Fashion

$6 bn of India’s T&A exports to the EU concentrated in 20 HS codes

Analysis at the product level

Over $6 billion of India’s textile and apparel exports to the EU are concentrated in just 20 four-digit HS codes, out of a total export base of ~$7.5 billion, making the India–EU FTA a sharply product-specific opportunity rather than a broad-based boost.

Finished apparel emerges as the primary beneficiary, as tariff parity improves India’s competitiveness against other Asian suppliers.

India and the European Union have signed the long-awaited Free Trade Agreement (FTA), with the pact expected to come into force in early 2027 (or earlier) following ratification. While trade flows will remain largely unchanged in the near term, product-wise export data indicates that the agreement could reshape India’s textile and apparel exports to the EU over the medium term, with gains concentrated in finished apparel rather than intermediate products.

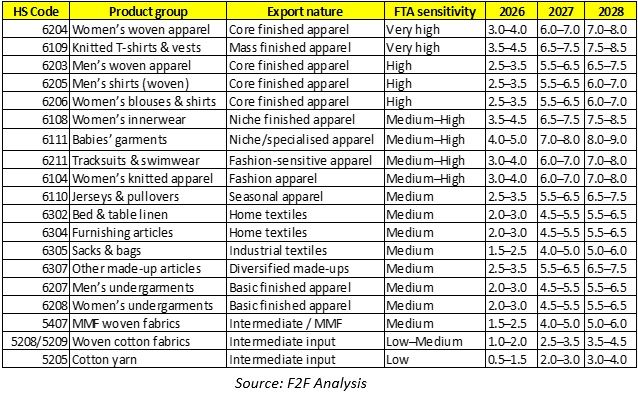

India’s EU-facing textile and apparel exports are highly concentrated. The top 20 four-digit HS codes account for more than $6 billion, out of total textile and apparel exports of roughly $7.5 billion to the EU, underscoring where the FTA’s eventual impact is likely to be most visible.

Apparel dominates India’s EU export basket

Finished apparel forms the backbone of India’s textile and apparel exports to the EU, led by women’s wear, knitted garments, and core woven apparel. Home textiles represent the second pillar, while yarns, fabrics, and fibre-based products contribute a smaller share in value terms.

Table 1: India’s total Textile and Apparel exports to the EU-27 – Top 20 four-digit HS codes (2025)

Export growth in 2026 is expected to remain moderate as buyers focus on audits, compliance checks, and limited pilot orders ahead of implementation. A clearer divergence is expected from 2027, once tariff concessions take effect, with finished apparel emerging as the most responsive category.

Table 2: India–EU textile exports – Product-wise growth outlook (YoY growth %, indicative)

What to watch till 2027

Product readiness is expected to improve fastest in high-volume apparel categories, while home textiles see incremental upgrades rather than greenfield expansion. Compliance alignment, particularly on sustainability and traceability will be a key differentiator, with cotton-based segments better positioned than MMF apparel. Buyer engagement is likely to intensify through audits and pilot orders ahead of implementation, while competing suppliers such as Bangladesh and Vietnam are expected to defend share through pricing and buyer integration rather than capacity expansion. Final tariff schedules and rules of origin will determine which products benefit first.

The India–EU FTA signals a medium-term reset, not an immediate surge. With over $6 billion concentrated in the top 20 product groups, finished apparel is best positioned to lead post-2027 gains, while home textiles compound steadily and intermediates remain less responsive.

Fibre2Fashion News Desk (AA)

The company posted a net loss of $7 million, compared to a net income of $16.3 million in FY24. Adjusted EBITDA fell to $63.6 million, or 6.4 per cent of sales, from $109.1 million, or 9.9 per cent a year earlier.

Torrid Holdings has reported a weak FY25, with sales falling 9.4 per cent to $1 billion and a net loss of $7 million amid margin pressure.

The company closed 151 stores and saw EBITDA decline.

Q4 performance also weakened.

Despite this, Torrid expects modest recovery in FY26, supported by optimisation efforts, improved marketing and a stronger operational foundation.

The company closed a total of 151 stores during the year as part of its retail optimisation strategy, reducing its footprint from 634 to 483 stores, Torrid Holdings said in a press release.

Torrid ended the year with $20 million in cash and cash equivalents, while total liquidity stood at $84.9 million. Net cash used in operations was $13 million, compared to positive operating cash flow of $77.4 million in the previous year.

For the fourth quarter (Q4), net sales dropped 14.3 per cent year-on-year (YoY) to $236.2 million, while comparable sales fell 10 per cent. Gross margin contracted to 30.0 per cent from 33.6 per cent a year earlier. The company reported a net loss of $8.1 million, widening from a $3.0 million loss in the same period last year. Adjusted EBITDA declined sharply to $5.1 million, or 2.2 per cent of sales, compared to $16.7 million, or 6.1 per cent, previously.

During the quarter, Torrid closed 77 stores under its Store Footprint Optimisation Project, taking the total store count to 483 locations.

Commenting on performance, Lisa Harper, chief executive officer at Torrid Holdings, said, “2025 was a transformational year. We delivered $1 billion in net sales, in line with our guidance, and $63.6 million in Adjusted EBITDA, exceeding the high end of our outlook, while making deliberate strategic decisions required to put this business on a stronger footing. We closed 151 structurally unproductive locations, launched five sub-brands that generated approximately $70 million in sales, and fundamentally restructured our product assortment around core franchises and fabrications our customers value most. Trends in Q4 and early Q1 give us confidence that the foundation we’ve built is beginning to take hold.”

Looking ahead, the company expects first-quarter fiscal 2026 net sales in the range of $236 million to $244 million, with Adjusted EBITDA between $14 million and $18 million. For the full year, Torrid forecasts net sales between $940 million and $960 million and Adjusted EBITDA of $65 million to $75 million, alongside capital expenditure of $8 million to $10 million.

“We enter 2026 with a strong operational foundation—optimised channels, product and pricing. This positions us to accelerate customer file growth through renewed marketing efforts, helping us re-engage past shoppers, attract new customers and deepen loyalty across our existing base. I am confident we are on the right path and encouraged by early signs of progress we are seeing in the business,” added Harper.

Fibre2Fashion News Desk (SG)

The People’s Bank of China (PBoC) is set to conduct a one-year medium-term lending facility (MLF) operation worth 500 billion yuan (~$72.52 billion) on Wednesday. The move is aimed at ensuring sufficient liquidity within the banking system.

The People’s Bank of China will conduct a 500-billion-yuan (~$72.52 billion) one-year MLF operation to support banking liquidity.

Conducted via variable-rate tenders, the move will offset 450 billion yuan in maturing funds, resulting in a net injection of 50 billion yuan (~$6.9 billion).

This marks the 13th consecutive month of net liquidity infusion by the central bank.

The operation will be carried out via variable-rate tenders with a fixed volume, using a multiple-price auction mechanism, said Chinese media reports quoting the central bank.

With 450-billion-yuan worth of MLF funds due to mature this month, the latest operation will result in a net liquidity injection of. This marks the 13th consecutive month in which the PBoC has added net liquidity through the facility.

The operation will result in a net liquidity injection of 50 billion yuan (~$6.9 billion), after accounting for 450 billion yuan in MLF funds maturing this month, extending the PBoC’s streak of net injections to 13 consecutive months.

Fibre2Fashion News Desk (SG)

During the second month of ****, apparel and accessories accounted for *.* per cent of Japan’s total imports, which stood at *,***,*** million yen. Imports of textile yarn and fabric rose **.* per cent to **,*** million yen (~$***.** million), representing * per cent of total imports.

On the export side, textile yarn and fabric shipments decreased *.* per cent to **,*** million yen (~$***.** million). Textile machinery exports rose *.* per cent to **,*** million yen (~$***.** million), contributing *.* per cent to Japan’s total exports of *,***,*** million yen.

US’ Torrid sees FY25 sales fall 9.4%, reports $7 mn loss

Wristband enables wearers to control a robotic hand with their own movements

UK inflation rate steady in February ahead of Iran war

-

Fashion7 days ago

Fashion7 days agoSales at US apparel, clothing accessories stores up 4% YoY in Jan 2026

-

Business1 week ago

Business1 week agoPeloton is launching bikes and treadmills for gyms, accelerating commercial strategy

-

Tech1 week ago

Tech1 week agoJustice Department Says Anthropic Can’t Be Trusted With Warfighting Systems

-

Fashion1 week ago

Fashion1 week agoTrump signs order to combat fraudulent ‘Made in America’ labels

-

Business1 week ago

Business1 week agoStocks and pound rise as US rate call approaches

-

Fashion1 week ago

Fashion1 week agoLenzing launches TENCEL Lyocell-HV100 at Intertextile Shanghai

-

Sports7 days ago

Sports7 days agoMarch Madness 2026 – How to watch in SA, start time, schedule, TV channel for NCAA championship basketball tournament

-

Entertainment7 days ago

Entertainment7 days agoVal Kilmer revived 1 year after death through AI