to use the space however they want; classes, which alternate between saunas and cold plunges with group-led activities; and socials, imitating clubs without the alcohol in an effort to be present.

Co-founder Taylor said through Othership, he’s seen customers form new friend groups, propose to their partners in the sauna and find belonging with others while also fueling their own health.

Creating alcohol-free spaces was one of the Othership founders’ aims when creating the vision. Othership now hosts comedians, live musicians and more at its saunas to mimic similar spaces seen in big cities that are often associated with alcohol.

“There’s so much social media, which gives us the false perception that there’s social engagement and interaction, but so many of us have experienced when we’re doomscrolling, it almost even does the opposite,” Taylor said. “There’s a void in the wake of that social satiation that we all require as humans, so it’s that coming together and just being so real with one another that really creates a deep sense of belonging.”

Building community

Glo30 skincare studio.

Courtesy: Arleen Lamba

Wellness communities can form in other ways, too. Glo30, a membership studio founded 13 years ago with locations across the country, offers personalized skincare treatments for members every 30 days, creating a schedule aligned with other members to foster community.

“Community building is a lot about not just getting the results and [feeling] good, but also being able to have a commonality on their experiences and share what they feel,” Glo30’s founder and CEO Arleen Lamba told CNBC.

While urban cities like New York and Los Angeles have seen a boom in wellness clubs, Lamba said her more than 100 locations represent the in-between, in places like Texas, Arizona, North Carolina and more.

Every Glo30 appointment is scheduled on the hour in each location to create more opportunities for social connection, Lamba said.

“As people come into the studio, people are also leaving the studio, and we recognize that they recognize each other, they would actually make new friends,” she said, adding that especially post-pandemic, the company has seen a growing number of social groups form in the treatment rooms.

Lamba said she’s seen the craving for social connection increase with the rise of social media, but that creating community can often happen in untraditional places, like Glo30. At the same time, that social interaction isn’t as “overwhelming” as other places like parties or big group events, allowing for intimate socializing, she said.

In the past two years, Lamba said the number of Glo30’s franchise units in development has grown 67.5% as it sees more demand for its services.

The boom of third spaces goes beyond wellness, too. Exclusive restaurant memberships, gyms, creative spaces, social clubs and more are gaining more popularity as consumers search for ways to build community outside of their houses and offices.

At Glo30, Lamba said she’s seen every type of customer base at the company’s locations, from families to girl groups to couples.

“The third space is interesting because it creates a true connection,” she said. “We get to be witness to someone’s life — their highs, their lows, their middles — and we are the constant, and that, to me, is what the third space is about: No matter what kind of day you had out there, good or bad or medium, this space belongs to you. And when you come to this space, people will know you, see you, appreciate you and be glad you’re there.”

Ball State fires Michael Lewis after 3 straight losing seasons

Paul McCartney's overlooked work

Timothee Chalamet’s ‘insensitive’ joke sparks response from Met Opera

India Us Trade Deal: Fresh look at India-US trade deal? May be ‘rebalanced’ if circumstances change, says Piyush Goyal – The Times of India

LPGA legend shares her feelings about US women’s Olympic wins: ‘Gets me really emotional’

Bobby J. Brown, “The Wire” and “Law & Order: SUV” actor, dies of smoke inhalation after reported fire

-

Business1 week ago

India Us Trade Deal: Fresh look at India-US trade deal? May be ‘rebalanced’ if circumstances change, says Piyush Goyal – The Times of India

-

Sports1 week ago

Sports1 week agoLPGA legend shares her feelings about US women’s Olympic wins: ‘Gets me really emotional’

-

Entertainment1 week ago

Entertainment1 week agoBobby J. Brown, “The Wire” and “Law & Order: SUV” actor, dies of smoke inhalation after reported fire

-

Fashion1 week ago

Fashion1 week agoSouth Korea’s Misto Holdings completes planned leadership transition

-

Fashion1 week ago

Fashion1 week agoTexwin Spinning showcasing premium cotton yarn range at VIATT 2026

-

Entertainment1 week ago

Entertainment1 week agoPakistan’s semi-final qualification scenario after England defeat New Zealand

-

Entertainment1 week ago

Entertainment1 week agoWhat’s new in Pokémon? Every game, update, surprise from 30th anniversary event

-

Business1 week ago

Business1 week agoGreggs to reveal trading amid pressure from cost of living and weight loss drugs