Business

Trump sees a ‘dead economy’ – but US-based S&P Global upgrades India’s credit rating – here’s why – Times of India

S&P Global, the US-based credit ratings agency, has upgraded India’s rating to ‘BBB’ from ‘BBB-) citing several positive factors in favour of the world’s fifth largest economy. S&P’s confidence in India’s growth story comes at a time when US President Donald Trump has imposed a 50% tariff on Indian exports to America, and has even called India a ‘dead economy’. This is reportedly the first rating upgrade for India in almost 19 years.The credit rating of an economy reflects the country’s ability and willingness to repay debt. It is a crucial indicator of economic health, indicating the risk level for investors and lenders.

“The upgrade of India reflects its buoyant economic growth, against the backdrop of an enhanced monetary policy environment that anchors inflationary expectations. Together with the government’s commitment to fiscal consolidation and efforts to improve spending quality, we believe these factors have coalesced to benefit credit metrics,” S&P said.

Little impact of Trump’s tariffs on India

Not only has S&P upgraded India’s sovereign rating, it has also said that the impact of US tariffs is not likely to be extensive on India’s economy.“We believe the effect of US tariffs on the Indian economy will be manageable. India is relatively less reliant on trade and about 60% of its economic growth stems from domestic consumption,” S&P Global said.“We expect that in the event India has to switch from importing Russian crude oil, the fiscal cost, if fully borne by the government, will be modest given the narrow price differential between Russian crude and current international benchmarks,” it said.While the United States is India’s biggest trading ally, the potential imposition of 50% tariffs is not anticipated to significantly hinder economic growth. Exports from India to the US account for roughly 2% of the country’s GDP, S&P notes.Taking into account specific exemptions for sectors like pharmaceuticals and consumer electronics, the portion of Indian exports that would be affected by these tariffs decreases to 1.2% of GDP. Although this could lead to a temporary setback in growth, we predict that the overall effect will be minimal and will not disrupt India’s long-term economic trajectory, it added.Also Read | ’Secondary tariffs could go up…’: US official warns of higher sanctions on India if Trump’s talks with Putin fail; asks Europe to ‘put up or shut up’After Trump’s move to impose high tariffs on India, several global institutions and experts have predicted that India’s GDP growth may take an up to 0.3% hit due to US trade moves.

Major items US imports from India

Why did S&P upgrade India’s credit rating?

- India continues to be one of the top-performing economies globally. It has made a significant recovery from the pandemic, with real GDP growth from fiscal year 2022 (ending March 31) to fiscal year 2024 averaging 8.8%, the highest in the Asia-Pacific region.

- The Indian economy’s overall size is now believed to be approximately 80% bigger in rupee terms compared to its pre-COVID state, and nearly 50% larger when measured in dollars. However, the pace of economic growth is stabilizing towards a more sustainable rate, maintaining strong momentum.

- S&P anticipates that this growth trend will persist in the medium term, with GDP projected to rise by 6.8% annually over the next three years. This growth helps to moderate the government debt-to-GDP ratio, despite the presence of substantial fiscal deficits.

- The recent performance of India’s economy underscores its enduring strength. S&P’s forecasts for robust growth, despite external challenges, are based on the country’s positive structural developments. These include favorable demographics and competitive labor costs.

- India’s corporate and financial sectors have improved their balance sheets compared to the pre-pandemic period. Nonetheless, S&P acknowledges that maintaining high growth rates over an extended period is essential for the economy to generate enough jobs, lessen inequality, and fully capitalize on its demographic advantages.

- India’s fiscal weaknesses have historically been the most fragile aspect of its sovereign credit ratings. However, with the economy now on a solid recovery path, the government is able to outline a clearer, though gradual, strategy for fiscal consolidation. S&P forecasts suggest that the general government deficit, which is 7.3% of GDP in fiscal year 2026, will decrease to 6.6% by fiscal year 2029.

- Over the past five to six years, the quality of government expenditure has seen improvement, says S&P. The current government has increasingly prioritized infrastructure in its budget allocations. The union government’s capital expenditure is projected to rise to 11.2 trillion Indian rupees, or approximately 3.1% of GDP, by fiscal year 2026, up from 2% of GDP a decade ago.

- When including capital spending by state governments, total public investment in infrastructure is expected to be around 5.5% of GDP, which is comparable to or exceeds that of similar sovereign entities. S&P anticipate that enhancements in infrastructure and connectivity in India will eliminate bottlenecks that currently impede long-term economic growth.

- The shift in monetary policy towards inflation targeting has proven beneficial. Inflation expectations are now more stable compared to ten years ago. From 2008 to 2014, India frequently experienced inflation rates in the double digits. However, over the last three years, despite fluctuations in global energy prices and supply disruptions, the Consumer Price Index (CPI) has grown at an average rate of 5.5%. Recently, it has remained at the lower end of the Reserve Bank of India’s (RBI) target range of 2%-6%. These changes, along with a robust domestic capital market, indicate a more stable and conducive environment for monetary policy, says S&P.

- India’s sovereign ratings are supported by a vibrant and rapidly expanding economy, a strong external balance sheet, and democratic institutions that ensure policy consistency. These positive aspects are offset by the government’s poor fiscal performance, high debt levels, and low GDP per capita.

Indian Economy: The road ahead

“The Indian general elections resulted in a third consecutive term for Prime Minister Narendra Modi after his Bhartiya Janata Party (BJP) won the largest number of seats but fell short of an absolute majority. The subsequent formation of a coalition government is a first for the BJP, which has ruled independently in its previous two terms,”S&P said.“But the BJP retains a healthy majority in the Lok Sabha, India’s lower house of parliament. This supports the government’s efforts to implement economic reforms. Since the beginning of economic liberalization in 1991, India has had consistently high GDP growth while governed by different political parties and coalitions–reflecting a consensus on key economic policies,” it adds.Also Read | ‘Can’t cross some red lines’: Government officials tell Parliamentary Panel on India-US trade talks; focus on export diversification amidst Trump tariffs“In our view, the success of the government in funding large infrastructure investment without substantially widening the country’s current account deficit will be important. If India can shrink the fiscal deficit significantly while achieving these objectives, rating support will strengthen over time,” it says.According to S&P Global, its stable outlook indicates the belief that India’s long-term growth prospects will be bolstered by consistent policy stability and significant infrastructure investments. This, coupled with prudent fiscal and monetary policies that help manage the government’s high debt and interest obligations, will support the rating over the next two years.S&P said that it may upgrade the ratings if fiscal deficits significantly decrease, leading to a structural reduction in the net change of general government debt to below 6% of GDP. Sustained increases in public infrastructure investment would enhance economic growth, and when combined with fiscal reforms, could strengthen India’s weak public finances.However, S&P said it might consider lowering the ratings if it sees a decline in political commitment to improving public finances. Additionally, if India’s economic growth significantly slows down in a way that threatens fiscal sustainability, it could also exert downward pressure.

Business

NaBFID signs pact with PDCOR to expand advisory support for state projects – The Times of India

The National Bank for Financing Infrastructure and Development (NaBFID) has signed a Memorandum of Agreement with Projects Development Company of Rajasthan Limited (PDCOR) to strengthen advisory services for state and city-level infrastructure projects.The agreement will also allow both institutions to jointly explore financing and transaction advisory opportunities, including transaction structuring, commercial and technical due diligence, and support for financial closure of projects undertaken by state governments and urban local bodies across India, according to PTI.“This collaboration seeks to enhance access to long-term institutional finance for State Governments and Urban Local Bodies, while strengthening the infrastructure advisory and financing ecosystem,” Rajkiran Rai G., Managing Director of NaBFID, said.He added that the partnership would help both institutions jointly pursue project advisory opportunities, develop replicable financing frameworks, accelerate financial closures and mobilise capital across the infrastructure value chain.Monika Kalia, DMD-CFO, NaBFID, said the tie-up would leverage the strengths of both organisations to provide much-needed advisory support to states and urban local bodies for impactful urban infrastructure projects.Dileep Chingapurath, Chief Executive Officer, PDCOR, said the agreement would address the long-felt need for end-to-end professional support to structure and mobilise sustainable financing solutions, particularly for state governments and their agencies.“Through this collaboration, both institutions aim to enhance the quality of project preparation, mobilise institutional capital more effectively and accelerate the implementation of sustainable infrastructure projects across states and municipalities,” he said.NaBFID is a Development Financial Institution focused on long-term infrastructure financing, while PDCOR is an undertaking of the Government of Rajasthan.

Business

Explained: On way to 4th largest, how India slipped to 6th rank & what it means for 3rd largest economy dream – The Times of India

In April 2025 when the International Monetary Fund (IMF) released its World Economic Outlook, India was seen overtaking Japan to become the world’s fourth largest economy by the end of 2025-26. One year later, India has slipped to the sixth position on the largest economies rankings, with the United Kingdom reclaiming its spot as the fifth largest economy.In fact, IMF’s latest World Economic Outlook (April 2026) sees India sitting at the sixth spot this financial year too. This projection comes even as India has grown better than expected in FY26 and is seen retaining its tag of being the world’s fastest growing major economy.What has led to the sudden fall? Why has India dropped to the sixth position, falling behind the UK, instead of overtaking Japan to become the fourth largest economy? And what does this setback mean for its dream of becoming the third largest economy by the end of this decade? We decode:

Data drive: India projected as 4th largest, but fell to 6th spot

First let’s look at some IMF data to see which way the Indian economy was headed in April 2025, and what the April 2026 outlook data suggestsAs per April 2025 estimates of IMF, India’s economy would have been at $4601.225 billion at the end of FY 2025-26, overtaking Japan which was estimated at $4373.091 billion. The UK at the 6th spot was projected to have a nominal GDP of $4040.844 billion.However, as per the April 2026 estimates, India’s economy had a nominal GDP of $4,153 billion at the end of FY 2025-26, with the UK overtaking it with $4,265 billion GDP. Japan’s GDP is seen at $4,379 billion.As the above estimates show, India’s GDP estimates have seen a drop over one year, while UK’s nominal GDP has grown better than expected. Japan has been steady.So, what went wrong? Blame the rupee and GDP data itself!

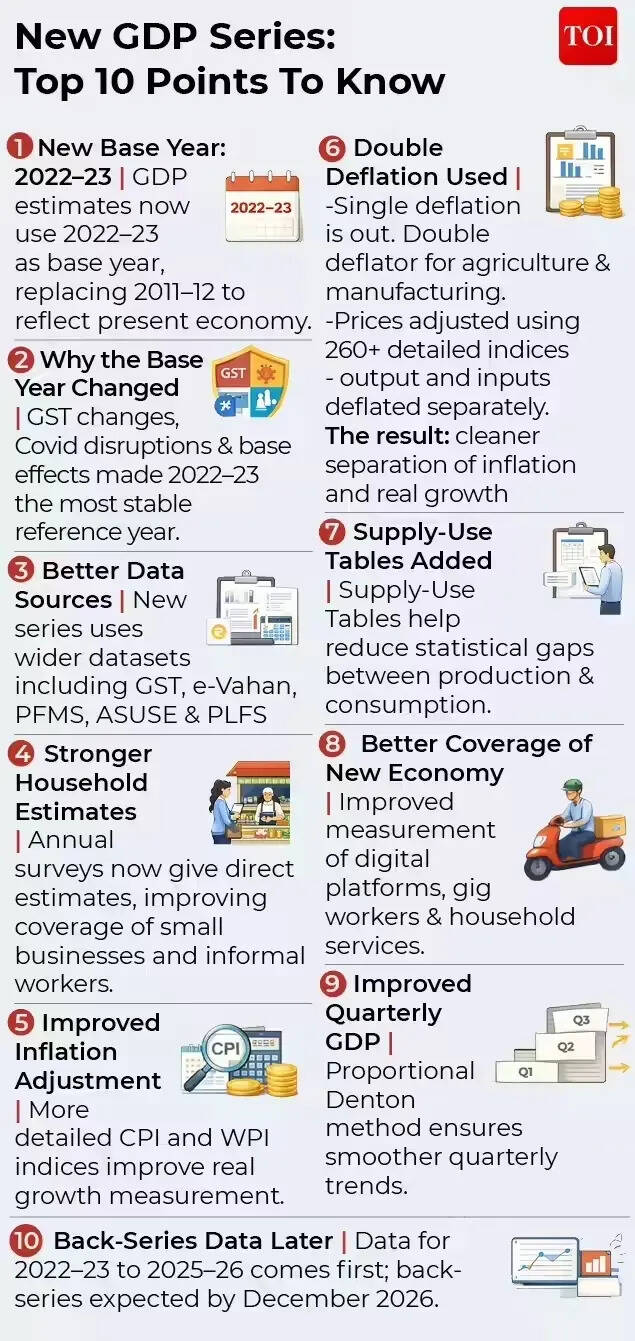

Rupee Depreciation Blow & New GDP Series

The first thing to understand is that IMF’s data on the size of a country’s nominal GDP is in dollar terms. Hence, with global rankings based on dollar‑denominated GDP, they are highly sensitive to exchange rate movements. The biggest party pooper for India’s dream of becoming the fourth largest has been the rupee’s slide. The Indian currency has depreciated more than expected over the last year, dropping from 84.57 versus the US dollar in 2024 to 88.48 in 2025, as per IMF data. The IMF estimates see it at 92.59 this year.Several factors have contributed to the rupee’s decline, including capital outflows, uncertainty related to India-US trade deal up until February, and the recent Middle East conflict which has raised crude oil prices and India’s import bill. Also, the RBI while actively managing volatility in the forex market, is not targeting any particular level of the rupee.Arun Singh, Chief Economist, Dun & Bradstreet India says that India’s recent slip to sixth place in global GDP rankings does not reflect a weakening of the economy, but is largely the result of currency conversion effects and a one‑time statistical revision.The rupee’s depreciation from 2024 to 2026, has mechanically compressed India’s GDP in dollar terms, effectively halving apparent growth despite strong domestic expansion, says Arun Singh.According to Ranen Banerjee, Partner and Leader, Economic Advisory Services, PwC India, GDP in US dollar terms would shave off with rupee depreciation. “We have had almost 7-8% depreciation over the last few months owing to the conflict and portfolio outflows. Thus, in effect in US dollar terms, it is close to shaving out almost a year’s nominal GDP,” he tells TOI.And it’s not just about the Indian economy. The United Kingdom which has overtaken India to bag the 5th spot again also has economic factors working in its favour. UK’s GDP growth at 0.5% has recently beaten forecasts of 0.1% by a wide margin. Not only that, its currency – pound – has actually appreciated against the US dollar.The second factor that has impacted the rankings is India’s adoption of a new base year for its latest GDP series. As per the new data, which also makes use of a more refined methodology, the size of India’s nominal GDP in rupee terms has gone down. Sample this: As per the older base year of 2011-12, India’s GDP at the end of 2025-26 would have been Rs 35,713,886 crore. But under the new series, it is estimated to be Rs 34,547,157 crore. The new calculation methodology and base year revision presents a more accurate picture of the size of the Indian economy.Hence the currency effect has been compounded by a one‑time downward revision following India’s shift to a new GDP base year, which has lowered reported nominal levels without affecting real activity.

Does India’s drop to 6th indicate fundamental weakness?

Experts are confident that India’s growth story is intact and fundamentally strong, a fact that is reflected in projections of it continuing to be the world’s fastest growing major economy. They see technical factors behind the current slip, rather than any deterioration in economic fundamentals.It’s also interesting to note that while India will be the sixth largest economy in FY27, in the upcoming financial year, it is likely to overtake both the UK, and Japan to bag the fourth spot.Arun Singh of Dun & Bradstreet India explains this resilience with numbers:IMF World Economic Outlook (April 2026) data show that India’s GDP at current prices in domestic currency rose strongly from ₹318 trillion in 2024 to ₹346.5 trillion in 2025 and further to ₹384.5 trillion in 2026, translating into robust nominal growth of about 8.9% in 2024–25 and nearly 11% in 2025–26, among the fastest globally. In contrast, other large economies recorded more moderate domestic nominal growth – around 5% in the US, roughly 4% in China, 3–5% in the UK, 3–3.5% in Germany, and lower or volatile growth in Japan – underscoring India’s strong underlying momentum. In times of global economic turmoil, while GDP growth is expected to take some hit, most agencies and experts have pegged India’s growth to be strong. Incidentally, the IMF has even marginally raised its GDP growth forecast for FY27 to 6.5% despite the ongoing Middle East conflict.

“In India, growth for 2025 is revised upward by 1.0 percentage point relative to October, to 7.6 percent, reflecting the better-than-expected outturn in the second and third quarters of the fiscal year and sustained strong momentum in the fourth quarter,” IMF said in its latest outlook. “For 2026, growth is revised upward moderately by 0.3 percentage point (0.1 percentage point relative to January) to 6.5 percent, led by positive contributions from the carryover of the strong 2025 outturn and the decline in additional US tariffs on Indian goods from 50 to 10 percent, which outweigh the adverse impact of the Middle East conflict. Growth is projected to stay at 6.5 percent in 2027,” it added.

Will India become 3rd largest anytime soon?

The rupee depreciation and the nominal GDP revision has also pushed back India’s dream of becoming the third largest economy by the end of this decade. In the October 2025 estimates, IMF had said that India will overtake Germany to become third largest by FY30. However, the April 2026 projections see it reaching the third rank only by FY 2030-31.Experts point to the rupee’s depreciation versus the dollar to note that the road ahead is likely to be uncertain. Madan Sabnavis, Chief economist, Bank of Baroda is confident that India will continue to do well in the coming years.“We will definitely improve in terms of GDP growth which will be higher than that of other countries especially UK and Japan which are just above us. However, the rupee value will finally determine how India gets placed on the global scale,” he told TOI.Ranen Banerjee of PwC India sees rupee beginning to get support with the conflict containment, relatively lower oil prices and portfolio flow reversals with valuations getting attractive in recent times. “Thus, we should not be experiencing any further sharp depreciation of the rupee in the immediate term provided the conflict does not escalate and oil prices relatively softening from their highs and come down to a range of $85-90 a barrel,” he says.For Arun Singh of Dun & Bradstreet, looking ahead, India’s relative position in US dollar‑based GDP rankings will remain highly sensitive to currency movements rather than domestic growth dynamics. “Continued global dollar strength or capital‑flow volatility may cause periodic slippage in rankings despite robust fundamentals. Sustaining external macro stability and limiting undue rupee volatility will be crucial for India’s strong growth performance to translate more fully into higher global economic rankings,” Arun Singh told TOI.The Indian economy, largely driven by domestic fundamentals, is not immune to external shocks. High US tariffs of 50% from August 2025 to early February, and the ongoing US-Iran war have spelt back-to-back shocks for the economy. Even as experts stress on the resilience of the growth story, the vulnerability to higher crude oil prices, and other global supply chain disruptions is a reality. In such a scenario, India may well have to contend with fluctuating world rankings, while banking on its strong GDP growth to tide over disruptions.

new video loaded: Why Your Paycheck Feels Smaller

By Ben Casselman, Nour Idriss, Sutton Raphael and Stephanie Swart

April 18, 2026

Everything to know about venue, guest list, dress, more

Secretary Doug Burgum expects Teddy Roosevelt’s induction into Pro Football Hall of Fame: report

Ariana Grande teases new era after ‘Eternal Sunshine’ with cryptic video

-

Politics1 week ago

Politics1 week agoIndian airlines hit hardest after Dubai limits foreign flights until May 31

-

Entertainment6 days ago

Entertainment6 days agoPalace left in shock as Prince William cancels grand ceremony

-

Sports5 days ago

Sports5 days agoThe case for Man United’s Fernandes as Premier League’s best

-

Politics1 week ago

Politics1 week agoChinese, Taiwanese will unite, Xi tells Taiwan opposition leader

-

Business6 days ago

Business6 days agoUK could adopt EU single market rules under new legislation

-

Entertainment1 week ago

Entertainment1 week agoDua Lipa hits major career high ahead of wedding with Callum Turner

-

Business1 week ago

Business1 week agoThe FAA wants gamers to apply for air traffic control jobs

-

Business1 week ago

Business1 week agoHe paid $248 in illegal tariffs for this coat. Will he ever get it back?