Business

Market watch: India’s equity valuations dip below long-term averages; but stay elevated versus peers – The Times of India

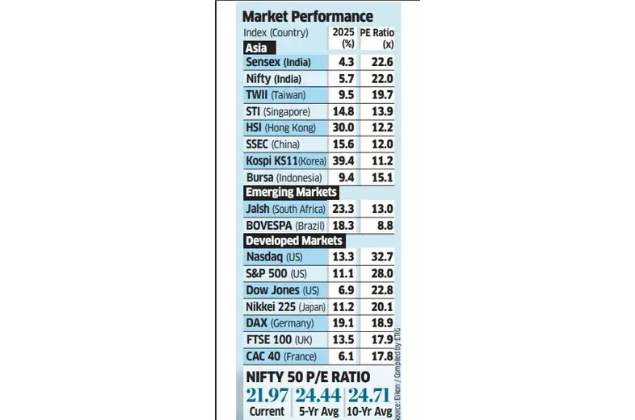

India’s equity valuations are trading marginally below their historical averages but continue to remain expensive compared with regional peers, raising concerns amid slowing earnings growth.The benchmark Nifty currently trades at a price-to-earnings (PE) ratio of 21.97 times, lower than its five- and 10-year averages of 24.4 and 24.8, respectively. In contrast, Hong Kong’s Hang Seng is at 11.7, South Korea’s Kospi below 13, and South Africa at around 12.7, according to an ET report.Valuations in India have traditionally traded at a premium to peers, supported by strong growth prospects. However, with corporate earnings momentum weakening, foreign investors are paring exposure and holding back fresh allocations.

“Valuations have begun mattering now because nominal GDP growth has slipped into single digits compared to around 12-13%,” said Ritesh Jain, founder of Pinetree Macro, a global macro asset allocation fund. “Corporate profitability is a function of nominal GDP. So, for an overseas fund manager looking at various markets, a country with slowing nominal growth and rich valuations is far less appealing despite its inherent strengths.”India is now the second-most expensive major market after the US, with some global fund managers increasingly shifting allocations to cheaper Chinese, European, and Japanese equities.Fund managers also noted that index composition plays a key role in valuation levels. “The composition of Indian indices must be taken into account while looking at valuations,” said Nilesh Shah, managing director, Kotak Mutual Fund. “If the Sensex and Nifty are full of expensive consumer names and there are fewer commodity players, it’s bound to push up valuation levels. If we were to remove some of the consumer names, our valuations are around averages on a historical basis.”

One day after a famous short-seller said Close Brothers has “systematically misrepresented” the extent of its exposure to the car loan mis-selling scandal, the merchant bank said it would axe 600 jobs as it looks to cut costs.

Yesterday shares in the finance house tumbled 14 per cent on Monday after Viceroy Research, which has previously called out Wirecard and Home Reit, said Close would have to at least double its provision for the scandal, which could end up costing the car loan sector £10 billion, watchdogs estimate.

Close expects to pay £300m for the car saga, which saw the commission paid to sales people not disclosed to consumers.

Lloyds Bank has the biggest exposure of any financial business, with much of the car trade also on the hook. Lloyds could end up paying out £2bn, though it has raised criticisms of how the regulator, the Financial Conduct Authority, is calculating payments.

The FCA said payouts are due on around 14 million unfair car finance deals, averaging at about £700 each, within a 360-page consultation document for its proposed redress scheme published last week.

Shares in Close were up slightly today at 360p.

The firm said the cuts – nearly a quarter of its 2,600-strong workforce – would be made over the next 18 months across its teams in the UK and Ireland.

It comes as part of plans to cut costs by about £25 million in its current year to the end of September, up from a £20 million previous target, and by around another £60 million in the next financial year, which is a year earlier than planned.

The cuts will come from actions including moves to outsource and offshore work, cut back its office network and roll out the use of artificial intelligence (AI) “at pace”.

Chief executive Mike Morgan said: “While the impact on affected colleagues is regrettable, these actions are necessary to structurally lower our cost base, while increasing our agility and ability to serve our customers.”

The note from Viceroy said: “We believe Close Brothers has systematically misrepresented its exposure to the Financial Conduct Authority’s forthcoming motor finance consumer redress scheme.”

Viceroy thinks Close could have to pay out between £572m and £1.23bn to compensate customers in all. At the higher end, that exceeds the entire market value of the company.

Close Brothers said it “strongly disagrees” with Viceroy’s conclusions. It added: “Our provisioning approach in relation to this matter is in accordance with UK-adopted international accounting standards and follows a robust governance process.”

Short-sellers such as Viceroy take a market position against shares, betting they will fall.

Close today which it reported a £65.5m loss for the six months to the end of January. It reported a £102.2m loss for the same period last year.

Additional reporting by PA

Business

LPG crisis hits restaurants: Staff face salary cuts, layoffs as eateries struggle to keep kitchens running – The Times of India

The Middle East crisis continues to boil and the ripples have triggered an operational stress for India’s food services sector. As LPG supply flows are disrupted amid the Strait of Hormuz transit issues, industry voices have warned of layoffs, salary cuts and widespread business impact if the situation drags on. Despite assurances from the government on boosting availability, restaurant owners and caterers have flagged that access to commercial LPG remains inconsistent, leaving many scrambling to keep operations afloat. Several described the situation as unpredictable, with little clarity on when normal supply will resume.Anjan Chatterjee, founder of Speciality Restaurants pointed to the growing distress across the sector. Highlighting the uncertainty of the situation, Chatterjee told ET that people are running from pillar to post. The founder further cautioned that the worst-hit would be workers at the lower end of the chain. “If restaurants and eateries are unable to do business, the first ones to get hit will be people down below.”

Impact on businesses, especially smaller players

Smaller restaurants, street-side eateries, caterers and cloud kitchens are the worst affected, with many already shutting or scaling down. Anjan Chatterjee of Speciality Restaurants described the chaos, saying people are running from pillar to post, and warned, “If restaurants and eateries are unable to do business, the first ones to get hit will be people down below.” He added, “While we hope supplies improve soon, currently, the situation is dynamic and we don’t know how things will pan out. At the ground level, particularly for local and street-side eateries, things are much worse.”Kirit Budhdev of the Federation of All India Caterers flagged worsening delays, “Suppliers are telling us to wait for 15 days. The on-ground situation is very challenging and it’s actually worsening for a lot of our members.”

Financial strain and risk of layoffs

The shortage is hitting profitability, menus and operating hours. Sagar Daryani of the National Restaurant Association of India said, “Smaller players which cannot bear the loss will see job cuts and the bigger players may bear the brunt for a while,” adding that multiple aspects of operations will be impacted.The strain is cascading to workers, especially those at the lower end. Aditya Narayan Mishra of CIEL HR explained, “For instance, if a restaurant has to close shop or run for fewer days in a week, they will not be employing helpers, local delivery boys, etc., who typically get paid Rs 500-700 daily. This segment, which accounts for the largest number of people employed, is already seeing an impact.”In Pune, Ganesh Shetty said, “Our members are still being told by agencies and suppliers that the supply is not for them but for other priority sectors like hospitals. Smaller restaurants have already shut down and they are not operational in Pune.Meanwhile, street food vendors in Madhya Pradesh are facing mounting pressure as a shortage of commercial gas cylinders disrupts operations, particularly for pani puri stalls and similar snack sellers. The impact is clearly visible across key markets such as Kolar, Jawahar Chowk and the BHEL area, where several carts remain closed or operate only during limited peak evening hours. Vendors who once catered to regular crowds are now struggling to secure enough fuel even for basic preparation.

Turning towards alternatives

Cloud kitchens are also under pressure, with FreshMenu’s Rashmi Daga noting, “At a central level, we are trying to move to firewood cooking, bring in induction, electric stoves, etc. But one can’t just move seamlessly to electric equipment given that summer months will also see power cuts.” At the same time in MP, two villages, Bandarkol in Jabalpur district and Baghuwar in neighbouring Narsinghpur, remain largely unaffected, with kitchen stoves continuing to run smoothly. In these villages, residents have turned to biogas instead of LPG cylinders. In Bandarkol, several households have installed small biogas plants that convert cattle dung into cooking fuel. Villagers say the system requires only a few minutes of daily effort while ensuring a steady supply of fuel for use throughout the day.

Uncertainty and outlook

Industry stakeholders say the situation remains volatile, with no clear timeline for recovery. While there has been slight easing compared to earlier days, supply gaps persist, and businesses continue to operate under uncertainty as they brace for prolonged disruption. Chatterjee added that while there is hope for improvement, conditions on the ground remain volatile. “While we hope supplies improve soon, currently, the situation is dynamic and we don’t know how things will pan out. At the ground level, particularly for local and street-side eateries, things are much worse,” he said. Speaking to ET, Rashmi Daga also highlighted the uncertainty ahead, saying, “One can’t even plan for perishables without knowing if gas is available the next day. Right now, the industry is bracing for 40-60 days of pain, but who knows, it could continue for months, too. If this happens, we will have no choice but to send some workers home.” The All Assam Restaurant Association (AARA) has called on the state government to urgently ensure a dedicated supply of commercial LPG cylinders for the hospitality sector, cautioning that continued shortages could force restaurants and hotels across the state to shut down operations entirely. The association has appealed to CM Himanta Biswa Sarma to step in, describing the situation as an “escalating commercial LPG crisis” impacting the restaurant industry in Assam. Members said that eateries across the state are grappling with an abrupt disruption in the supply of commercial LPG cylinders, leaving many struggling to function.

Business

After Anthropic hit, Infosys, TCS & other Indian IT stocks tank on Nvidia’s new AI system news; what’s happening – The Times of India

Indian IT shares tank! Shares of Indian IT companies dropped by as much as 6% on Tuesday after fresh artificial intelligence announcements from global chipmaker Nvidia, which reignited concerns about AI-driven disruption in the technology services sector. Investor caution also remained high ahead of the US Federal Reserve’s FOMC meeting scheduled for later this week.Indian IT stocks had already experienced a notable drop earlier this year after Anthropic introduced plug-ins for its Claude Cowork agent, capable of automating tasks across departments such as legal, sales, marketing and data analysis. Some analysts had then warned that IT services firms may eventually need to reduce their workforce as more affordable and efficient AI tools begin to replace certain functions.

What Nvidia has announced

At its annual GTC developer conference in San Jose, California, Nvidia said the potential revenue opportunity for its artificial intelligence chips could reach at least $1 trillion by 2027. During the event, CEO Jensen Huang introduced a new central processor along with an AI system built using technology from Groq, a chip startup whose technology Nvidia licensed for $17 billion in December.“The inference inflection has arrived,” Huang said. “And demand just keeps on going up,” he added.Wall Street closed higher after Nvidia’s announcements. The S&P 500 rose 1% to finish at 6,699, marking its strongest single-day gain in more than a month. The tech-heavy Nasdaq advanced 1.22%, while the Dow Jones Industrial Average climbed 0.83%.Investors are also closely watching the outcome of the US Federal Reserve’s FOMC meeting scheduled later this week. The decision is expected to influence sentiment toward IT stocks, as Indian technology companies generate a large share of their revenue from the US market.

Indian IT shares take a hit

Shares of Coforge fell about 6%, while major companies such as Wipro, Infosys, Mphasis, LTI Mindtree and Persistent Systems each declined by more than 2%. Several of these stocks touched fresh 52-week lows during the session, according to an ET report.Earlier, brokerage Nuvama said in a note that the sharp correction in IT stocks since the start of the year, triggered by fears of AI-driven disruption following successive AI tool launches by Anthropic, has made valuations in the sector more appealing.“Reports of my death are greatly exaggerated,” Nuvama said, quoting Mark Twain to describe what it believes reflects the current situation in the IT industry.“Given the advent and adoption of Gen AI, obituaries of the Indian IT services industry are being written all around. The concerns have been amplified by the sharp stock reactions, first with global SaaS and now with IT services companies,” the note said according to ET.Nuvama added that it does not view generative AI as an existential threat to the sector. The brokerage said companies will continue to require system integrators capable of customising plug-and-play enterprise software inputs and outputs to meet specific organisational needs.(Disclaimer: Recommendations and views on the stock market, other asset classes or personal finance management tips given by experts are their own. These opinions do not represent the views of The Times of India)(Disclaimer: Recommendations and views on the stock market, other asset classes or personal finance management tips given by experts are their own. These opinions do not represent the views of The Times of India)

Close Brothers to cut hundreds of jobs amid criticism over car finance scandal plan

Nine African players to watch at March Madness on ESPN in Africa and Disney+

Tennessee minors sue Musk’s xAI, alleging Grok generated explicit images of them

: Nifty50 opens below 23,600; BSE Sensex down over 900 points on continuing US-Iran war – The Times of India")

Stock market crash today (March 12, 2026): Nifty50 opens below 23,600; BSE Sensex down over 900 points on continuing US-Iran war – The Times of India

Intertextile Shanghai 2026: Fringe events spotlight market trends

2026 NCAA Tournament Berth Tracker: Automatic Bids, Championship Game Times, and Defending Champs

-

Business5 days ago

Stock market crash today (March 12, 2026): Nifty50 opens below 23,600; BSE Sensex down over 900 points on continuing US-Iran war – The Times of India

-

Fashion1 week ago

Fashion1 week agoIntertextile Shanghai 2026: Fringe events spotlight market trends

-

Sports1 week ago

Sports1 week ago2026 NCAA Tournament Berth Tracker: Automatic Bids, Championship Game Times, and Defending Champs

-

Entertainment7 days ago

Entertainment7 days agoWhat time will NASA’s 600 kg satellite crash to Earth today— 14 years after launch?

-

Fashion1 week ago

Fashion1 week agoGerman brand Adidas posts 13% revenue growth in 2025

-

Business1 week ago

Business1 week agoGulf war risks global economic shock | The Express Tribune

-

Tech1 week ago

Tech1 week agoIs Daylight Saving Time Killing Your Mornings? This Gadget Can Save Them

-

Fashion6 days ago

Fashion6 days agoUK’s Topshop unveils Tolu Coker capsule collection