Business

JPMorgan’s looming question: What happens when CEO Jamie Dimon leaves?

As Wall Street’s top bankers huddled in New York last month, preparing to convince Elon Musk’s SpaceX that they should be chosen to lead its upcoming IPO, one firm wasn’t letting its star advisor miss the bake-off.

Among the squad of JPMorgan Chase investment bankers flying 2,500 miles west to California to pitch SpaceX was the lender’s boss, billionaire CEO Jamie Dimon, people with knowledge of the trip told CNBC.

The morning after that pitch meeting, on Dec. 19, Dimon was already back in his customary early Friday perch: sitting in his bank’s New York lobby, taking meetings in full view of the thousands of employees streaming through the building’s turnstiles.

The whirlwind few days highlight the reality of Dimon’s singular impact on JPMorgan, the world’s largest bank by market capitalization.

Dimon marks his 20th anniversary as CEO this month and remains deeply involved across the sprawling businesses of JPMorgan, a giant across Wall Street and Main Street with $4.6 trillion in assets. Half a dozen executives across investment banking, asset management and consumer banking echoed that view.

Which makes the inevitable questions surrounding Dimon’s tenure loom large as he approaches 70 years of age. Dimon has for years maintained, somewhat tongue-in-cheek, that his retirement was perpetually 5 years away. In 2024, for the first time, he acknowledged that window was shrinking.

Will JPMorgan’s era of dominance be over when Dimon exits as CEO?

“Given his track record, anybody else would be a downgrade,” said Ben Mackovak, a bank board member and investor through his firm Strategic Value Bank Partners.

“I’m sure somebody else could grow into the role and surprise people,” Mackovak said. “But on day one, no one is going to be as qualified to run that bank as Jamie.”

Jamie Dimon, Chairman and Chief Executive Officer of JPMorgan Chase & Co., attends the ribbon-cutting ceremony opening the firm’s new headquarters at 270 Park Avenue, in New York City, U.S., October 21, 2025.

Eduardo Munoz | Reuters

In two decades, Dimon took a middle-of-the-pack American lender and, with his unique combination of judgment, paranoia, attention to detail and scope of vision, created a juggernaut of finance that the world hadn’t seen before.

During calm times, he invested aggressively for the future, and during periods of tumult, like 2008 and 2023, he avoided pitfalls that consumed other banks, allowing him to snap up three failed institutions.

Over the past 20 years, the bank’s annual net income soared more than 500% to $58.5 billion in 2024. The firm reports full-year 2025 results on Tuesday.

Now, at a market cap of roughly $900 billion, JPMorgan is worth nearly as much as the next three largest U.S. banks combined: Bank of America, Citigroup and Wells Fargo.

Besides running JPMorgan, Dimon has taken on an outsized role in global finance as a top voice explaining market gyrations or emerging risks and influencing regulators amid policy shifts. It was Dimon’s recession warning on a Fox News segment in April that helped convince President Donald Trump to pivot on his trade policy, igniting a historic relief rally.

“It’s just the aura he has, the credibility that he’s built up in the markets,” said Fitch Ratings analyst Chris Wolfe. “The minute you step out of that role, it’s not like you can just hand that over, your successor doesn’t automatically inherit that. I think that’s the real challenge.”

Potential successors

The question of who could take over for Dimon — who was already a cancer survivor when he nearly died in 2020 from a ruptured aorta — has been openly discussed among investors for more than a decade.

To investors, his most likely successor is currently Marianne Lake, head of the firm’s giant consumer bank and former CFO of the company, followed by Doug Petno and Troy Rohrbaugh, the co-heads of the firm’s commercial and investment bank.

Marianne Lake, chief financial officer of JPMorgan Chase & Co.

Jin Lee | Bloomberg | Getty Images

Other contenders include asset and wealth management head Mary Erdoes and CFO Jeremy Barnum.

“If investors were to do a straw poll today, they’d probably pick Marianne,” said Truist bank analyst Brian Foran.

“The running joke is that she’s a human supercomputer when it comes to banking,” Foran said. “Really, the only question mark people have about her is, she’s so analytical, can she do the kind of ‘rah-rah’ stuff to inspire the sales force?”

Wells Fargo banking analyst Mike Mayo hypothesized that JPMorgan stock could immediately drop 5% if Dimon were to suddenly exit, regardless of the named replacement. (The bank has said Dimon would serve as chairman even after relinquishing the CEO role.)

It’s a somewhat common occurrence on Wall Street for companies with iconic CEOs: The stock premium shrinks, at least for a period, when their longtime leaders announce their departures. For instance, Berkshire Hathaway shares trailed the S&P 500 last year after Warren Buffett said he was stepping down as CEO.

‘Never going to quit’

When asked about CEO succession, JPMorgan executives say that Dimon is as plugged in as ever, and unlikely to step down soon.

Depending on how long he sticks around, that means it’s not necessarily his current direct reports like Lake, Petno and Rohrbaugh who are in line, but more junior executives now being groomed and evaluated for leadership roles, they told CNBC.

“There’s a lot of work going into imagining that day without him,” said a JPMorgan executive who asked not to be named speaking about his boss. “If he stays until he’s 85, it’s not his direct reports that are going to be next in line, its maybe one or two levels down from today.”

“Does he leave a huge vacuum? Yes,” said the executive. “It’s not fatal, though, because we’ve been planning for it. I think there’s combinations of people that together can create the same outcome.”

The CEO of a commercial bank and former JPMorgan executive, who described Dimon as a mentor, also said he didn’t think Dimon would step down soon.

“Jamie’s never going to quit,” said the CEO, who asked for anonymity to speak candidly. “What else would he do where he’s as important as he is now? His friends are all people from work. He loves it.”

Still, beyond the day-to-day management of a company with 318,000 employees, Dimon seems intent on setting up JPMorgan for a future without him.

Legacy values

In recent months, Dimon oversaw the completion of the bank’s new $3 billion headquarters in midtown Manhattan and announced a $1.5 trillion initiative to bolster industries crucial to U.S. interests.

And, perhaps most crucially, he continues to instill his values into the firm’s management team.

Last year, at a conference for JPMorgan’s top 400 executives, Dimon rattled off a list of once-great companies that died though mismanagement. Finance is especially prone to this threat, because of the temptation to manipulate numbers for short-term gain, he said.

“Travelers blew up. Citi blew up, twice. Bear Stearns failed, Lehman failed, I’m here because Bank One screwed up a bunch of businesses,” Dimon said, referring to a predecessor firm to JPMorgan.

“If you look at these things, it’s complacency, it’s bureaucracy, it’s arrogance. A lot of it is dishonest numbers. Failure to set standards,” Dimon said. “These are the cancers that kill companies.”

Nobody knows when Dimon’s last day as CEO will come, except to know that it is approaching. After adjusting his standard 5-year retirement answer to hint at a sooner departure, Dimon hasn’t advanced that clock any further.

“As great as he is, he can’t do this forever,” said Barclays banking analyst Jason Goldberg. “Every day that passes, you’re a day closer to the end.”

— CNBC’s Gabriel Cortes contributed to this report.

Business

NaBFID signs pact with PDCOR to expand advisory support for state projects – The Times of India

The National Bank for Financing Infrastructure and Development (NaBFID) has signed a Memorandum of Agreement with Projects Development Company of Rajasthan Limited (PDCOR) to strengthen advisory services for state and city-level infrastructure projects.The agreement will also allow both institutions to jointly explore financing and transaction advisory opportunities, including transaction structuring, commercial and technical due diligence, and support for financial closure of projects undertaken by state governments and urban local bodies across India, according to PTI.“This collaboration seeks to enhance access to long-term institutional finance for State Governments and Urban Local Bodies, while strengthening the infrastructure advisory and financing ecosystem,” Rajkiran Rai G., Managing Director of NaBFID, said.He added that the partnership would help both institutions jointly pursue project advisory opportunities, develop replicable financing frameworks, accelerate financial closures and mobilise capital across the infrastructure value chain.Monika Kalia, DMD-CFO, NaBFID, said the tie-up would leverage the strengths of both organisations to provide much-needed advisory support to states and urban local bodies for impactful urban infrastructure projects.Dileep Chingapurath, Chief Executive Officer, PDCOR, said the agreement would address the long-felt need for end-to-end professional support to structure and mobilise sustainable financing solutions, particularly for state governments and their agencies.“Through this collaboration, both institutions aim to enhance the quality of project preparation, mobilise institutional capital more effectively and accelerate the implementation of sustainable infrastructure projects across states and municipalities,” he said.NaBFID is a Development Financial Institution focused on long-term infrastructure financing, while PDCOR is an undertaking of the Government of Rajasthan.

Business

Explained: On way to 4th largest, how India slipped to 6th rank & what it means for 3rd largest economy dream – The Times of India

In April 2025 when the International Monetary Fund (IMF) released its World Economic Outlook, India was seen overtaking Japan to become the world’s fourth largest economy by the end of 2025-26. One year later, India has slipped to the sixth position on the largest economies rankings, with the United Kingdom reclaiming its spot as the fifth largest economy.In fact, IMF’s latest World Economic Outlook (April 2026) sees India sitting at the sixth spot this financial year too. This projection comes even as India has grown better than expected in FY26 and is seen retaining its tag of being the world’s fastest growing major economy.What has led to the sudden fall? Why has India dropped to the sixth position, falling behind the UK, instead of overtaking Japan to become the fourth largest economy? And what does this setback mean for its dream of becoming the third largest economy by the end of this decade? We decode:

Data drive: India projected as 4th largest, but fell to 6th spot

First let’s look at some IMF data to see which way the Indian economy was headed in April 2025, and what the April 2026 outlook data suggestsAs per April 2025 estimates of IMF, India’s economy would have been at $4601.225 billion at the end of FY 2025-26, overtaking Japan which was estimated at $4373.091 billion. The UK at the 6th spot was projected to have a nominal GDP of $4040.844 billion.However, as per the April 2026 estimates, India’s economy had a nominal GDP of $4,153 billion at the end of FY 2025-26, with the UK overtaking it with $4,265 billion GDP. Japan’s GDP is seen at $4,379 billion.As the above estimates show, India’s GDP estimates have seen a drop over one year, while UK’s nominal GDP has grown better than expected. Japan has been steady.So, what went wrong? Blame the rupee and GDP data itself!

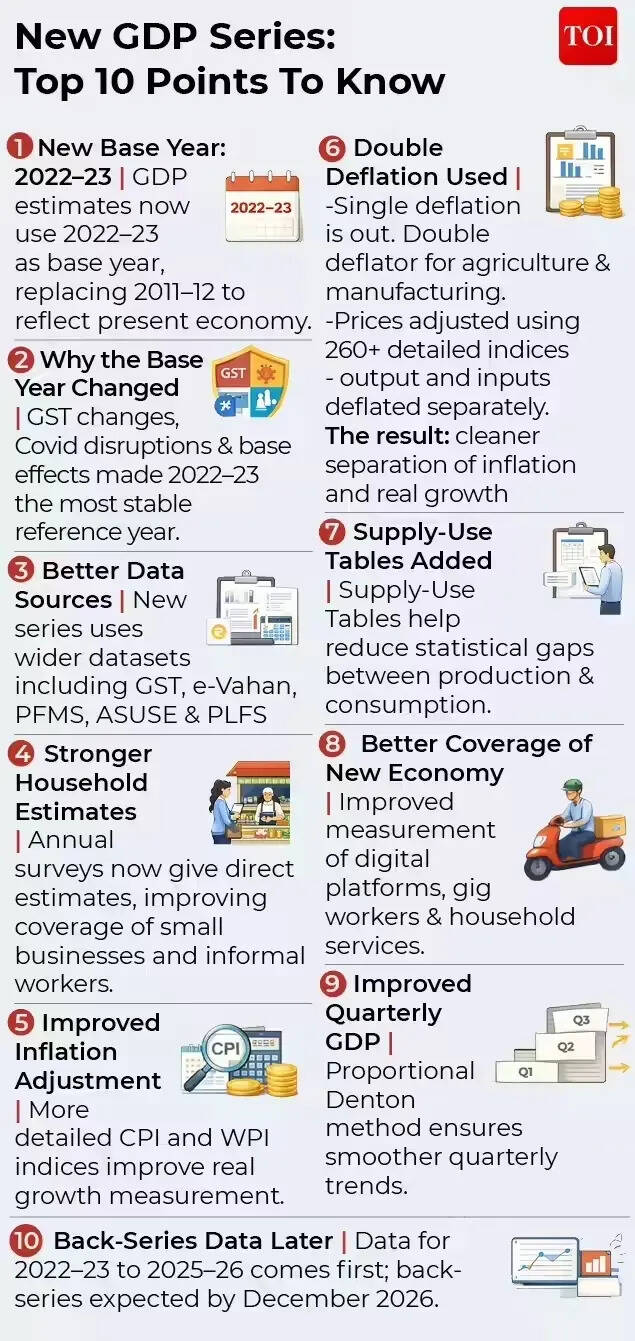

Rupee Depreciation Blow & New GDP Series

The first thing to understand is that IMF’s data on the size of a country’s nominal GDP is in dollar terms. Hence, with global rankings based on dollar‑denominated GDP, they are highly sensitive to exchange rate movements. The biggest party pooper for India’s dream of becoming the fourth largest has been the rupee’s slide. The Indian currency has depreciated more than expected over the last year, dropping from 84.57 versus the US dollar in 2024 to 88.48 in 2025, as per IMF data. The IMF estimates see it at 92.59 this year.Several factors have contributed to the rupee’s decline, including capital outflows, uncertainty related to India-US trade deal up until February, and the recent Middle East conflict which has raised crude oil prices and India’s import bill. Also, the RBI while actively managing volatility in the forex market, is not targeting any particular level of the rupee.Arun Singh, Chief Economist, Dun & Bradstreet India says that India’s recent slip to sixth place in global GDP rankings does not reflect a weakening of the economy, but is largely the result of currency conversion effects and a one‑time statistical revision.The rupee’s depreciation from 2024 to 2026, has mechanically compressed India’s GDP in dollar terms, effectively halving apparent growth despite strong domestic expansion, says Arun Singh.According to Ranen Banerjee, Partner and Leader, Economic Advisory Services, PwC India, GDP in US dollar terms would shave off with rupee depreciation. “We have had almost 7-8% depreciation over the last few months owing to the conflict and portfolio outflows. Thus, in effect in US dollar terms, it is close to shaving out almost a year’s nominal GDP,” he tells TOI.And it’s not just about the Indian economy. The United Kingdom which has overtaken India to bag the 5th spot again also has economic factors working in its favour. UK’s GDP growth at 0.5% has recently beaten forecasts of 0.1% by a wide margin. Not only that, its currency – pound – has actually appreciated against the US dollar.The second factor that has impacted the rankings is India’s adoption of a new base year for its latest GDP series. As per the new data, which also makes use of a more refined methodology, the size of India’s nominal GDP in rupee terms has gone down. Sample this: As per the older base year of 2011-12, India’s GDP at the end of 2025-26 would have been Rs 35,713,886 crore. But under the new series, it is estimated to be Rs 34,547,157 crore. The new calculation methodology and base year revision presents a more accurate picture of the size of the Indian economy.Hence the currency effect has been compounded by a one‑time downward revision following India’s shift to a new GDP base year, which has lowered reported nominal levels without affecting real activity.

Does India’s drop to 6th indicate fundamental weakness?

Experts are confident that India’s growth story is intact and fundamentally strong, a fact that is reflected in projections of it continuing to be the world’s fastest growing major economy. They see technical factors behind the current slip, rather than any deterioration in economic fundamentals.It’s also interesting to note that while India will be the sixth largest economy in FY27, in the upcoming financial year, it is likely to overtake both the UK, and Japan to bag the fourth spot.Arun Singh of Dun & Bradstreet India explains this resilience with numbers:IMF World Economic Outlook (April 2026) data show that India’s GDP at current prices in domestic currency rose strongly from ₹318 trillion in 2024 to ₹346.5 trillion in 2025 and further to ₹384.5 trillion in 2026, translating into robust nominal growth of about 8.9% in 2024–25 and nearly 11% in 2025–26, among the fastest globally. In contrast, other large economies recorded more moderate domestic nominal growth – around 5% in the US, roughly 4% in China, 3–5% in the UK, 3–3.5% in Germany, and lower or volatile growth in Japan – underscoring India’s strong underlying momentum. In times of global economic turmoil, while GDP growth is expected to take some hit, most agencies and experts have pegged India’s growth to be strong. Incidentally, the IMF has even marginally raised its GDP growth forecast for FY27 to 6.5% despite the ongoing Middle East conflict.

“In India, growth for 2025 is revised upward by 1.0 percentage point relative to October, to 7.6 percent, reflecting the better-than-expected outturn in the second and third quarters of the fiscal year and sustained strong momentum in the fourth quarter,” IMF said in its latest outlook. “For 2026, growth is revised upward moderately by 0.3 percentage point (0.1 percentage point relative to January) to 6.5 percent, led by positive contributions from the carryover of the strong 2025 outturn and the decline in additional US tariffs on Indian goods from 50 to 10 percent, which outweigh the adverse impact of the Middle East conflict. Growth is projected to stay at 6.5 percent in 2027,” it added.

Will India become 3rd largest anytime soon?

The rupee depreciation and the nominal GDP revision has also pushed back India’s dream of becoming the third largest economy by the end of this decade. In the October 2025 estimates, IMF had said that India will overtake Germany to become third largest by FY30. However, the April 2026 projections see it reaching the third rank only by FY 2030-31.Experts point to the rupee’s depreciation versus the dollar to note that the road ahead is likely to be uncertain. Madan Sabnavis, Chief economist, Bank of Baroda is confident that India will continue to do well in the coming years.“We will definitely improve in terms of GDP growth which will be higher than that of other countries especially UK and Japan which are just above us. However, the rupee value will finally determine how India gets placed on the global scale,” he told TOI.Ranen Banerjee of PwC India sees rupee beginning to get support with the conflict containment, relatively lower oil prices and portfolio flow reversals with valuations getting attractive in recent times. “Thus, we should not be experiencing any further sharp depreciation of the rupee in the immediate term provided the conflict does not escalate and oil prices relatively softening from their highs and come down to a range of $85-90 a barrel,” he says.For Arun Singh of Dun & Bradstreet, looking ahead, India’s relative position in US dollar‑based GDP rankings will remain highly sensitive to currency movements rather than domestic growth dynamics. “Continued global dollar strength or capital‑flow volatility may cause periodic slippage in rankings despite robust fundamentals. Sustaining external macro stability and limiting undue rupee volatility will be crucial for India’s strong growth performance to translate more fully into higher global economic rankings,” Arun Singh told TOI.The Indian economy, largely driven by domestic fundamentals, is not immune to external shocks. High US tariffs of 50% from August 2025 to early February, and the ongoing US-Iran war have spelt back-to-back shocks for the economy. Even as experts stress on the resilience of the growth story, the vulnerability to higher crude oil prices, and other global supply chain disruptions is a reality. In such a scenario, India may well have to contend with fluctuating world rankings, while banking on its strong GDP growth to tide over disruptions.

new video loaded: Why Your Paycheck Feels Smaller

By Ben Casselman, Nour Idriss, Sutton Raphael and Stephanie Swart

April 18, 2026

Everything to know about venue, guest list, dress, more

Secretary Doug Burgum expects Teddy Roosevelt’s induction into Pro Football Hall of Fame: report

Ariana Grande teases new era after ‘Eternal Sunshine’ with cryptic video

-

Politics1 week ago

Politics1 week agoIndian airlines hit hardest after Dubai limits foreign flights until May 31

-

Entertainment6 days ago

Entertainment6 days agoPalace left in shock as Prince William cancels grand ceremony

-

Sports5 days ago

Sports5 days agoThe case for Man United’s Fernandes as Premier League’s best

-

Politics1 week ago

Politics1 week agoChinese, Taiwanese will unite, Xi tells Taiwan opposition leader

-

Business5 days ago

Business5 days agoUK could adopt EU single market rules under new legislation

-

Entertainment1 week ago

Entertainment1 week agoDua Lipa hits major career high ahead of wedding with Callum Turner

-

Business1 week ago

Business1 week agoThe FAA wants gamers to apply for air traffic control jobs

-

Sports1 week ago

Sports1 week agoLamar Jackson hits back at critics with faithful message on social media