Business

The Poundland stores set to close revealed after business escapes collapse

A high-street retailer is set to close a number of its stores across Britain after narrowly avoiding collapse.

Poundland received court approval for a major restructuring plan on Tuesday after the company told a judge that the plan would save it from entering administration.

Had the scheme had not been sanctioned, the company would have run out of money by September 7, barristers told the court.

In June, the discount retail chain said it planned to permanently shut 68 shops after being sold by Pepco Group to Peach Bidco, a subsidiary of private equity firm Gordon Brothers, for £1.

Poundland said it will shut down a total of 16 more stores but has not yet identified their locations.

It is understood that the closure dates for these are likely to be announced later in the year, when store workers will be informed.

These are the stores set to close on Sunday, August 31:

- Blackburn, Lancashire

- Cookstown, Northern Ireland

- Erdington, West Midlands

- Kimberley Nottingham, Nottinghamshire

- Horsham, West Sussex

- Hull Kingston retail park, East Yorkshire

- Kettering, Northamptonshire

- Omagh, Northern Ireland

- Shepherd’s Bush, Greater London

- Southport, Merseyside

- Taunton, Somerset

This store will shut on September 14:

The following stores have already closed:

- Ammanford, Wales

- Birmingham Fort Shopping Park, West Midlands

- Cardiff, Wales

- Cramlington, Northumberland

- Leicester, Leicestershire

- Long Eaton, Nottinghamshire

- Port Glasgow, Scotland

- Seaham, County Durham

- Shrewsbury, Shropshire

- Tunbridge Wells, Kent

- Bedford, Bedfordshire

- Bidston Moss, Merseyside

- Broxburn, Scotland

- Craigavon, Northern Ireland

- Dartmouth, Devon

- East Dulwich, Greater London

- Falmouth, Cornwall

- Hull St Andrew retail park, East Yorkshire

- Newtownabbey, Northern Ireland

- Perth, Scotland

- Poole, Dorset

- Sunderland Pallion retail park, Tyne and Wear

- Stafford, Staffordshire

- Thornaby, North Yorkshire

- Worcester, Worcestershire

- Brigg, North Lincolnshire

- Canterbury, Kent

- Coventry Hertford Street, West Midlands

- Newcastle Killingworth Centre, Tyne and Wear

- Kings Heath, West Midlands

- Peterborough Orton Gate shopping centre, Cambridgeshire

- Peterlee, County Durham

- Rainham, Kent

- Salford, Greater Manchester

- Sheldon, West Midlands

- Wells, Somerset

- Whitechapel, Greater London

- Swiss Cottage, Greater London

- Southampton West Quay, Hampshire

- Chiswick, Greater London

Business

US stocks today: Wall Street inches higher as markets eye ceasefire deadline; Dow jumps 300 points, S&P 500 remains flat – The Times of India

US stocks moved higher on Tuesday, as investors remained optimistic over a possible extension of the US-Iran ceasefire. Markets showed early strength, with the Dow Jones Industrial Average rising 0.56% or 279 points to 49,721.56 around 8 pm IST. The S&P 500 inched up 0.2% to 7,129, while the Nasdaq Composite gained 96 points or 0.4% to reach 24,500. As trading progressed, the upward momentum strengthened, with the Dow climbing 397 points, or 0.8%, and the S&P 500 adding 0.2%, putting it within reach of another record high. The Nasdaq remained modestly higher. Investor sentiment was shaped in part by developments in the Middle East. Oil prices, which had surged a day earlier amid renewed disruption to the Strait of Hormuz, eased on Tuesday. Brent crude slipped 0.7%% to $94.78 per barrel ahead of the expected expiry of a two-week ceasefire between the United States and Iran. The conflict has driven sharp swings in oil markets, with prices ranging from about $70 before the war to peaks of $119 as concerns over a prolonged closure of the key shipping route intensified. Economic data released during the session pointed to continued resilience in consumer activity. US retail sales rose 1.7% from the previous month to $752.1 billion, beating expectations, largely due to higher petrol prices. Spending remained relatively steady even when excluding gasoline sales, indicating broader stability in consumption during the first full month of the conflict. Global markets presented a mixed picture, with European indices trading unevenly after a stronger performance in Asia, where South Korea’s Kospi index jumped 2.7%. In the bond market, US Treasury yields edged higher, with the 10-year yield ticking up to 4.27% from 4.26% the previous day. Attention is also turning to Washington, where Kevin Warsh, nominated by US President Donald Trump to lead the Federal Reserve, is scheduled to testify before Congress later in the day. Investors are expected to closely watch his remarks for indications on interest rate policy and the central bank’s independence.(Disclaimer: Recommendations and views on the stock market, other asset classes or personal finance management tips given by experts are their own. These opinions do not represent the views of The Times of India.)

Business

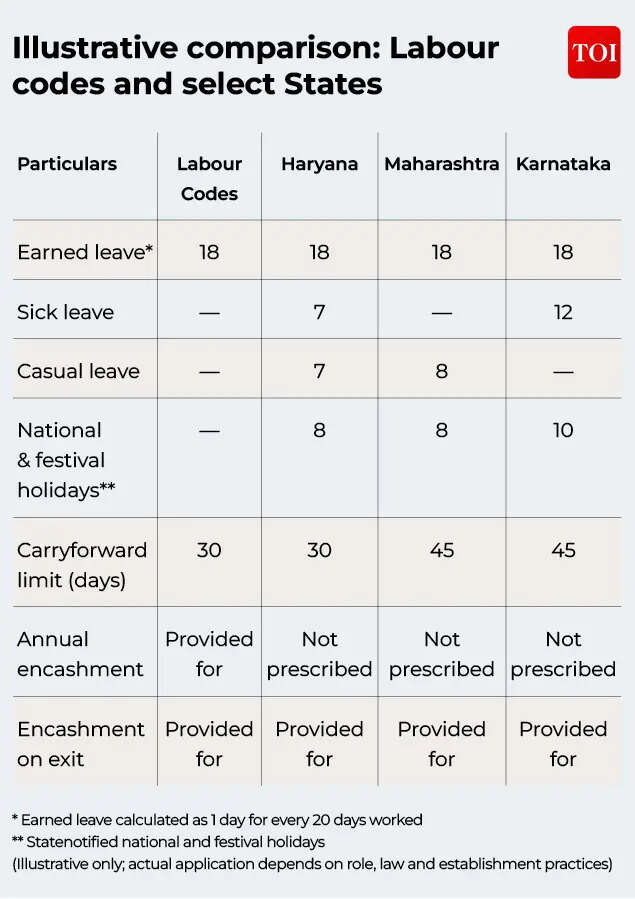

Leave, holidays and encashment: What India’s changing labour laws mean for employees – The Times of India

Leave is often seen as a simple workplace benefit – an approved absence from work. In reality, it is one of the more structured and regulated aspects of employment in India. With the implementation of new labour codes, questions around leave entitlement, holidays and leave encashment have drawn renewed attention. This matters because these rules affect not just everyday working life, but also what happens when an employee leaves an organisation.For employers and employees, understanding how leave works today is not always straightforward. This is because two legal systems operate side by side: the new central labour codes and the older State-level Shops and Establishments (S&E) laws. While the intent is to move towards a simpler and more uniform system, the actual position still depends on job role, location and which law applies.Different types of statutory leaveIndian labour laws recognise several types of statutory leave. The most important is earned leave (also called privilege leave). This leave builds up over time based on how many days an employee works. In addition, there are provisions for sick leave, casual leave, and national and festival holidays.Earned leave is different from other types of leave because it has both time-off value and financial value. If it is not used, it can build up and may be paid out in cash – either during employment or when the employee leaves, subject to carry forward limits – depending on the applicable law and company policy.Sick leave and casual leave, on the other hand, are meant for short-term or urgent needs and are usually not designed to be encashed.National and festival holidays form a separate category. These ensure paid holidays on important national or regional days, based on State notifications and local rules.Labour codes vs Shops and Establishments lawsA frequent point of confusion is the interface between the labour codes and State Shops and Establishments Acts.The Occupational Safety, Health and Working Conditions Code introduces a common framework for leave, but for people classified as “workers” under that law. At the same time, State S&E laws continue to apply to many salaried employees working in offices, shops and service-sector businesses.Because of this, uniformity has not fully arrived yet. Different State laws and leave rules may still apply for employees depending on where they are employed and work. Those who fall under the labour code framework move towards a more standard national system. Where both laws could apply, guidance from authorities suggests that the more beneficial provision would generally continue to apply.

Employers are expected to apply these frameworks together and ensure consistency as the new system takes shape.How earned leave builds upEarned leave generally depends on how long an employee has worked.Under the labour codes, earned leave accrues at a standard rate of one day for every twenty days of work, subject to certain eligibility conditions. This is meant to create a common reference point across the country.State Shops and Establishments laws, however, follow different approaches. Some States grant a fixed number of leave days each year, while others link leave closely to days worked. States also differ on how much unused leave can be carried forward.Sick leave, casual leave and holidaysSick leave and casual leave are mainly meant for short-term protection rather than long-term accumulation. Sick leave helps employees during illness, while casual leave allows flexibility for sudden personal needs.These types of leave are mostly governed by State law and internal company policy, with limited direct impact from the labour codes. Usually, unused sick or casual leave does not carry forward.National and festival holidays are largely decided at the State level. Employers are expected to follow notified holiday lists or compensate employees who work on those days, as per State rules.Carrying forward unused earned leaveHow unused earned leave is treated is one area where the labour codes bring more structure.Earlier, State laws allowed different levels of leave accumulation. Under the labour code approach, carry-forward is subject to clear limits, after which settlement mechanisms may apply. This is intended to avoid unlimited build-up of leave while still protecting employee interests.If leave could not be taken because of work requirements, safeguards exist to ensure such leave is not lost automatically.Annual leave encashment under labour codesAnother change under the labour codes is clearer recognition of leave encashment during ongoing employment.Earlier, in many States, leave was typically encashed only when an employee resigned, retired or was terminated. Under the new labour codes framework, employees may be entitled to encash leave exceeding permissible carry forward limits even while they remain in service. As per provisions under labour codes, a worker shall be entitled on his / her demand for encashment of leave at the end of calendar year. Worker shall be entitled, where the total number of leave exceeds 30 days, to encash such exceeded leave.Leave encashment when employment endsAcross Indian labour laws, one position has remained largely consistent. Unused earned leave is expected to be settled when employment comes to an end, whether the employee resigns, retires, is retrenched or is terminated.How this amount is calculated depends on the applicable law. State S&E laws refer to specific wage definitions, while the labour codes require calculation using the definition of “wages” under the Code. This may differ from earlier practice.

What employees and employers should keep in mindFor employees, the key point is that leave is not only a company benefit but part of a legal framework. How it applies depends on role, location and legal coverage.For employers, the focus remains on aligning internal policies with both Central and State laws, while ensuring smooth implementation. Clear communication and regular policy reviews will continue to be important during this transition.Leave rules may not attract the same attention as pay or job security, but they play a quiet role in work-life balance and financial certainty. As India’s labour framework evolves, earned leave is increasingly seen not just as time away from work, but as a regulated employment benefit with defined outcomes.(The author, Puneet Gupta is Partner, People Advisory Services Tax at EY India)

The war in the Middle East has brought renewed attention to Britain’s vulnerability to energy price shocks.

Source link

WhatsApp to let users generate private summaries of unread chats

US stocks today: Wall Street inches higher as markets eye ceasefire deadline; Dow jumps 300 points, S&P 500 remains flat – The Times of India

Soccer’s incredible shrinking shin guards could be a big problem

-

Fashion5 days ago

Fashion5 days agoFrance’s LVMH Q1 revenue falls 6%, shows resilience amid Iran war

-

Sports1 week ago

Sports1 week agoThe case for Man United’s Fernandes as Premier League’s best

-

Entertainment1 week ago

Entertainment1 week agoPalace left in shock as Prince William cancels grand ceremony

-

Business1 week ago

Business1 week agoUK could adopt EU single market rules under new legislation

-

Entertainment6 days ago

Entertainment6 days agoIs Claude down? Here’s why users are seeing errors

-

Fashion1 week ago

Fashion1 week agoEnergy emerges as biggest cost driver in textile margins

-

Business1 week ago

Business1 week agoDelta Air Lines unveils first new Delta One suite in premium cabin arms race

-

Fashion1 week ago

Fashion1 week agoAsia claims largest share of markets on Kearney FDI Confidence Index