Fashion

US-Iran war pushes India denim prices up by $0.66/metre

In India, if a customer walks into a Zudio, Westside or OWND, they are presented with several new denim collections as part of the spring and summer offerings at these stores, with various styles including dresses, tops and a wide variety of jeans, including baggy and boot cuts.

And these are all being offered to customers at an affordable price range, attracting the younger shopper as well as the lower-income customers to the ****;*** ($*.**) and ****;*** price tags. But how long will this sustain?

According to Similarweb’s head of advisory services for CPG & retail, EMEA, Varvara Blazhko, the company’s data tracking web traffic to LVMH brand sites showed that physical retail sales have declined sharply, but the digital landscape appears less affected whereas in some markets and categories, still expanding.

LVMH saw footfall drop up to 70 per cent in the Middle East amid US-Israel-Iran conflict, while digital traffic remained more resilient with smaller declines and some growth.

This gap reflects shifting consumer behaviour, with e-commerce cushioning losses.

However, weak sentiment, inflation fears and ongoing tensions may delay recovery and push brands to rethink strategies.

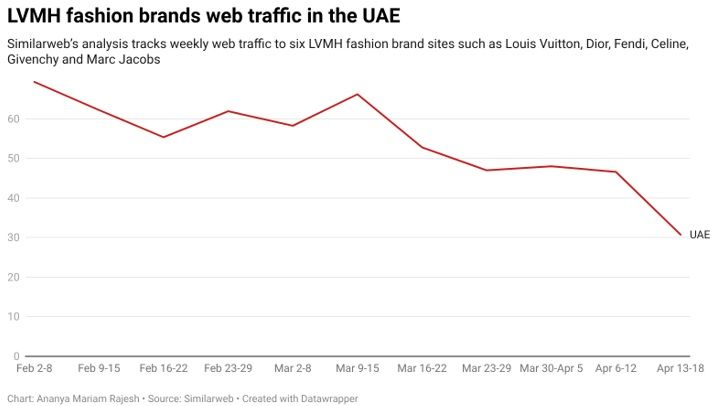

Similarweb’s analysis tracks monthly and weekly web traffic to six LVMH fashion brand sites such as Louis Vuitton, Dior, Fendi, Celine, Givenchy and Marc Jacobs and three other major brands, namely Sephora, TAG Heuer, and Hublot. The data was specifically tracked and analysed on Fibre2Fashion’s request.

Blazhko said that online traffic to LVMH’s fashion websites in the UAE only declined by 7 per cent year-over-year in March, while weekly visits declined slightly after February 28, rather than collapsing completely. She noted that Saudi Arabia as highlighted by Cabanis as well, was more resilient and stood out as the most digitally robust market.

On the other hand, last week, Cabanis said that there was a deterioration in foot traffic at its stores, mainly in the Middle East region, which accounts for 6 per cent of LVMH’s turnover. The initial decline in traffic once the war broke out was between 30-70 per cent, with 50 per cent as an average fall, according to the LVMH CFO.

Middle East vs EU traffic in view of a war

The Middle East is widely regarded as a global luxury hub and a key shopping destination for tourists. The region contributes significantly to sales for major brands such as LVMH, Prada and Ralph Lauren.

Blazhko highlighted that February to March typically sees a strong seasonal increase across the Gulf. In 2025, fashion traffic rose by 36 per cent in the UAE, 67 per cent in Saudi Arabia, and 64 per cent in Qatar.

But this year, the UAE’s growth was negligible with a 2.1 per cent decline, Qatar falling 13.2 per cent, and Saudi Arabia despite a slowdown, growing by 22.8 per cent, making it the only Gulf market to maintain its seasonal boost.

She observed that these shifts of 38 to 77 percentage points are much steeper than the 13-point seasonal variation observed in Europe’s top five markets, indicating that the conflict is the main cause. Last week, LVMH pointed out that the conflict in the Middle East also impacted sales in Europe, sending it down to 3 per cent.

LVMH’s European market web traffic was also down, with a 19 per cent fall in March across the UK, from a year ago, while Italy was down by 32 per cent, Germany fell by 27 per cent with Blazhko observing that the Gulf’s digital decline is milder than Europe’s, despite being a conflict zone.

Blazhko highlighted that the European and Gulf trajectories are now diverging as weekly fashion traffic across the five European markets rebounded in early April relative to their March average, with web traffic in Italy seeing a 26.9 per cent rise, Germany’s traffic jumping by 19.3 per cent, Spain increasing 25.1 per cent, France an 8.4 per cent rise and the UK’s traffic up 3.6 per cent while the UAE continued to decline.

“This suggests Europe’s softness in March was largely cyclical, while the Gulf’s downturn is conflict-driven and ongoing,” Blazhko said.

“The real impact on digital sales may be greater than year-on-year comparisons suggest. The gap between digital and physical performance remains significant, and LVMH’s e-commerce setup appears to offer protection that traditional retail cannot match,” Blazhko said.

Neil Saunders, managing director of retail at Global Data, told Fibre2Fashion in an emailed interview that in a lot of Western markets, the consumer remains under considerable financial pressure.

“This has recently been exacerbated by rising gas prices and uncertainty that has been caused by the Iran conflict. So there has been a retrenchment from luxury, especially among middle-income consumers. LVMH has a very strong portfolio and is well managed, but it is not immune to the cooling effect of the Iran situation,” Saunders added.

Will luxury bounce back?

Around this time last year, the entire world was grappling with the sudden spike in tariffs due to US President Donald Trump implementing sweeping duties on the country’s global trading partners, and luxury companies were continuing to see a slowdown.

The luxury sector was betting on the Middle East as it tackled China’s growth concerns, but the war has upended the slow recovery that was taking place late last year, putting several luxury firms in a tight spot again.

“The conflict in the Middle East could disrupt the steady recovery luxury goods makers had been anticipating this year,” said Danni Hewson, head of financial analysis at AJ Bell. She added that while the direct impact from fewer wealthy shoppers visiting malls in places like Dubai may be moderate, the bigger concern is the potential hit to overall consumer confidence amid inflation fears.

However, LVMH CFO Cabanis said “what we have not seen yet is repatriation, and what we know is that the wealth has not evaporated, so there will be a time where we will see that coming, probably elsewhere, and mitigate the impact, should the conflict continue.” The war impacted LVMH’s overall organic growth by 1 per cent during the first quarter.

“If shoppers press pauses on big-ticket purchases again, the anticipated recovery for companies like LVMH could be curtailed,” Danni Hewson said. She added that while wealthy consumers may weather another cost-of-living crisis, uncertainty from global upheaval could shift behaviour, prompting luxury brands to reassess their outlook, especially if the conflict continues into the summer.

Cabanis, during the earnings call last week, said that the Middle East was “quite a profitable market” and if the company is losing 1 euro in sales, it was probably losing a bit more in margin.

Similarweb’s data showed that UAE LVMH’s fashion brands saw web traffic decline of 7.1 per cent in March, when compared to a year ago. Blazhko noted the 7.1 per cent was just a fraction of the 70 per cent physical retail drop, Cabanis cited.

According to the data, there was no sharp decline after February 28 and louisvuitton.com’s weekly visits ranged from 26,000 to 34,000 in March, compared to 32,000 to 36,000 in February.

Blazhko noted that for the UAE, the April trajectory showed that the overall fashion brands’ weekly averages fell further, almost recording a 26 per cent decline, and the week of April 13 to April 18 recorded nearly 31,000 website visits and was the lowest in Similarweb’s dataset, with no bounce-back signal yet in the region.

Similarweb analysed Saudi Arabia’s web traffic, showing a 49.5 per cent jump from a year ago in March, and Qatar’s traffic saw a 10.8 per cent decline. Data from Similarweb shows total web traffic—across desktop and mobile—for the UAE and Europe, while only desktop data is available for Saudi Arabia and Qatar.

The company noted that for Saudi Arabia and Qatar, desktop figures represent a directional signal but undercount total digital activity, and smaller domains in these markets carry more volatility.

“The gap between physical and digital performance raises the question of whether e-commerce is partially offsetting lost footfall, or whether these represent fundamentally different customer segments,” Blazhko concluded.

Fibre2Fashion News Desk (AMR)

Median perceived inflation over the past 12 months rose to 3.5 per cent in March from 3.0 per cent in February. Short-term inflation expectations increased sharply, with one-year ahead expectations climbing to 4 per cent from 2.5 per cent, while three-year expectations rose to 3 per cent from 2.5 per cent. Longer-term expectations edged up slightly to 2.4 per cent from 2.3 per cent, ECB said in a press release.

Euro area consumers grew more pessimistic in March 2026 as inflation expectations rose, with one-year ahead forecasts reaching 4 per cent, as per ECB.

Spending expectations strengthened, while income outlook remained unchanged.

Growth expectations fell to -2.1 per cent and unemployment expectations increased.

Consumers also expected higher house prices and mortgage rates, signalling a cautious outlook.

Across income groups, lower-income households continued to report slightly higher inflation perceptions and expectations than higher-income groups, although the overall trend of rising expectations was broadly consistent. Younger respondents reported lower inflation expectations than older cohorts.

Consumers’ income outlook remained subdued. Expected nominal income growth over the next 12 months was unchanged at 1.2 per cent. However, spending expectations strengthened, with expected spending growth rising to 4.1 per cent from 3.5 per cent, the highest level since May 2023. Perceived spending growth over the past year also increased to 5.1 per cent.

Economic sentiment weakened further. Growth expectations for the next 12 months fell deeper into negative territory at -2.1 per cent, compared with -0.9 per cent in February. At the same time, the expected unemployment rate 12 months ahead rose to 11.3 per cent from 10.8 per cent, with lower-income households anticipating higher joblessness than higher-income groups.

The ECB said the results point to a more cautious consumer outlook, marked by rising inflation concerns, resilient spending expectations, and a deteriorating view of economic growth and labour market conditions.

Fibre2Fashion News Desk (SG)

Imports of knitted apparel (HS **) eased to NZ$*,***.** million (~$***.** million) from NZ$*,***.** million, registering a decline of *.* per cent. Similarly, non-knitted apparel (HS **) imports fell to NZ$***.** million (~$***.** million) from NZ$***.** million, down *.* per cent. The parallel softness across both segments indicates broad-based stabilisation in garment demand rather than category-specific weakness.

In contrast, textile fabric imports (HS **) showed strong growth, rising to NZ$**.** million (~$**.** million) in fiscal ****–** from NZ$**.** million in the previous fiscal, marking an increase of **.* per cent. This suggests relatively steady demand for intermediate inputs even as finished apparel imports softened.

Taylor Swift reveals favourite part of working with pal Jack Antonoff

US-Iran war pushes India denim prices up by $0.66/metre

UAE dismantles drug ring worth over Dh3m

-

Politics1 week ago

Politics1 week agoUK’s Starmer seeks to deflect blame over Mandelson appointment

-

Business1 week ago

Business1 week agoHow Trump’s psychedelics executive order could unlock stalled cannabis reform

-

Entertainment1 week ago

Entertainment1 week agoLee Anderson, Zarah Sultana kicked out of UK Parliament for calling PM ‘liar’

-

Business1 week ago

Business1 week agoUs-India Trade Talks: US–India trade deal: Where do talks stand & what to expect – explained – The Times of India

-

Fashion1 week ago

Fashion1 week agoIndia, US to resume BTA talks today

-

Tech1 week ago

Tech1 week agoA Humanoid Robot Set a Half-Marathon Record in China

-

Sports1 week ago

Sports1 week ago‘It’s his superpower’: Inside Fernando Mendoza’s extraordinary rise to No. 1

-

Business1 week ago

Business1 week agoUK inflation accelerates after Iran war drives sharp rise in fuel prices