Business

Are UK interest rates expected to fall again?

Kevin PeacheyCost of living correspondent

Getty Images

Getty ImagesThe Bank of England has cut interest rates from 4% to 3.75%, the lowest level since February 2023.

Analysts are divided about whether the Bank will cut again when it next meets in February.

Interest rates affect mortgage, credit card and savings rates for millions of people.

What are interest rates and why do they change?

An interest rate tells you how much it costs to borrow money, or the reward for saving it.

The Bank of England’s base rate is what it charges other banks and building societies to borrow money, which influences what they charge their own customers for mortgages as well as the interest rate they pay on savings.

The Bank moves interest rates up and down in order to keep UK inflation – the rate at which prices are increasing – at or near 2%.

When inflation is above that target, the Bank typically puts rates up. The idea is that this encourages people to spend less, reducing demand for goods and services and limiting price rises.

What has been happening to UK interest rates and inflation?

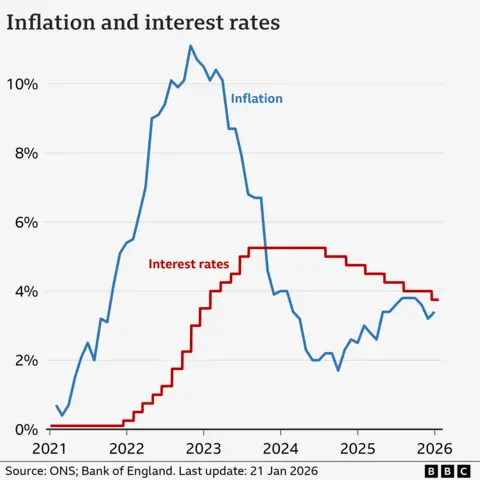

The main inflation measure, CPI, has dropped significantly since the high of 11.1% recorded in October 2022.

However, it was 3.4% in the year to December 2025 – up from 3.2% in November, and slightly higher than analysts had expected.

The Office for National Statistics (ONS) – which measures inflation – said the increase was driven by higher tobacco prices and the cost of airfares over the Christmas and New Year period.

The Bank of England’s base rate reached a recent high of 5.25% in 2023. It remained at that level until August 2024, when the Bank started cutting.

Five cuts brought rates down to 4%, before the Bank held rates at its meetings in September and November 2025 before the December cut.

Are interest rates expected to fall again?

Most analysts had expected the December cut, but the vote among members of the nine-member monetary policy committee (MPC) was divided, with only five in favour.

The Bank said rates were likely to continue dropping in the future, but warned decisions on further cuts in 2026 would be contested.

“We still think rates are on a gradual path downward but with every cut we make, how much further we go becomes a closer call,” said the Bank’s governor Andrew Bailey.

If inflation continues to rise – or just fails to fall – further rate cuts are less likely.

Mr Bailey has also repeatedly warned about the continuing impact of US tariffs, and political uncertainty around the world.

The next interest rate decision is on Thursday 5 February.

How do interest rate cuts affect mortgages, loans and savings rates?

Getty Images

Getty ImagesMortgages

Just under a third of households have a mortgage, according to the government’s English Housing Survey.

About 500,000 homeowners have a mortgage that “tracks” the Bank of England’s rate. A 0.25 percentage point cut is likely to mean a reduction of £29 in the monthly repayments for the average outstanding loan.

For the additional 500,000 homeowners on standard variable (SVR) rates – assuming their lender passed on the benchmark rate cut – there would typically be a £14 a month fall in monthly payments for the average outstanding loan.

But the vast majority of mortgage customers have fixed-rate deals. While their monthly payments aren’t immediately affected by a rate change, future deals are.

Mortgage rates have been falling recently, partly owing to the expectation the Bank would cut rates in December.

As of 21 January, the average two-year fixed residential mortgage rate was 4.77%, according to financial information company Moneyfacts. A five-year rate was 4.87%.

The average two-year tracker rate was 4.41%.

About 800,000 fixed-rate mortgages with an interest rate of 3% or below are expected to expire every year, on average, until the end of 2027. Borrowing costs for customers coming off those deals are expected to rise sharply.

Mortgage calculator

You can see how your mortgage may be affected by future interest rate changes by using our calculator:

Credit cards and loans

Bank of England interest rates also influence the amount charged on credit cards, bank loans and car loans.

Lenders can decide to reduce their own interest rates if Bank cuts make borrowing costs cheaper.

However, this tends to happen very slowly.

Getty Images

Getty ImagesSavings

The Bank base rate also affects how much savers earn on their money.

A falling base rate is likely to mean a reduction in the returns offered to savers by banks and building societies.

The current average rate for an easy access savings account is 2.45%, according to Moneyfacts.

Any further cut in rates could particularly affect those who rely on the interest from their savings to top up their income.

What is happening to interest rates in other countries?

In recent years, the UK has had one of the highest interest rates in the G7 – the group representing the world’s seven largest so-called “advanced” economies.

In June 2024, the European Central Bank (ECB) started to cut its main interest rate for the eurozone from an all-time high of 4%.

At its meeting in June 2025 the ECB cut rates by 0.25 percentage points to 2% where they have remained.

The US central bank – the Federal Reserve – has cut interest rates three times since September 2025, taking them to the current range of 3.5% to 3.75%, the lowest since 2022.

President Trump had repeatedly attacked the Fed for not cutting earlier.

Mumbai: Warburg Pincus-backed housing finance company Truhome Finance ( formerly Shriram Housing) has filed draft papers with capital markets regulator SEBI to raise Rs 3,000 crore through an initial public offering.The IPO will comprise a fresh issue of equity shares of face value Rs 10 aggregating up to Rs 1,500 crore and an offer for sale of equity shares of face value Rs 10 aggregating up to Rs 1,500 crore, according to the draft red herring prospectus filed with SEBI. The offer for sale will be undertaken by promoter selling shareholder Mango Crest Investment, which plans to offload shares worth up to Rs 1,500 crore.Truhome Finance plans to use the net proceeds from the fresh issue to augment its capital base to support future capital requirements, including onward lending and general corporate purposes. The funds will also help the company comply with RBI’s capital adequacy norms as its business expands.The company said the proceeds are expected to be deployed over the financial years ending March 31, 2027 and March 31, 2028.JM Financial, IIFL Capital Services, Jefferies India and Kotak Mahindra Capital Company are the book running lead managers to the issue.Warburg Pincus completed its acquisition of Shriram Housing Finance (SHFL) from Shriram Finance and other sellers in December 2024 for approximately Rs 4,630 crore, marking a strategic shift in India’s housing finance sector.

Business

Ticketmaster parent Live Nation reaches settlement with Department of Justice over antitrust concerns

Signs are seen at the Live Nation NYC headquarters on May 23, 2024 in New York City.

Michael M. Santiago | Getty Images

Live Nation Entertainment has reached a settlement with the Department of Justice over antitrust concerns surrounding its Ticketmaster platform, a senior DOJ official said Monday.

The settlement would see Ticketmaster unwind some of its exclusivity agreements with musical artists and open up the ticketing industry to greater competition. It still needs approval by more than 20 states that had filed suit and by the court.

As part of the settlement, Ticketmaster will offer a standalone third-party ticketing system for other companies like SeatGeek to use its technology. Live Nation has also agreed to divest at least 13 of its amphitheaters and will no longer be able to require artists to use other Live Nation products tied to its venues. It has also agreed to pay roughly $280 million in civil penalties.

Shares of Live Nation rose 5% in morning trading. Live Nation and Ticketmaster did not immediately respond to requests for comment.

Ticketmaster has long faced criticism that its dominance in the live events and ticketing space pushes up prices for consumers. The company has come under heightened scrutiny in recent years from fans who argue that it’s become harder and pricier to snag coveted event tickets.

In 2022, the backlash boiled over when the rollout of tickets for Taylor Swift’s Eras Tour was mishandled, leading to a probe of the company. And in 2024, the DOJ — along with more than two dozen states — sued to break up Live Nation and Ticketmaster, which merged in 2010.

In September, Live Nation was separately sued by the Federal Trade Commission over what the agency called “illegal” ticket resale tactics. The FTC said Ticketmaster controls roughly 80% of major concert venues’ ticketing.

In a Monday statement, New York Attorney General Letitia James said her office would continue to fight against Live Nation’s alleged monopoly even after its agreement with the DOJ.

“The settlement recently announced with the U.S. Department of Justice fails to address the monopoly at the center of this case, and would benefit Live Nation at the expense of consumers. We cannot agree to it,” said James, who is joined by the attorneys general of more than 20 other states.

The conflict in the Middle East could raise the cost of petrol, household energy bills and even food.

Source link

Adidas salutes USMNT’s 1994 World Cup run with denim jersey

Oil surges past $100 a barrel as stocks tumble amid US-Israeli aggression against Iran

Espresso Machines Are Like Guitars: The Rich Don’t Win

-

Politics2 days ago

Politics2 days agoIndia let Iran warship dock the day US sank another off Sri Lanka, say officials

-

Sports3 days ago

Sports3 days agoPakistan set for FIH Pro League debut | The Express Tribune

-

Sports1 week ago

Sports1 week agoCollege basketball star suspended by team for spitting toward opposing fan

-

Entertainment1 week ago

Entertainment1 week agoAl Jazeera broadcast interrupted by emergency missile alert in Qatar

-

Entertainment2 days ago

Entertainment2 days agoHarry Styles kicks off new era with ‘One Night Only’ comeback show

-

Business1 week ago

Business1 week agoLabour parliamentarians urge UK Government to oppose Rosebank oil field

-

Sports1 week ago

Sports1 week agoMichigan loses L.J. Cason for rest of season with torn ACL

-

Business3 days ago

Business3 days agoHome heating oil: ‘Most of my pension has gone on home heating oil’