Business

2026 is the year of obesity pills. Here’s how they could reshape the GLP-1 market

The booming GLP-1 space was built on weekly injections. In 2026, new obesity pills will push the market into its next chapter.

Patients are already getting their hands on the first GLP-1 pill for obesity from Danish drugmaker Novo Nordisk — a once-daily drug that shares the same brand name as its popular injection Wegovy. A GLP-1 pill from the company’s chief rival Eli Lilly isn’t far behind, with a U.S. approval expected within months.

For some people, pills may serve as a more convenient — and potentially cheaper — alternative to today’s blockbuster injections. The cash prices of Novo Nordisk’s Wegovy pill range from $149 to $299 per month, depending on the dose, which is slightly less than the newly lowered cash prices of injections.

While the pills aren’t expected to bring more weight loss than weekly shots, based on separate clinical trials, some health experts say expanding the range of treatments could still be a major win for patients.

Pills could attract new patients to seek obesity treatment for the first time, expanding the broader weight loss and diabetes drug market and potentially boosting sales for Novo Nordisk and Eli Lilly. The new users may include people who are afraid of needles, as well as patients who could benefit from existing injections but don’t view their condition as severe enough to warrant a weekly shot.

“I think that there are a lot of people out there who have never tried these GLP-1 drugs and are maybe waiting for the pills to come out,” said Dr. Eduardo Grunvald, medical director of the UC San Diego Health Center for Advanced Weight Management. “It’s kind of a natural preference for some people and even some prescribers.”

“Secondly, if you have to pay out of pocket, the pills are going to be a bit less expensive than the injections, so that’s another reason,” he said.

The logo of pharmaceutical company Novo Nordisk is displayed in front of its offices in Bagsvaerd, on the outskirts of Copenhagen, Denmark, Nov. 24, 2025.

Tom Little | Reuters

It’s unclear exactly how many people are currently using GLP-1s in the U.S., especially for obesity. But around 1 in 8 adults said they were taking a GLP-1 drug to lose weight or treat another chronic condition as of November, according to a poll from health policy research organization KFF.

Now, pills are emerging as the next battleground for Novo Nordisk and Eli Lilly, which established the GLP-1 space that some analysts say could be worth almost $100 billion by the 2030s. In August, Goldman Sachs analysts forecast that pills could capture roughly 24% — or about $22 billion — of the global weight-loss drug market by 2030.

Here’s how obesity pills could reshape the space.

Pills could expand the market

Oral drugs may pull new patients into the obesity treatment market.

“I believe that this will quite a bit expand the market,” Novo Nordisk CEO Mike Doustdar told CNBC in late December. “We know from our own family members and circles of friends that there are many people who still would not rather take an injection … for this group of people, having a pill option is important.”

Pills could prompt some people to start obesity treatment because “they think it’s somehow more acceptable or approachable” than an injection, said Dr. Caroline Apovian, co-director of the Center for Weight Management and Wellness at Brigham and Women’s Hospital.

That doesn’t mean a pill will be the best fit for everyone. But once patients enter the health-care system for treatment, doctors can guide them through all options – whether that’s an injection, metabolic surgery, or structured diet and exercise programs, Apovian said.

UCSD’s Grunvald said uptake of obesity pills is likely to be driven by primary care physicians, who treat the majority of eligible patients and may be more comfortable prescribing an oral drug.

Grunvald said obesity medicine specialists, who care for only about 5% to 10% of eligible patients, are more likely to continue favoring injections, which appear more effective than pills based on separate clinical trials.

Deborah, a 53-year-old librarian in St. Louis, Missouri, said she is curious about the new Wegovy pill in part because of its convenience factor. She declined to provide her last name due to concerns about stigma associated with GLP-1s.

Deborah said she would consider an oral GLP-1 because she is already accustomed to taking pills for other prescriptions. She said an oral drug would also bring other benefits, like making travel easier because it won’t require refrigeration, like injections do.

She said she is also interested in the potentially lower costs of pills. Deborah has been taking weekly injections of Wegovy since June, and was paying $449 per month in cash before Novo Nordisk lowered that price to $349 per month.

Pills cost slightly less

Cost could be a factor for other patients, too.

Novo Nordisk’s pill appears to have among the lowest cash prices in the market, at $149 per month for the starting dose and $299 per month for the two highest doses. Eli Lilly’s rival pill is expected to have similar pricing for cash-paying patients.

Those users will also be able to access the starting dose of both pills for $149 per month through President Donald Trump‘s direct-to-consumer website, TrumpRx, under a deal both companies struck with his administration in November.

Obesity injections have long been hard for patients to get, due in part to spotty insurance coverage and list prices of roughly $1,000 per month. Both Novo Nordisk and Eli Lilly have moved to address those concerns by cutting cash prices for their injectable drugs to less than half that amount.

A combination image shows an injection pen of Zepbound, Eli Lilly’s weight loss drug, and boxes of Wegovy, made by Novo Nordisk.

Hollie Adams | Reuters

Eli Lilly in December said the highest doses of single-dose vials of Zepbound will cost $449 per month for cash-paying patients, while Novo Nordisk in November said nearly all doses of Wegovy will cost $349 per month in cash.

Those prices are closer to the cost of Novo Nordisk’s pill, which may still be expensive for some. But Grunvald said the roughly $150 monthly difference between the highest doses of Zepbound and Novo’s pill “could be a big difference for many people” willing to pay out of pocket.

Patients with insurance coverage for Novo Nordisk’s oral drug can pay as little as $25 per month for the treatment. But pills likely won’t move the needle to boost insurance coverage of GLP-1s for obesity in the U.S.

The direct-to-consumer cash prices of Novo Nordisk’s oral drug are likely “significantly less” than what employers and middlemen called pharmacy benefit managers would pay to cover the drugs, said John Crable, senior vice president of Corporate Synergies, an insurance and employee benefits brokerage and consultancy.

Crable said it is unclear how much the pill will ultimately cost payers such as employers since those prices are not publicly disclosed. But if they mirror injection costs — often higher than $1,000 per month — employers may be reluctant to add the drug to their formularies, he said.

Some companies that already offer coverage of obesity injections could add the pills this year. But Crable said some employers have actually dropped coverage of GLP-1s for obesity in 2026 due to their high costs.

“I don’t see employers being highly motivated to add what is probably going to be another high volume, very high cost drug to their formulary when the direct-to-consumer pricing for it is so much cheaper,” Crable said.

Injections are here to stay

Drugmakers have tried to make a case that patients using injections can switch easily to oral drugs. Eli Lilly in December released data showing that patients who initially took Wegovy or Zepbound shots maintained the majority of their weight loss after switching to the company’s pill.

But Apovian, of Brigham and Women’s Hospital, said cost would be the only real reason to move patients who are doing well on injections to a pill.

“If the [cash price] is similar, I always prefer the injectables because I believe that the weight loss is better and the side effects are less,” she said.

Apovian said she wants to see real-world data on how pills perform compared with injections, but separate late-stage trials already offer some clues.

Zepbound has shown average weight loss of more than 20% in late-stage studies. That’s higher than results seen with both the Wegovy injection and pill as well as Eli Lilly’s oral drug in separate trials.

In those same studies, about 7% of patients or less stopped treatment due to side effects from the Zepbound and Wegovy injections.

The Wegovy pill showed similar discontinuation rates, while about 10.3% of patients taking the highest dose of Eli Lilly’s oral drug stopped treatment because of side effects.

Leerink Partners analyst David Risinger said patients with obesity who need to lose a larger percentage of their body weight will likely stick with injections, unless they have a fear of needles.

Pills, he said, could primarily attract new patients who are overweight or mildly obese and want to achieve only “modest” weight loss.

Some patients currently using weekly injections may try pills, Risinger added, though not all will find a daily oral option more convenient.

That includes Karen Galante, 42, of Horsham, Pennsylvania, who is taking a compounded version of semaglutide – the active ingredient in Wegovy – which she said is priced similarly to Novo Nordisk’s new pill.

Galante said she does not plan to switch.

“It’s hard enough for me to remember to take my vitamins every day,” she said. “I like the set-it-and-forget-it of taking one shot a week.”

More than enough room for Novo, Lilly

Risinger said he expects both pills from Novo Nordisk and Eli Lilly to “take off like a rocket” this year.

He noted that uptake will be greater for the Wegovy pill initially since Eli Lilly’s drug, orforglipron, is likely still months away from entering the market.

But Risinger said he believes Eli Lilly’s pill will ultimately generate higher sales because patients could consider it more convenient.

Eli Lilly’s orforglipron is a small-molecule drug that is absorbed more easily in the body and doesn’t require dietary restrictions like Novo Nordisk’s pill, which is a peptide medication. Patients are supposed to drink no more than four ounces of water with the Wegovy pill and must wait 30 minutes before eating or drinking anything else each day.

But Novo Nordisk’s CEO Doustdar has argued that those dietary requirements won’t hinder uptake. He told CNBC in December it has not been an issue for the more than a million people who are taking the lower-dose version of the pill for diabetes, marketed as Rybelsus, which entered the market in 2019.

“Simply sip and go, and you’re going to be fine,” Doustdar said. “These people are waking up in the morning and taking their pill with a glass of water, and then they do their normal daily routine half an hour later and move on with their life.”

He also called the company’s drug the “most efficacious pill,” saying that no other products in development have been able to show its same level of weight loss in a late-stage trial.

The highest dose of Novo Nordisk’s Wegovy pill helped patients lose up to 16.6% of their weight on average at 64 weeks in one late-stage study. That’s comparable to the injectable form of the drug.

There are no head-to-head studies directly comparing that pill with Eli Lilly’s. In one of Eli Lilly’s late-stage trials, the highest dose of its pill helped patients lose 12.4% of their body weight on average at 72 weeks.

Despite that difference in efficacy, Risinger said the two pills are viewed as promoting roughly similar levels of weight loss. Some patients may also not need to take the highest dose of either pill, he added.

In an August note, Goldman analysts said they expect Eli Lilly’s pill to have a 60% share — or roughly $13.6 billion — of the daily oral segment of the market in 2030. They expect Novo Nordisk’s oral semaglutide to have a 21% share — or around $4 billion — of that segment. The analysts said they expect the remaining 19% slice to go to other emerging pills.

More competitors emerge

Other drugmakers are racing to bring their own oral options to the market, including Pfizer, AstraZeneca, Structure Therapeutics and Viking Therapeutics.

Risinger highlighted Structure’s daily oral GLP-1, which will enter phase three trials later this year. Shares of Structure soared more than 100% on Dec. 9 after it released midstage data showing that its pill, aleniglipron, helped patients with obesity lose more than 11% of their weight at 36 weeks, when adjusted for placebo.

Additional trial data showed that a higher dose of the pill could deliver greater efficacy – more than 15% weight loss – surpassing the results seen with the highest dose of Eli Lilly’s orforglipron. Still, the tolerability data, or how well patients tolerated Structure’s treatment, appeared to be worse than that of Eli Lilly’s pill.

In a release at the time, Structure CEO Raymond Stevens said the pill could be “potentially best-in-class” for an oral small-molecule GLP-1.

Risinger said he expects that pill and another oral GLP-1 from AstraZeneca could launch as soon as late 2028.

He said potential pills that are taken weekly, as opposed to daily, and have “compelling profiles could tilt the balance more towards orals” in the market.

Risinger pointed to privately held Verdiva Bio, which is developing several oral peptide treatments designed to be taken once a week. That company has an ongoing phase two trial on an oral GLP-1.

Business

Explained: On way to 4th largest, how India slipped to 6th rank & what it means for 3rd largest economy dream – The Times of India

In April 2025 when the International Monetary Fund (IMF) released its World Economic Outlook, India was seen overtaking Japan to become the world’s fourth largest economy by the end of 2025-26. One year later, India has slipped to the sixth position on the largest economies rankings, with the United Kingdom reclaiming its spot as the fifth largest economy.In fact, IMF’s latest World Economic Outlook (April 2026) sees India sitting at the sixth spot this financial year too. This projection comes even as India has grown better than expected in FY26 and is seen retaining its tag of being the world’s fastest growing major economy.What has led to the sudden fall? Why has India dropped to the sixth position, falling behind the UK, instead of overtaking Japan to become the fourth largest economy? And what does this setback mean for its dream of becoming the third largest economy by the end of this decade? We decode:

Data drive: India projected as 4th largest, but fell to 6th spot

First let’s look at some IMF data to see which way the Indian economy was headed in April 2025, and what the April 2026 outlook data suggestsAs per April 2025 estimates of IMF, India’s economy would have been at $4601.225 billion at the end of FY 2025-26, overtaking Japan which was estimated at $4373.091 billion. The UK at the 6th spot was projected to have a nominal GDP of $4040.844 billion.However, as per the April 2026 estimates, India’s economy had a nominal GDP of $4,153 billion at the end of FY 2025-26, with the UK overtaking it with $4,265 billion GDP. Japan’s GDP is seen at $4,379 billion.As the above estimates show, India’s GDP estimates have seen a drop over one year, while UK’s nominal GDP has grown better than expected. Japan has been steady.So, what went wrong? Blame the rupee and GDP data itself!

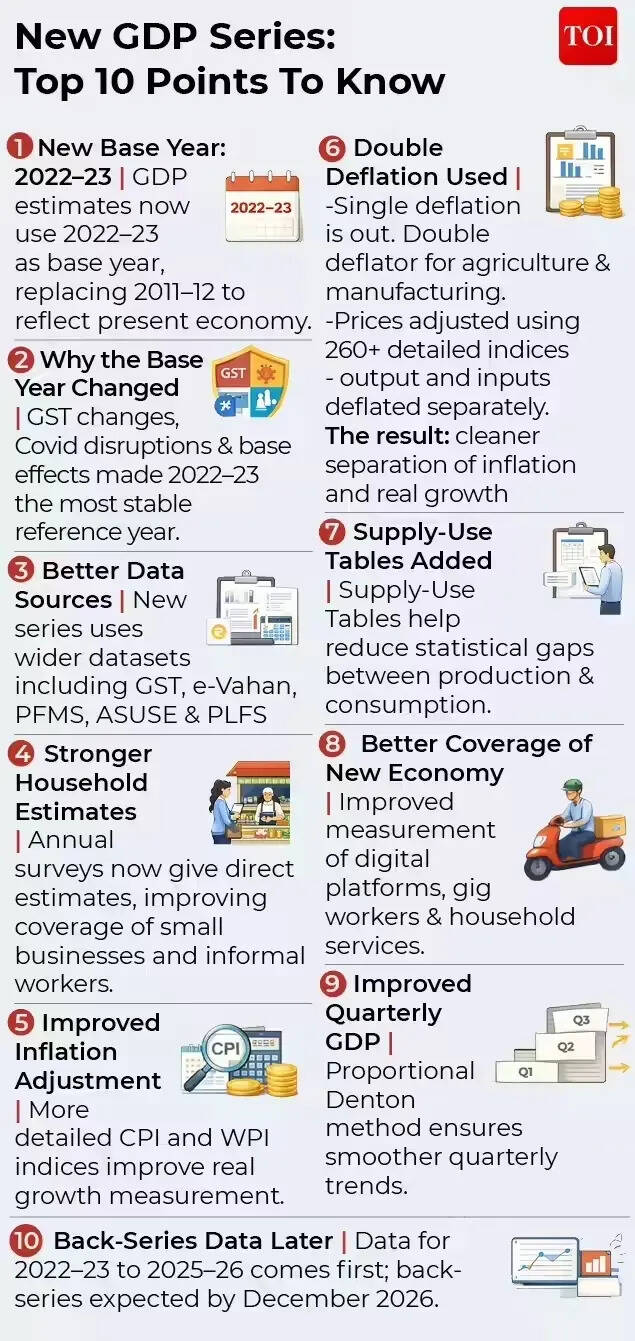

Rupee Depreciation Blow & New GDP Series

The first thing to understand is that IMF’s data on the size of a country’s nominal GDP is in dollar terms. Hence, with global rankings based on dollar‑denominated GDP, they are highly sensitive to exchange rate movements. The biggest party pooper for India’s dream of becoming the fourth largest has been the rupee’s slide. The Indian currency has depreciated more than expected over the last year, dropping from 84.57 versus the US dollar in 2024 to 88.48 in 2025, as per IMF data. The IMF estimates see it at 92.59 this year.Several factors have contributed to the rupee’s decline, including capital outflows, uncertainty related to India-US trade deal up until February, and the recent Middle East conflict which has raised crude oil prices and India’s import bill. Also, the RBI while actively managing volatility in the forex market, is not targeting any particular level of the rupee.Arun Singh, Chief Economist, Dun & Bradstreet India says that India’s recent slip to sixth place in global GDP rankings does not reflect a weakening of the economy, but is largely the result of currency conversion effects and a one‑time statistical revision.The rupee’s depreciation from 2024 to 2026, has mechanically compressed India’s GDP in dollar terms, effectively halving apparent growth despite strong domestic expansion, says Arun Singh.According to Ranen Banerjee, Partner and Leader, Economic Advisory Services, PwC India, GDP in US dollar terms would shave off with rupee depreciation. “We have had almost 7-8% depreciation over the last few months owing to the conflict and portfolio outflows. Thus, in effect in US dollar terms, it is close to shaving out almost a year’s nominal GDP,” he tells TOI.And it’s not just about the Indian economy. The United Kingdom which has overtaken India to bag the 5th spot again also has economic factors working in its favour. UK’s GDP growth at 0.5% has recently beaten forecasts of 0.1% by a wide margin. Not only that, its currency – pound – has actually appreciated against the US dollar.The second factor that has impacted the rankings is India’s adoption of a new base year for its latest GDP series. As per the new data, which also makes use of a more refined methodology, the size of India’s nominal GDP in rupee terms has gone down. Sample this: As per the older base year of 2011-12, India’s GDP at the end of 2025-26 would have been Rs 35,713,886 crore. But under the new series, it is estimated to be Rs 34,547,157 crore. The new calculation methodology and base year revision presents a more accurate picture of the size of the Indian economy.Hence the currency effect has been compounded by a one‑time downward revision following India’s shift to a new GDP base year, which has lowered reported nominal levels without affecting real activity.

Does India’s drop to 6th indicate fundamental weakness?

Experts are confident that India’s growth story is intact and fundamentally strong, a fact that is reflected in projections of it continuing to be the world’s fastest growing major economy. They see technical factors behind the current slip, rather than any deterioration in economic fundamentals.It’s also interesting to note that while India will be the sixth largest economy in FY27, in the upcoming financial year, it is likely to overtake both the UK, and Japan to bag the fourth spot.Arun Singh of Dun & Bradstreet India explains this resilience with numbers:IMF World Economic Outlook (April 2026) data show that India’s GDP at current prices in domestic currency rose strongly from ₹318 trillion in 2024 to ₹346.5 trillion in 2025 and further to ₹384.5 trillion in 2026, translating into robust nominal growth of about 8.9% in 2024–25 and nearly 11% in 2025–26, among the fastest globally. In contrast, other large economies recorded more moderate domestic nominal growth – around 5% in the US, roughly 4% in China, 3–5% in the UK, 3–3.5% in Germany, and lower or volatile growth in Japan – underscoring India’s strong underlying momentum. In times of global economic turmoil, while GDP growth is expected to take some hit, most agencies and experts have pegged India’s growth to be strong. Incidentally, the IMF has even marginally raised its GDP growth forecast for FY27 to 6.5% despite the ongoing Middle East conflict.

“In India, growth for 2025 is revised upward by 1.0 percentage point relative to October, to 7.6 percent, reflecting the better-than-expected outturn in the second and third quarters of the fiscal year and sustained strong momentum in the fourth quarter,” IMF said in its latest outlook. “For 2026, growth is revised upward moderately by 0.3 percentage point (0.1 percentage point relative to January) to 6.5 percent, led by positive contributions from the carryover of the strong 2025 outturn and the decline in additional US tariffs on Indian goods from 50 to 10 percent, which outweigh the adverse impact of the Middle East conflict. Growth is projected to stay at 6.5 percent in 2027,” it added.

Will India become 3rd largest anytime soon?

The rupee depreciation and the nominal GDP revision has also pushed back India’s dream of becoming the third largest economy by the end of this decade. In the October 2025 estimates, IMF had said that India will overtake Germany to become third largest by FY30. However, the April 2026 projections see it reaching the third rank only by FY 2030-31.Experts point to the rupee’s depreciation versus the dollar to note that the road ahead is likely to be uncertain. Madan Sabnavis, Chief economist, Bank of Baroda is confident that India will continue to do well in the coming years.“We will definitely improve in terms of GDP growth which will be higher than that of other countries especially UK and Japan which are just above us. However, the rupee value will finally determine how India gets placed on the global scale,” he told TOI.Ranen Banerjee of PwC India sees rupee beginning to get support with the conflict containment, relatively lower oil prices and portfolio flow reversals with valuations getting attractive in recent times. “Thus, we should not be experiencing any further sharp depreciation of the rupee in the immediate term provided the conflict does not escalate and oil prices relatively softening from their highs and come down to a range of $85-90 a barrel,” he says.For Arun Singh of Dun & Bradstreet, looking ahead, India’s relative position in US dollar‑based GDP rankings will remain highly sensitive to currency movements rather than domestic growth dynamics. “Continued global dollar strength or capital‑flow volatility may cause periodic slippage in rankings despite robust fundamentals. Sustaining external macro stability and limiting undue rupee volatility will be crucial for India’s strong growth performance to translate more fully into higher global economic rankings,” Arun Singh told TOI.The Indian economy, largely driven by domestic fundamentals, is not immune to external shocks. High US tariffs of 50% from August 2025 to early February, and the ongoing US-Iran war have spelt back-to-back shocks for the economy. Even as experts stress on the resilience of the growth story, the vulnerability to higher crude oil prices, and other global supply chain disruptions is a reality. In such a scenario, India may well have to contend with fluctuating world rankings, while banking on its strong GDP growth to tide over disruptions.

new video loaded: Why Your Paycheck Feels Smaller

By Ben Casselman, Nour Idriss, Sutton Raphael and Stephanie Swart

April 18, 2026

Business

‘It’s just scale’: Local mom-and-pop car dealerships are growing or dying amid industry consolidation, rise of mega-retailers

Derek Sylvester with members of his family, team and mascot Molly, who was featured on the dealership’s logo.

Courtesy Sylvester Chevrolet

Derek Sylvester’s father built the family’s original Chevrolet dealership with his bare hands on Main Street in rural Peckville, Pennsylvania, in 1972.

The store and family have been a pillar of the village, outside Scranton, ever since. That was until late last month, when Sylvester and his family closed a deal to sell Sylvester Chevrolet to a New York-based dealer group.

“As a family, we decided this might be the time,” said Sylvester, who at 67 has been contemplating retirement. “Unless you’re a larger store, a much larger store, it’s a little bit harder to make money. … It’s just scale.”

Many of Sylvester’s family members plan to continue working at the dealership, but he said they didn’t feel they were in a position to continue running the business amid the rapidly changing automotive retail landscape in the U.S. The industry is facing a tumultuous adoption of all-electric vehicles, technological shifts such as artificial intelligence, and growing demands from automakers.

Sales of dealerships such as Sylvester Chevrolet are occurring across the country at a rapid pace as the business of selling cars, once considered the purview of mom-and-pop shops, has evolved into a lucrative trillion-dollar industry rife with consolidation that has drawn more notice from Wall Street and investors in recent years.

While the National Automobile Dealers Association, or NADA, reports that the vast majority of its U.S. franchised dealers are small business owners such as Sylvester who have fewer than six stores, the top retailers in the country have significantly grown.

The top 150 dealers sold 27% of all retail and fleet new vehicles in 2025, up from 24.3% in 2021 and 21.2% in 2015, according to Automotive News’ annual ranking of top automotive retailers. They also owned roughly a quarter of dealerships last year, up from less than 20% a decade ago, according to the trade publication.

Meanwhile, top publicly traded dealers such as Lithia Motors and AutoNation have ballooned to market caps of more than $6 billion each. Even online used-car retailer Carvana — and its $74 billion market cap, which surpasses the value of most car companies it sells vehicles from — has quietly started purchasing new vehicle franchises without disclosing its future plans.

“There’s a lot of money that wants to come to the industry,” Brian Gordon, president of dealer advisor and broker Dave Cantin Group, told CNBC. “And, generally, the industry is sort of aligned on how to value these things. That makes for a good climate for [mergers and acquisitions].”

Industry consolidation

Multibillion-dollar dealerships have been on the rise amid a decadeslong consolidation that has led to a grow-or-die mentality for many U.S. automotive retailers.

NADA, a trade association representing franchised dealers, reports the average dealership owner has between two and three stores, but the largest growth area over the past decade has been in medium-sized dealerships that own between six and 25 stores.

NADA reports 90.5% of its nearly 17,000 dealers own between one and five stores, down from 94.4% in 2016. Meanwhile, 0.2% of dealers own 50 stores or more, up from 0.1% during that time frame.

“It’s clear that it’s a consolidating industry, and it’s an industry that is going to continue to consolidate,” Gordon said. But, he added, that is happening at every level, especially the expansion of mom-and-pop shops to larger players.

Dave Cantin Group — the advisor for Matthews Auto Group, the dealer group that acquired Sylvester Chevrolet — conducts dozens of such deals a year and said it expects the pace of consolidation and mergers and acquisitions to continue to increase this year.

Matthews Auto Group is one of many regional dealership companies that has decided to expand. The family-owned company started in Vestal — in central New York, south of Syracuse — in 1973 with a single Chrysler-Plymouth store that has grown into a roughly $800 million business with 18 locations and 800 employees.

Rob Matthews, a second-generation owner and CEO of Matthews Auto Group, said the company’s decision to grow is ongoing and that it aims to be more profitable and better compete in its current markets of New York and Pennsylvania.

Matthews Auto Group CFO John Totolis (from left to right), Dave Cantin Group managing director Talon Fee, Sylvester Chevrolet President Derek Sylvester, partner Sylvester Chevrolet Neil Sylvester, Matthews Auto Group CEO Rob Matthews and Matthews Auto Group President Mark Gaeta outside Sylvester Chevrolet in Peckville, Pennsylvania

Courtesy image

“I think that’s certainly a competitive advantage. I think staying still is probably not the best play. You’re seeing continued scale,” Matthews said. “The trend is you’re just going to continue to see consolidation to allow you to stay competitive.”

That’s also why Sylvester said he wanted to sell his business, with stipulations about retaining the store’s dozens of employees — something that’s part of Matthews’ strategy when acquiring a store.

“There’s a lot of things that, because of our scale, we see we can really unlock a store like his,” Matthews said. “I think, honestly, it’s exciting in the sense that we’re just looking to give them more tools and hopefully let everyone work going forward.”

Growth of mega-dealers

Wall Street has taken notice of how lucrative and protected franchised dealerships are in the U.S. The franchised dealer system, which exists to sell new vehicles to consumers rather than automakers selling their vehicles themselves, is unique and heavily regulated.

“I think there’s endless upside. The opportunity for growth in our company is just endless,” Sonic Automotive President Jeff Dyke told CNBC during a recent interview. “I think having mom-and-pop dealers is really good for the business. The thing is, the mom-and-pop dealer is going to have to advance their thinking.”

Sonic Automotive, a publicly traded company with a market cap of more than $2 billion, has grown from 96 franchised dealership stores in 2015 to 134 to end last year. It’s also gone through a massive expansion of its EchoPark used vehicle stores and Sonic Powersports. The company’s revenue during that time jumped 58% to $15.2 billion last year.

Dealership stocks

Others, such as Lithia Motors, have been even more aggressive in growth. The Medford, Oregon-based company surpassed longstanding dealership group AutoNation to become the top U.S. new vehicle franchised dealer in 2022.

Lithia, with a $6.3 billion market cap, has executed an audacious growth plan, from $8.7 billion in revenue in 2016 to $37.6 billion last year. The company nearly tripled its new and used stores from 154 locations to 455 stores during that time frame.

John Murphy, a longtime automotive analyst who is a managing director of strategic advisory at buy-sell advisory firm Haig Partners, said he believes that dealerships remain an extremely lucrative market for investors, despite things settling down somewhat after companies saw inflated profits during the Covid pandemic.

“Structurally, there’s some real potential upside, and there is an increasing level of attention by existing capital in the dealership community as it stands right now from outside players, private equity family offices, other pools of capital on this limited number of dealers and finite number of dealers,” he said. “The earnings upside is increasing and there’s increasing attention, or demand, on the buy side of the equation.”

Mom-and-pops remain

All of that combines to make many mom-and-pop dealerships ripe for acquisition or expansion.

“There’s just so many factors that make competition for a small mom-and-pop dealership more difficult,” said Talon Fee, a managing director at Dave Cantin Group who led the sale of Sylvester Chevrolet to Matthews Auto Group. “It’s not to say that small mom-and-pop dealerships can’t continue to exist and thrive and survive, but they do need to have a plan.”

Fee and others said the top reasons for owners to sell are a lack of succession planning, a growing competitive and changing industry, and a lack of commitment to reinvest in the businesses.

“There’s a lot of outside capital that’s figured out how to come in, given the fact that you have to be an operator in order to get approved by a manufacturer,” said Gordon, of Dave Cantin Group.

But the industry is changing in other ways, as new automakers such as Tesla, Rivian and Lucid try to bypass the franchised dealer model and sell vehicles directly to consumers.

Such companies have continuously fought state laws to allow such sales, with Rivian recently winning a battle with car dealers in Washington state by threatening to take its case to voters with a ballot measure to permit direct sales.

It adds to the evolving U.S. automotive retail landscape that owners such as Sylvester and his wife, who also worked at the dealership, haven’t had to deal with in the past. It’s also something Sylvester and many other smaller mom-and-pop stores won’t have to compete with once they sell their businesses.

“I lived a great life, don’t get me wrong. But, hey, good things come to an end,” said Sylvester, who plans to spend retirement caring for a 92-acre farm in Pennsylvania. “We made a good living. You know, we helped the community out.”

Explained: On way to 4th largest, how India slipped to 6th rank & what it means for 3rd largest economy dream – The Times of India

Saturday Sessions: The Lone Bellow performs "You Were Leaving"

Video: Why Your Paycheck Feels Smaller

-

Politics1 week ago

Politics1 week agoIndian airlines hit hardest after Dubai limits foreign flights until May 31

-

Entertainment5 days ago

Entertainment5 days agoPalace left in shock as Prince William cancels grand ceremony

-

Politics1 week ago

Politics1 week agoChinese, Taiwanese will unite, Xi tells Taiwan opposition leader

-

Sports5 days ago

Sports5 days agoThe case for Man United’s Fernandes as Premier League’s best

-

Business5 days ago

Business5 days agoUK could adopt EU single market rules under new legislation

-

Entertainment1 week ago

Entertainment1 week agoDua Lipa hits major career high ahead of wedding with Callum Turner

-

Business1 week ago

Business1 week agoThe FAA wants gamers to apply for air traffic control jobs

-

Sports1 week ago

Sports1 week agoLamar Jackson hits back at critics with faithful message on social media