Business

Serena Williams invests in women’s basketball league Unrivaled, now valued at $340 million

Serena Williams introduces Maria Sharapova during the 2025 Induction Celebration weekend at the International Tennis Hall of Fame in Newport, Rhode Island, on Aug. 23, 2025.

Joe Buglewicz | Getty Images Sport | Getty Images

Women’s 3-on-3 basketball league Unrivaled is now valued at $340 million after a new funding round that included tennis legend Serena Williams, the league announced Monday.

Williams’ Serena Ventures was part of a Series B funding round that was led by Bessemer Venture Partners and also included Warner Bros. Discovery and Alex Morgan’s Trybe Ventures. Unrivaled did not disclose the size of the individual contributions.

Unrivaled’s latest cash infusion means a dramatic rise in its valuation from just one year ago when the league was valued at $95 million, according to a person familiar with the league who spoke on the condition of anonymity about internal matters.

The investment comes as women’s sports have soared in both popularity and valuations in recent years.

“To add arguably the most iconic female athlete to play sports, I think it exemplifies who Unrivaled is not just with our players on the court, but the number of investors on our cap table who had been icons in their own lanes,” said Alex Bazzell, co-founder and president of Unrivaled.

Angel Reese, #5 of Rose, goes up for a shot against Napheesa Collier, #24 of the Lunar Owls, during the second half at Wayfair Arena in Medley, Florida, on Feb. 21, 2025.

Rich Storry | Getty Images Sport | Getty Images

Other Unrivaled investors include high-profile names such as tennis legend Billie Jean King, NBA superstar Stephen Curry, tennis champion Coco Gauff and Olympic swimmer Michael Phelps.

Bessemer has previously invested in ticketing resale site StubHub, as well as streaming services BallerTV and Twitch. The venture firm sees Unrivaled as a blueprint for the next generation of sports leagues, according to Caty Rea, a vice president at Bessemer.

“We always look for category-defining businesses with generational tail winds and really audacious founders who kind of have that product hard to fit,” Rea said. “We felt like we found that with Unrivaled.”

Unrivaled was founded in 2023 and offers women’s professional basketball players a league that runs in the offseason of the WNBA. Previously, many players went abroad in the offseason for extra compensation.

The league says it offers women the highest average salary in professional women’s sports history and provides equity to players.

For comparison, the WNBA does not offer its players equity, and players are currently negotiating their collective bargaining agreement, which expires Oct. 31. One of the key issues being debated is an increase in player compensation. WNBA Commissioner Cathy Engelbert told CNBC in July that the average WNBA team valuation has increased to about $260 million.

Bazzell said the new funding will be used to add more resources to the league’s facilities, for developmental efforts and to create additional awareness of the league as it heads into its second season.

“We’ve built a sustainable and sticky audience, both on television and certainly on social. So now we have to grow that footprint,” he said.

Business

Armageddon scenario! Why Iran’s missile strikes on Qatar’s LNG spell nightmare for Europe, Asia – The Times of India

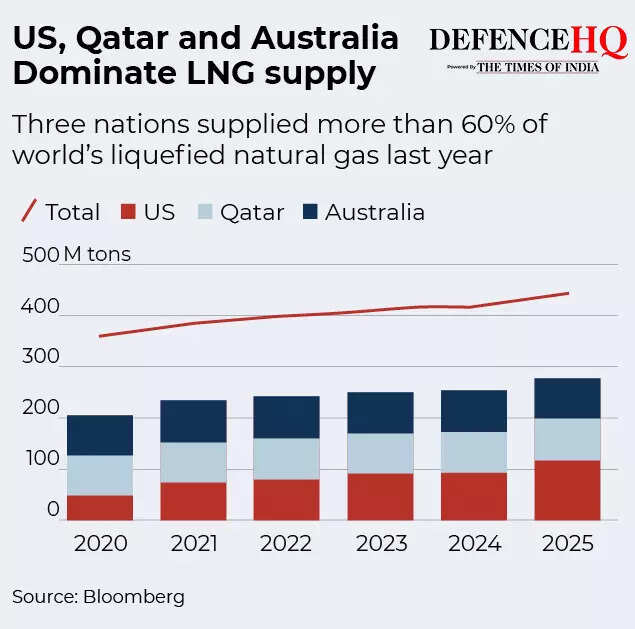

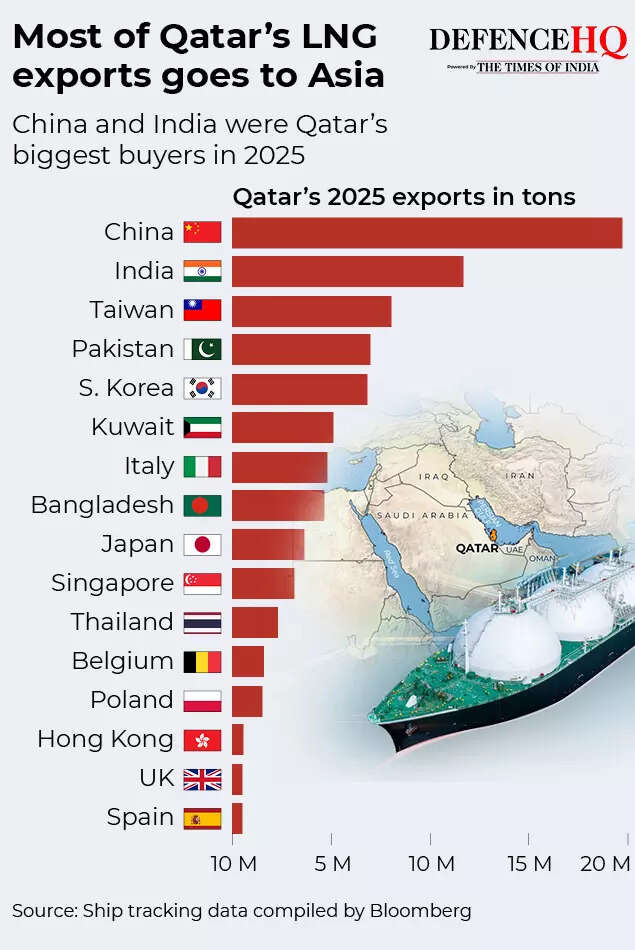

Is an Armageddon scenario about to play out? Europe and Asia are facing a nightmare scenario with the escalating crisis in the Middle East now increasingly impacting key energy infrastructure. The latest shockwave for the market has come in the form of a big hit to Qatar’s Ras Laffan complex on Thursday morning by Iran.LNG or liquefied natural gas facilities rank among the most intricate and large-scale industrial structures ever built, and Ras Laffan stands as the biggest of them, converting Qatar’s vast gas reserves into super-cooled fuel for global transport—until the Iranian missile strikes disrupted operations.This has led to markets across Europe and Asia confronting a new energy shock. Under normal conditions, roughly one-fifth of the world’s LNG supply originates from Ras Laffan, which is a sprawling industrial hub developed over three decades at a cost of hundreds of billions of dollars and covering an area nearly three times that of Paris.To understand the scale of LNG operations at the facility, sample this: Ras Laffan operates 14 liquefaction trains that process gas into 77 million tonnes of LNG annually, sufficient to meet Japan’s entire yearly demand or exceed the combined needs of the UK and Italy!

Armageddon scenario plays out for Europe, Asia

The immediate impact of the latest strikes was evident across global energy markets. Brent crude prices briefly surged by over 10 percent, crossing the $119-per-barrel mark before easing from those highs.

In Europe, gas prices spiked as much as 35 per cent and later stabilised at around 70 euros per megawatt hour, still reflecting a gain of about 28 per cent. This rise is expected to feed through to electricity costs, as power prices in the region are largely linked to gas rates.Analysts at EnergyScan told AFP, “We are not yet in the worst-case scenario we described in our last monthly report, but we are getting closer.”European gas prices have more than doubled since the US-Israel-Iran conflict began, as traders assessed the implications of a prolonged disruption to Qatar’s LNG exports. “I woke up this morning and thought, ‘No, please no,’”Anne-Sophie Corbeau, former head of gas analysis at BP and now with Columbia University’s Center on Global Energy Policy, told the Financial Times. “This has always been my nightmare scenario, my Armageddon scenario, the one I didn’t want to happen,” the report quoted the expert saying.Two gas traders said they were still trying to absorb the scale of the incident after Iran carried out a two-stage attack, launching ballistic missiles at the facility late Wednesday and again in the early hours of Thursday. “This is unprecedented,” one of them said.QatarEnergy, the state-owned operator of Ras Laffan, told Reuters that damage to two LNG units—developed in partnership with ExxonMobil—could take between three and five years to repair. The disruption is expected to result in annual revenue losses of $20 billion and force the cancellation of long-term supply agreements with Italy, Belgium, Korea and China.The disruption has effectively removed about 17 per cent of Qatar’s overall gas output for the foreseeable future. Prior to the strike, market participants believed LNG shipments from Ras Laffan would quickly resume once tensions in the Middle East subsided and the Strait of Hormuz became secure for tanker movement. Although prices had climbed last week, they had steadied at levels well below those recorded during Russia’s invasion of Ukraine in 2022.That outlook has now been overturned!

Years of repair to drive up prices

One trader told Financial Times that European gas prices are likely to remain elevated “through 2027,” while the region could struggle to replenish storage levels over the summer as Asian buyers turn to US LNG to offset the shortfall. Asia was already dealing with constrained supply and rationing following disruptions from the Gulf. Europe, increasingly dependent on LNG after Russia curtailed pipeline exports during its war with Ukraine, now faces intensified competition with countries such as Japan and South Korea for limited LNG cargo availability.

Laurent Segalen, a clean energy investment banker, was quoted as saying: “It is apocalypse now. The coming months for gas importers are going to be a bloodbath.” The infrastructure required to cool gas into LNG is highly complex and cannot be replaced quickly. Repairs will involve a meticulous process that can only begin once Qatar is assured that the site is secure and personnel can return without the threat of further attacks.Tom Marzec-Manser, an LNG specialist at energy consultancy Wood Mackenzie, said it is already clear that a return to normal output levels in Qatar will not happen quickly, regardless of how soon the conflict ends. “What we can conclude immediately is that regardless of when the conflict now ends, a resumption of normal production from Qatar is not going to happen in a matter of weeks,” he told FT.The expert noted that earlier projections had suggested production at Ras Laffan could resume within about 40 days, but that timeline is no longer realistic. He also indicated that Qatar’s ambitious expansion plans for the facility, which include adding six new liquefaction units over this year and next, are now likely to face delays. “There is an element of uncertainty, but we know now this is a months-long reduction in supply,” he added.Although some LNG projects in the United States are expected to come online soon, Corbeau said replacing Qatari supply is far from straightforward and involves significant political challenges. She pointed out that some policymakers have already begun advocating for easing restrictions on Russian gas imports.At the same time, several countries have started reverting to coal-based power generation, while industrial operations in parts of Southeast Asia are being forced to scale back or suspend production due to limited energy availability. “The world of energy is going to fracture between the haves and the have-nots,” said Segalen.

Analysts fear the disruption to supply could continue for longer than initially thought.

Source link

Policymakers vote unanimously to hold rates at 3.75% after the Iran war prompts a sea-change in the debate over borrowing costs.

Source link

A New Game Turns the H-1B Visa System Into a Surreal Simulation

How assistant managers handle players, personal ambition

Armageddon scenario! Why Iran’s missile strikes on Qatar’s LNG spell nightmare for Europe, Asia – The Times of India

: Nifty50 opens below 23,600; BSE Sensex down over 900 points on continuing US-Iran war – The Times of India")

Stock market crash today (March 12, 2026): Nifty50 opens below 23,600; BSE Sensex down over 900 points on continuing US-Iran war – The Times of India

UK’s Topshop unveils Tolu Coker capsule collection

US ignites Iran war, but Gulf Arab states pay the price | The Express Tribune

-

Business1 week ago

Stock market crash today (March 12, 2026): Nifty50 opens below 23,600; BSE Sensex down over 900 points on continuing US-Iran war – The Times of India

-

Fashion1 week ago

Fashion1 week agoUK’s Topshop unveils Tolu Coker capsule collection

-

Business1 week ago

US ignites Iran war, but Gulf Arab states pay the price | The Express Tribune

-

Fashion1 week ago

Fashion1 week agoIndia’s textile recycling market may reach $3.5 bn by 2030: Report

-

Tech1 week ago

Tech1 week agoMeta Developed 4 New Chips to Power Its AI and Recommendation Systems

-

Business1 week ago

Business1 week ago8th Pay Commission: How Much Will Central Govt Employees’ Salaries Rise? What We Know So Far

-

Sports1 week ago

Sports1 week agoBangladesh crush Pakistan in ODI series opener | The Express Tribune

-

Entertainment1 week ago

Entertainment1 week agoGas, food, household prices explained